Before inputting figures into any short term disability calculator, a thorough review of your policy's precise terms is imperative. An accurate calculation is impossible without first understanding concepts such as your wage replacement rate, the maximum benefit cap, and—most critically—how your insurer defines pre-disability earnings. These are not mere technicalities; they are the fundamental mechanics governing your potential benefits.

Understanding Your Disability Coverage

To ascertain a realistic expectation of your short-term disability income, you must move beyond assumptions and analyze the specific language within your policy documents. This is especially true for high-net-worth individuals, whose compensation packages are frequently a complex blend of salary, bonuses, and commissions. For executives, this step is not just advisable—it is essential for prudent financial stewardship.

While the formula insurers employ is relatively standard, the inputs are entirely unique to your income structure and your specific policy terms.

The global disability insurance market underscores the critical nature of this coverage. Valued at approximately USD 4.17 billion in 2024, the market is projected to expand to an estimated USD 12.36 billion by 2034, with short-term disability insurance at the forefront of this growth. This data point is not arbitrary; it signifies a growing recognition that safeguarding one's income stream is a non-negotiable aspect of modern wealth management.

The Core Benefit Formula

At its essence, the calculation appears straightforward: multiply your pre-disability earnings by a wage replacement percentage. However, the nuance lies in the details.

What precisely constitutes "pre-disability earnings"? Some policies may consider only your base salary. Others might average your total compensation over a preceding period. This single definition is determinative.

Understanding the precise definition of 'earnings' in your policy is the most critical step. For executives, failing to account for how bonuses or vested equity are treated can lead to a significant overestimation of benefits.

A policy that solely covers your base salary will yield a vastly different benefit amount than one that includes variable compensation. You must identify this definition before commencing any calculations.

Key Policy Variables for High Earners

To facilitate your analysis, the following table outlines the essential terms you will encounter in any short term disability calculator, with definitions specifically tailored for executive and high-earner compensation structures.

Key Policy Variables for High Earners

| Term | Definition for High Earners | Impact on Calculation |

|---|---|---|

| Pre-Disability Earnings | The definition of income used for the calculation. Critically, does it include base salary only, or also bonuses, commissions, and RSU vesting? | This is the foundational number. A narrow definition significantly lowers the potential benefit. |

| Wage Replacement Rate | The percentage of your defined earnings the policy pays. Typically 50% to 70%. | A higher percentage directly increases the gross benefit, but it is often tethered to a lower benefit cap. |

| Maximum Benefit Cap | The absolute dollar limit on your weekly or monthly benefit, irrespective of your income or replacement rate. | This is the most common reason for a significant income gap for high earners. It can render a high replacement rate meaningless. |

| Elimination Period | The "waiting period" from the date of disability until benefits commence. Often 7 to 14 days. | This determines when you start receiving payments. A longer period necessitates a greater reliance on personal liquidity. |

Consider each of these variables as a lever that can either augment or diminish your final payout. Familiarizing yourself with the common insurance policy terms that define these calculations is a worthwhile investment of time.

You will encounter several of these critical terms repeatedly:

- Wage Replacement Rate: This is the percentage of your pre-disability earnings you will receive, usually between 50% to 70%.

- Maximum Benefit Cap: Most policies, particularly group plans, impose a strict dollar limit on your weekly or monthly payout. This cap is a frequent and unwelcome discovery for high earners.

- Elimination Period: Also known as a waiting period, this is the number of days you must be out of work before benefits commence. It is commonly seven to 14 days.

It is also prudent to understand the legal context. For instance, in certain European financial centers, regulations such as the Dutch Sickness Benefits Act can influence the design and disbursement of employer-provided benefits. Ultimately, a meticulous review of these key variables is the only way to construct a financial projection that is truly reliable.

