For discerning individuals residing in or relocating to the United Kingdom, a robust private health insurance in United Kingdom plan is not merely a benefit—it is an essential component of a sophisticated personal risk management strategy.

While the state-funded National Health Service (NHS) provides a comprehensive standard of care, the private healthcare sector operates in parallel, engineered for expediency, choice, and a superior level of comfort and privacy. Understanding the interplay between these two systems is the foundational step to securing the calibre of medical attention you expect for yourself and your family.

Understanding the UK Healthcare Landscape

Navigating healthcare in the UK requires a precise understanding of its unique dual structure. The foundation is the National Health Service (NHS), a comprehensive, tax-funded system providing care free at the point of delivery to all legal residents.

The UK's investment in this system is substantial. According to the Office for National Statistics, total UK healthcare expenditure was 11.3% of GDP in 2022. This commitment makes the NHS a cornerstone of the nation's social contract, funded through general taxation to serve millions.

However, for high-net-worth individuals, executives, and their families, time is an irreplaceable asset. While the NHS excels in handling acute emergencies and critical care, its resources are significantly constrained when addressing elective procedures and specialist appointments.

The primary challenge within the public system is not the quality of clinical care—it is the wait. Protracted delays for diagnostics and non-urgent treatments can result in unacceptable interruptions to both personal well-being and professional commitments.

The Private Sector Alternative

This is precisely where the private healthcare sector offers a vital alternative. Operating alongside the NHS, it provides a direct pathway to circumvent delays. Private health insurance is the mechanism that unlocks this parallel system.

It grants immediate access to leading specialists, premier hospitals, and a level of service and discretion commensurate with your expectations. When evaluating options, it is instructive to examine how the two systems manage specific diagnostic pathways. This resource provides a clear breakdown of navigating both NHS and private pathways for autism and ADHD assessments in the UK.

The UK's dual-track system presents a clear strategic choice. You may rely solely on the NHS, or you can implement a private health insurance plan to guarantee prompt attention when it matters most. For many, the decision is self-evident.

A private plan functions as a powerful tool, ensuring a health concern does not escalate into a significant life disruption. It restores your control over your healthcare—from selecting your consultant to scheduling procedures at your convenience. It is a matter of safeguarding your health, your wealth, and your time.

To clarify this choice, let us delineate the key differences between relying on the NHS and opting for private care.

Comparing NHS and Private Healthcare for HNWIs

This table offers a direct comparison of what to expect from each system.

| Feature | National Health Service (NHS) | Private Healthcare |

|---|---|---|

| Cost | Free at the point of use, funded by taxation | Paid via insurance premiums, employer, or self-funding |

| Waiting Times | Can be extensive for non-urgent procedures and specialist consultations | Minimal to zero waiting times for appointments and treatments |

| Choice of Specialist | Typically assigned a consultant based on geography and availability | You select your preferred specialist from an extensive network |

| Hospital Choice | Assigned to an NHS hospital, generally the nearest one | Choice of private hospitals from your insurer's network |

| Accommodations | Generally in a shared ward with multiple patients | Private, en-suite rooms ensuring comfort and confidentiality |

| Access to Drugs & Treatments | Access to treatments approved by NICE, which can involve delays | Faster access to novel drugs and advanced therapeutic options |

| Convenience | Appointments are scheduled by the hospital, offering limited flexibility | Procedures and consultations are scheduled around your availability |

| Emergency Care | The primary and most effective option for all life-threatening emergencies | Private facilities are not equipped for major Accident & Emergency services |

Ultimately, the choice is not about one system being inherently "better" but about which aligns with your personal and professional priorities. The NHS provides a universal safety net, particularly for emergencies, while private insurance offers a premium service focused on speed, choice, and comfort for non-urgent care. Many sophisticated clients adopt a hybrid approach—relying on the NHS for emergencies while utilising private insurance for all other medical needs—to achieve the optimal outcome.