How to Calculate Your Net Disability Benefit

Transitioning from theory to practical application—from understanding policy language to calculating your actual entitlement—requires a methodical approach. Determining your net benefit is not as simple as applying a percentage. It involves a series of adjustments for your specific pay structure, policy limitations, and tax implications. For a high earner, each of these steps can dramatically alter the final figure.

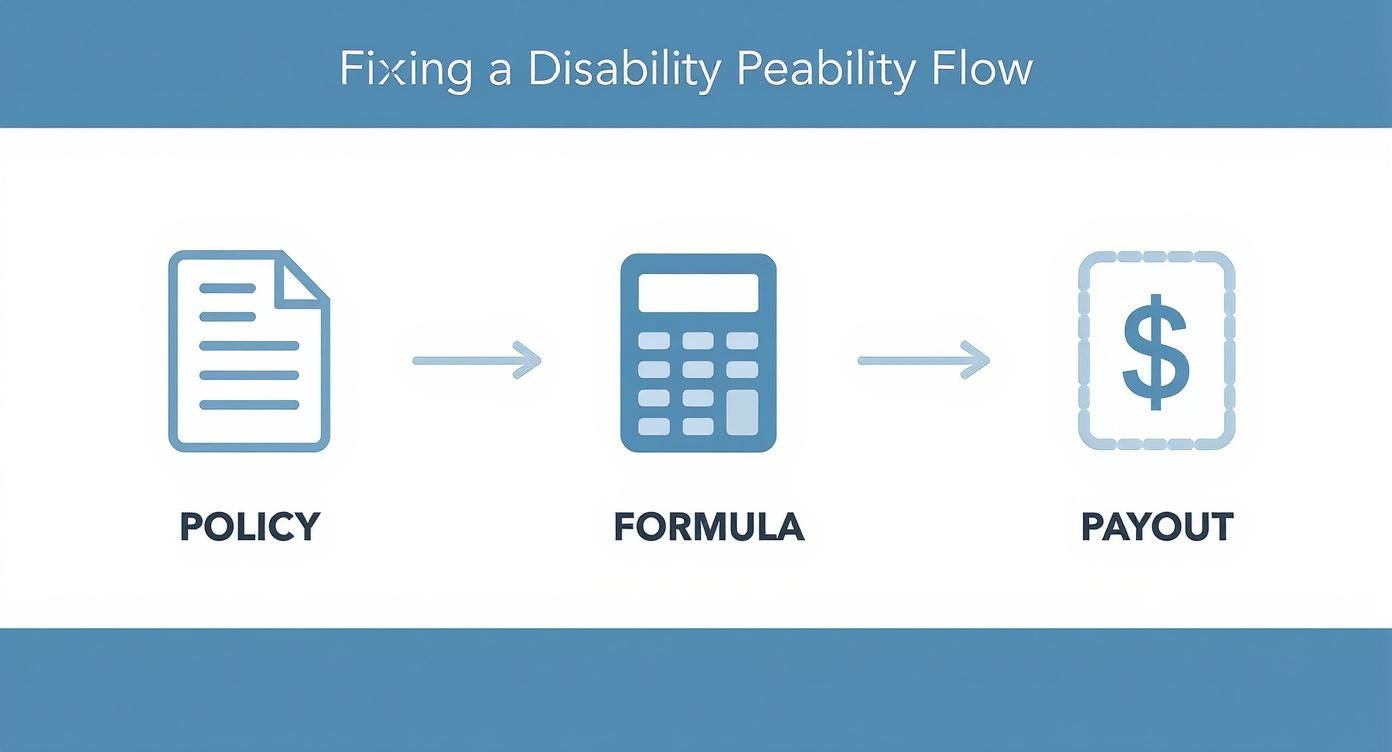

This visual guide provides a high-level overview of how your policy terms translate into a final payout.

As illustrated, the path from policy to payment involves several distinct stages. Ensuring the accuracy of each input from the outset is absolutely critical.

Define Your Pre-Disability Earnings

First, you must establish your pre-disability earnings. This is the baseline figure the insurer uses for all subsequent calculations. If you have a complex compensation structure, this figure is almost never your annual salary divided by 52.

You must delve into your policy documents to see how "income" is defined. Verify these common components:

- Base Salary: This is almost always included.

- Commissions and Bonuses: These are often covered but are typically averaged over a defined period, such as the previous 12 or 24 months.

- Vested Stock Units (RSUs): Coverage for equity compensation is rare in standard group plans and usually requires a specialized individual policy.

An incorrect definition of this baseline is the single most prevalent error. An inaccurate starting point renders the entire calculation invalid.

Apply the Wage Replacement Rate and Maximum Cap

With an accurate pre-disability earnings figure, you can now apply your policy's wage replacement percentage. For well-structured employer-sponsored plans, this typically falls between 60% and 70%. For example, if your defined weekly earnings are $5,000 and your rate is 60%, your initial gross benefit is $3,000.

However, that figure is immediately measured against the maximum benefit cap. This is a hard ceiling on your benefit, regardless of your income. If your policy has a weekly maximum of $2,500, your benefit in the preceding example is reduced from $3,000 to $2,500. This cap is the primary reason high earners often face a substantial income gap under standard group policies.

A high wage replacement rate is effectively negated by a low benefit cap. Always solve for the cap first to understand your true maximum potential benefit.

Account for the Elimination Period

Your benefits do not begin on the first day of disability. Every policy includes an elimination period—a waiting period—which is the time you must wait before payments commence. For short-term disability, this is typically 7 to 14 days.

During this interval, you will receive no income from your disability policy. It is essential to have sufficient liquidity to cover your obligations. To better understand how these waiting periods operate, you can read more about how excesses and deductibles function in insurance policies. This is a crucial component of your immediate cash flow planning.

Factor in Benefit Offsets

Your disability payment can be further reduced by other income you might receive while you are unable to work. These are known as offsets. Insurers use them to ensure you are not earning more while disabled than you did while working.

Common offsets include:

- State Disability Benefits: In jurisdictions with mandatory programs (like California or New York), your private plan will subtract any state-provided payments.

- Workers' Compensation: If your disability is work-related, these benefits will almost certainly be deducted.

- Social Security Disability Insurance (SSDI): While more common with long-term disability, this can sometimes apply and will serve as an offset.

For instance, if your calculated private benefit is $2,500 per week, but you also receive $800 from a state program, your insurance company will only pay the difference: $1,700.

Determine the Tax Treatment

The final, and often most overlooked, step is determining if your benefits are taxable. This is what separates your gross benefit from the net payment deposited into your account. The rule is straightforward: it depends entirely on who paid the premiums.

- Pre-Tax Premiums: If your employer pays the premiums and you do not pay taxes on that amount as a fringe benefit (the most common arrangement in group plans), your disability benefits are taxable as ordinary income.

- After-Tax Premiums: If you pay the premiums yourself with your own post-tax dollars, your benefits are received completely tax-free.

The financial impact of this distinction is substantial. A taxable $2,500 weekly benefit could easily be reduced to $1,750 or less after federal and state taxes are withheld, completely altering your financial position.

These types of analytical tools are not just for individual planning; they can also be powerful instruments for user engagement. For any organization developing a financial wellness platform, embedding a sophisticated calculator widget for websites is an excellent way to add tangible value. By performing these steps, you can move from a vague estimate to a clear, actionable net benefit figure.

Real-World Scenarios: Putting the Numbers to the Test

Policy documents and abstract formulas are one matter. Witnessing how they perform with actual financial data is another. To truly comprehend the financial implications of a short-term disability event, it is necessary to model calculations based on common, high-earner compensation structures.

These are not generic examples. These case studies are designed to reflect the complex pay packages of executive clients, demonstrating precisely how a calculator processes different income streams to arrive at a final number.

By examining these profiles, you will see common pitfalls and hidden details in practice. This is the clarity required to apply the same logic to your own circumstances.