Why Discerning Individuals Choose Private Insurance

While the NHS serves as an essential safety net, for a certain calibre of individual, time is the one asset they cannot afford to squander. The decision to invest in private medical insurance (PMI) is rarely about questioning the clinical quality of the NHS. It is a strategic manoeuvre to reclaim control over one's health, on one's own terms.

The single most significant driver is bypassing the extensive waiting lists for diagnostics, specialist consultations, and non-emergency surgery. For a busy executive or entrepreneur, these are not minor inconveniences; they are substantive disruptions that can derail critical projects and impact family life.

The Data Confirms the Trend

This is not merely anecdotal; the data reveals a clear trajectory. Demand for private health insurance in the United Kingdom has escalated, mirroring growing concerns over the NHS's capacity to provide timely care. The number of individuals securing private medical cover has risen markedly since 2020.

It is no coincidence that this trend aligns perfectly with NHS waiting list figures, which climbed from 4.4 million in February 2020 to 7.54 million in February 2024. A growing number of individuals are electing to pay for expedited access. You can explore the data behind this growing demand for private insurance here.

This data reframes private insurance not as an extravagant luxury, but as a pragmatic solution to a system under palpable pressure. It is a tool for those who value certainty and efficiency.

Private medical insurance is fundamentally about risk mitigation. It is the assurance that when you or your family require medical attention, you can access the very best care without delay, on your own terms.

This shift is not only personal; it is reshaping the corporate landscape. Top-tier employers now recognise that attracting and retaining elite talent requires more than a competitive salary. A comprehensive private health plan has become a standard, almost requisite, component of an executive benefits package. It sends an unequivocal signal: the company values its key personnel and understands that their performance is intrinsically linked to their well-being.

A Strategic Asset for Executives and Families

For high-net-worth families, the rationale is even more compelling. A robust family policy ensures that every member—from children requiring a paediatric specialist to a spouse needing a routine scan—receives consistent, high-quality care without delay. Such a unified approach provides profound peace of mind.

To fully appreciate how these plans deliver value, it is useful to deconstruct their core components. You can discover the benefits of international private medical insurance in our detailed guide.

Ultimately, opting for private health insurance is a strategic decision rooted in efficiency, control, and intelligent risk management. It transforms healthcare from a reactive event into a proactively managed component of a well-ordered life, ensuring your health remains an asset, not a liability.

Comparing Your Health Insurance Options

When examining private health insurance in the UK, the options fundamentally bifurcate into two principal types of cover. Each is engineered for a distinct lifestyle and geographic footprint. Comprehending this fundamental distinction is the first, and most critical, step toward securing a plan that aligns precisely with your life.

Your two primary choices are domestic Private Medical Insurance (PMI) and International Private Medical Insurance (IPMI). To use an analogy: PMI is a high-performance vehicle, perfectly engineered for UK roads. IPMI is a global-range private jet, prepared to transport you anywhere without a compromise in service or quality.

Domestic Private Medical Insurance

Domestic PMI is the standard for individuals and families whose lives are predominantly based in the United Kingdom. If you reside here and anticipate receiving all, or the vast majority, of your medical care within the UK, a domestic plan is an excellent and cost-effective solution.

These policies are structured to provide access to a network of private hospitals, leading specialists, and diagnostic centres across England, Scotland, Wales, and Northern Ireland. They are specifically designed to allow you to bypass NHS waiting lists for eligible conditions, fast-tracking consultations, scans, and elective surgeries. For a UK-based executive or family, a premium PMI plan affords the confidence that high-quality care is readily accessible.

International Private Medical Insurance

For the globally mobile executive, the expatriate family, or any individual dividing their time between countries, a standard domestic plan is inadequate. It is simply not designed for such a lifestyle. This is where International Private Medical Insurance becomes non-negotiable. IPMI is engineered to provide seamless, borderless medical cover.