Scenario One: The C-Suite Executive

Consider a Chief Financial Officer. Her group disability policy offers 60% wage replacement, capped at a $2,500 weekly maximum, with a seven-day waiting period. The policy's fine print is key: it defines "earnings" as base salary plus the prior year's cash bonus. Her employer pays 100% of the premiums before taxes.

Her compensation is as follows:

- Base Salary: $400,000

- Annual Bonus (previous year): $200,000

- Total "Covered" Earnings: $600,000

First, we determine her pre-disability weekly earnings. We take her total covered earnings of $600,000 and divide by 52 weeks, which gives us $11,538 per week.

Next, we apply the 60% replacement rate: $11,538 x 0.60 = $6,923. This is her potential gross weekly benefit. But this is where the benefit cap imposes a stark reality.

For high earners, the maximum benefit cap almost always supersedes the wage replacement percentage. It is the true ceiling on your potential income replacement from a standard group policy.

The policy's $2,500 weekly maximum is a small fraction of the calculated $6,923. Her actual gross weekly benefit is reduced to just $2,500. Because her employer paid the premiums, this benefit is fully taxable. Assuming a combined effective tax rate of 35%, her net weekly income is approximately $1,625. This represents a massive, and often shocking, income shortfall.

Scenario Two: The Commission-Based Sales Director

Next, consider a Sales Director whose income is predominantly commission-based. His policy appears generous—a 70% wage replacement rate—but the weekly maximum is only $2,000. His plan defines earnings as the average total compensation over the prior 12 months, and he pays for his premiums with after-tax dollars.

His income over the last year was:

- Base Salary: $150,000

- Commissions: $250,000

- Total Earnings: $400,000

To calculate his pre-disability weekly earnings, we divide $400,000 by 52, which is $7,692 per week. Applying the 70% rate yields a potential gross benefit of $5,384 weekly ($7,692 x 0.70).

Again, the policy's cap is immediately triggered. His gross weekly benefit is reduced to the $2,000 maximum. However, there is a critical distinction: because he paid the premiums with his own after-tax funds, the entire $2,000 weekly benefit is received tax-free. This single detail results in a net benefit that is significantly higher than the CFO's, despite a lower cap.

Scenario Three: The Tech Professional with Equity

Finally, let us examine a Senior Software Engineer at a major technology firm. Her compensation is a mix of base salary and Restricted Stock Units (RSUs) that vest quarterly. Her group plan offers 60% replacement with a $3,000 weekly maximum. The policy, like nearly all group plans, explicitly excludes equity compensation from its definition of earnings.

Her pay structure:

- Base Salary: $250,000

- Annual RSU Vesting: $150,000 (Completely excluded by the policy)

The only income the disability calculator considers is her base salary. We calculate her pre-disability weekly earnings as $250,000 / 52 = $4,808.

Applying the 60% rate gives a gross benefit of $2,885 per week ($4,808 x 0.60). In this case, the amount is below the $3,000 weekly cap, so the cap is not a factor. If her employer pays the premiums pre-tax, that $2,885 is taxable income.

This scenario reveals a substantial hidden risk for any professional with significant equity compensation. A large portion of their income is completely unprotected by their standard disability plan, creating an income gap far larger than they may have anticipated. These examples prove that a meaningful calculation requires looking past the headline percentage and scrutinizing every single variable—from earnings definitions to tax regulations.

Navigating State and International Regulations

For the globally mobile executive, understanding the intricate web of disability regulations is not merely an academic exercise—it is a critical component of managing financial risk. A short term disability calculator is only as effective as the real-world context provided. Your benefit structure can shift dramatically depending on whether your professional base is in New York, London, or Singapore.

The landscape of disability coverage is far from uniform. In the United States, for example, private insurance is the predominant model. According to the U.S. Bureau of Labor Statistics, in March 2023, 43% of private industry workers had access to short-term disability insurance plans. Access varies significantly by establishment size.

Only 31% of workers in smaller firms (fewer than 100 employees) have access to these benefits. This figure rises to 68% in large firms with 500 or more employees. This disparity highlights why a meticulous review of your specific employer-sponsored plan is essential. You can examine the official data on employee benefits in the United States for a comprehensive overview.

This patchwork system means most American professionals rely entirely on their employer's group plan or a private policy they have personally secured. However, a few states have mandated a baseline of coverage.

Mandatory State Disability Programs in the US

While most of the U.S. has no mandated short-term disability insurance, five states have established their own programs. If you work in one of them, this state-level benefit becomes a foundational piece of your income protection strategy.

These states are:

- California

- New York

- New Jersey

- Rhode Island

- Hawaii

These state-mandated programs provide a safety net, but the benefit amounts are typically modest and subject to a low weekly maximum. For a high earner, they will replace only a small fraction of your income. Their primary role in your calculation is as an offset. Your private or group disability insurer will almost certainly reduce its payout by the exact amount you receive from the state, ensuring your total benefit does not exceed your policy's replacement rate.

A state disability program is not a bonus—it is an integrated component. Your private insurer will factor it into their calculation, meaning your total benefit remains the same. The payment simply originates from two different sources.

An International Perspective for Global Professionals

Outside the US, the entire approach to disability and sickness benefits changes. Many of the world's financial centers have robust, government-mandated social security systems that provide a much higher level of income replacement than their American state-level counterparts.

In locales such as London, Singapore, or across the European Union, statutory sick pay and social insurance systems serve as the first line of defense. Employer-sponsored plans are typically designed to "top up" these government benefits, rather than acting as the primary source of income.

This is a critical distinction when using any short term disability calculator. You must begin by understanding the statutory benefits you are entitled to in your country of residence. Only then can you accurately assess the role and value of your private or group international medical insurance. To gain a better understanding of how these policies are constructed, you may wish to review our guide covering international private medical insurance benefits uncovered. Understanding these foundational differences is essential for anyone managing a career across multiple financial centers.

For example, a professional based in London has access to Statutory Sick Pay (SSP). An executive in Germany benefits from a system where the employer must continue paying a high percentage of their salary for a defined period. A private disability policy in these regions is structured around these existing benefits, filling gaps rather than providing core coverage. This legal and cultural framework directly shapes policy design, premiums, and the final net benefit you receive, rendering any one-size-fits-all calculation useless.

How High Earners Can Optimize Their Disability Coverage

For high earners, processing the numbers through a short term disability calculator often leads to a jarring realization: your employer's group policy likely leaves a substantial portion of your income entirely unprotected. Suddenly, the conversation transcends mere mathematics; it becomes about the proactive protection of your wealth. Disability insurance is not just another employee benefit—it is a critical tool for neutralizing one of the greatest financial risks you face: the loss of your ability to earn.

Your first action should be a meticulous, line-by-line review of your existing short-term and long-term disability policies from your employer. You are looking for the precise point where your income outstrips the coverage, which is almost always due to a restrictive maximum benefit cap. For an executive, this gap can easily translate into hundreds of thousands of dollars in unprotected income annually.

Bridging the Gap with Individual Disability Insurance

This is where supplemental individual disability insurance (IDI) becomes non-negotiable. Unlike a one-size-fits-all group plan, an individual policy is portable and remains with you even if you change employers. You can structure it to cover a much larger portion of your total compensation, including bonuses and commissions that group plans often exclude. It is designed to stack directly on top of your group coverage, activating to fill the income void created by those policy maximums.

The market is responding to this demand. Workplace short-term disability insurance is expected to see premium growth of approximately 4.0%, a reflection of both economic activity and a growing awareness of income protection. You can see a more detailed forecast on the growth of the workplace disability insurance market here.

Consider it this way: your group plan is the foundation, but a private IDI policy is the custom-built structure that protects your high-net-worth lifestyle. Coordinating the two is the cornerstone of a truly resilient income protection strategy.