Unlike a domestic policy, an IPMI plan is not constrained by the UK’s borders. It offers comprehensive coverage across a wide region—or even globally—ensuring you receive the same high standard of care whether you are in London, Dubai, or New York. These plans almost invariably include premium benefits not found in standard PMI policies, such as medical evacuation and repatriation. These are absolutely critical if you live or travel in locations where local healthcare may not meet international standards.

Our guide on choosing the right policy type for your needs delves much deeper into these distinctions.

For anyone whose business or lifestyle involves regular international travel, IPMI isn't merely an upgrade—it's a foundational component of your financial safety net. It guarantees continuity of care and eliminates the immense financial and logistical complexity of a medical emergency abroad.

Specialized Plans and Add-Ons

Beyond the core choice of domestic versus international, your policy can be refined to match your exact requirements. Consider these as modules that can be added to construct a truly bespoke safety net for you and your family.

Some of the most common enhancements include:

- Comprehensive Family Plans: These plans consolidate coverage for your entire family under a single, easily managed policy. They often include benefits tailored to children’s health and can be more cost-effective than insuring each individual separately.

- Dental and Optical Riders: Standard health plans typically exclude routine dental check-ups, fillings, or eye care. Adding a specific rider appends this coverage, providing a holistic approach to your well-being.

- Mental Health and Wellness Modules: A growing priority for many, these modules provide access to therapy, counselling, and psychiatric support, often with an emphasis on privacy and convenience through virtual consultations.

Ultimately, selecting the right health insurance in United Kingdom begins with a candid assessment of your life. If your world is UK-centric, a premium domestic PMI plan will serve you well. However, for the international professional or expatriate family, a comprehensive IPMI policy is the only viable solution for true global security.