Must-Have Provisions in a Private Policy

When procuring a private policy, a few features and definitions are absolutely critical for a highly-skilled professional. The most important of these is the 'own-occupation' definition of disability.

This provision is paramount for specialists such as surgeons, trial lawyers, or financial traders. It defines "disabled" as being unable to perform the specific duties of your occupation, even if you are capable of working in another capacity. Without it, an insurer could deny your claim by arguing you can still earn a living as a consultant or lecturer, completely disregarding the specialized skills and substantial earning potential you have lost.

Other vital elements to look for include:

- Residual Disability Rider: This provides partial benefits if you can still work part-time but have suffered a loss of income due to your disability.

- Cost of Living Adjustment (COLA) Rider: On a long-term claim, inflation can erode the value of your benefit. A COLA rider increases your payout annually to keep pace.

- Future Increase Option: This allows you to purchase additional coverage later as your income grows, without undergoing new medical underwriting.

Ultimately, your ability to earn is your most valuable asset. Treating your disability coverage as a set-it-and-forget-it benefit is a significant misstep. An annual review to ensure your protection keeps pace with your career is more than just sound financial hygiene—it is a fundamental aspect of responsible stewardship of your success.

Common Questions Answered

When navigating the complexities of disability insurance, a few key questions invariably arise, particularly for high-earning professionals. Obtaining clear answers is the only way to construct an income protection strategy that will perform as expected. Here are the most common inquiries.

How Are Bonuses and Commissions Treated?

This is an area where the policy's fine print is of utmost importance. The handling of variable pay like bonuses and commissions is dictated entirely by the specific contract. Most standard group plans—those provided by an employer—cover only base salary. For any individual whose compensation is heavily weighted towards performance pay, this creates a substantial, often unforeseen, coverage gap.

Conversely, a well-structured individual disability insurance (IDI) policy can be designed to include these income streams in its definition of "pre-disability earnings." It is absolutely critical to review this definition in your policy documents. Discovering your bonus is not covered after a disability has occurred is a detrimental surprise.

Why Does an Own-Occupation Definition Matter So Much?

For highly specialized professionals, an "own-occupation" definition of disability is not merely a desirable feature; it is the core value of the policy. It stipulates that you are considered disabled if you are unable to perform the specific duties of your career—such as a surgeon, trial lawyer, or software architect—even if you could theoretically work in another field.

This provision is what protects your high earning potential in your chosen profession. A less protective "any-occupation" policy might cease paying benefits if you are able to work at all, even if it entails a drastic reduction in income and an abandonment of your expertise.

Will My Disability Benefits Be Taxed?

The taxability of your benefits depends on a single, simple question: who paid the premiums? The answer can alter the net amount you receive by a significant margin.

- Employer-Paid Premiums: If your employer pays the premiums and you do not pay taxes on that benefit (a common pre-tax arrangement), your disability benefits will be taxable as ordinary income.

- You-Paid Premiums: If you pay the premiums yourself with after-tax funds, the benefits you receive are typically completely tax-free.

This difference can easily impact your net, in-pocket benefit by 30% or more. It is a massive factor to consider when calculating your actual replacement income.

Can I Receive Both State and Private Benefits?

Yes, it is possible to receive payments from both a state-run disability program and your private insurance policy, but do not expect to receive the full amount from both.

Private group policies almost invariably contain an "offset" provision. This clause allows your insurance company to reduce the benefit it pays you by the exact amount you receive from other sources, such as a state program. It is designed to ensure your total replacement income does not exceed your policy's maximum percentage, preventing a scenario where you would earn more while disabled than you did while working.

At Riviera Expat, we provide the clarity and expert guidance necessary to navigate these complex insurance decisions. Our specialists help you build a comprehensive income protection strategy that aligns with your unique financial circumstances. For a confidential consultation, visit us at https://riviera-expat.com.