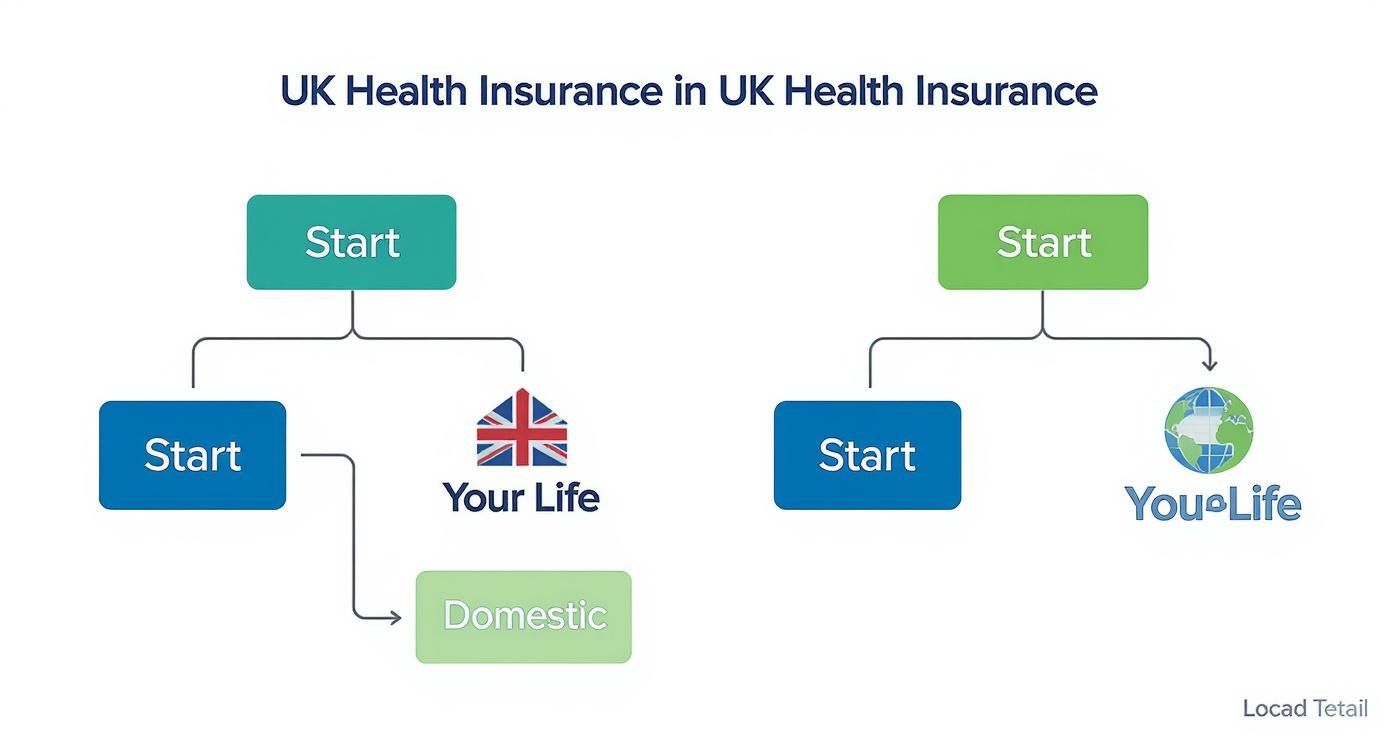

Decoding Key Policy Features and Exclusions

Selecting the right health insurance in United kingdom is not about choosing a brand or a price point. The real value is embedded in the policy wording—the specific features that grant you access to care and the exclusions that can prevent it. For any high-net-worth individual, mastering these details is paramount.

A premium policy is not just about gaining admission to a hospital; it is about securing access to the right one. The best plans open doors to elite networks of leading private hospitals and consultants, ensuring you are seen by top specialists in facilities renowned for exemplary service and absolute privacy.

This flowchart illustrates the first major decision you will need to make.

As you can see, the path bifurcates at the outset. Is your life primarily UK-based, or are you globally mobile? The answer to this single question dictates your entire strategy.

Core Benefits That Truly Matter

When scrutinising policy documents, certain features are far more critical than others, especially for those with demanding lifestyles or families to protect.

Generous outpatient limits are essential. This covers all diagnostics and consultations—MRIs, specialist visits, therapies—that occur before a hospital admission is considered. High limits mean you can obtain a diagnosis swiftly without concern for the cost, preventing a minor issue from escalating into a major problem.

Furthermore, advanced cancer care is completely non-negotiable. This refers not to standard treatments, but to securing access to next-generation pharmaceuticals, experimental therapies, and targeted treatments that the NHS might not approve for years. For executives and their families living internationally, comprehensive medical evacuation and repatriation are equally crucial. This is the ultimate safety net should a medical crisis occur while you are abroad.

The sophistication of a health insurance policy is measured by its response to complex medical needs. It should provide not just coverage, but a clear, unhindered pathway to the best possible care, wherever that may be in the world.

Understanding the Underwriting Process

How an insurer assesses your health history is termed underwriting, and it directly dictates what your policy will and will not cover. A clear understanding of this process is vital, as it determines your level of certainty from day one. There are two primary methods:

-

Full Medical Underwriting (FMU): This is the transparent approach. You provide a detailed medical history upfront, and the insurer responds with a clear offer, specifying precisely what is covered and explicitly stating any excluded conditions. For those who prioritise certainty above all else, FMU is the gold standard. There are no ambiguities.

-

Moratorium Underwriting: This is the more expedient option, as it forgoes an initial medical questionnaire. Instead, the policy automatically excludes any condition for which you have experienced symptoms or received treatment in the recent past (typically the last five years). These conditions may become eligible for cover later, but only after you complete a set period (usually two years) without any treatment, symptoms, or medical advice related to them. It is convenient, but it introduces a "wait-and-see" element that is not suitable for everyone.

The Critical Role of Exclusions

No policy covers everything. Understanding the exclusions is as important as knowing the benefits, as this is where unexpected financial liabilities arise.

The most significant exclusions are typically pre-existing and chronic conditions. A chronic condition is one that requires long-term management rather than a cure, such as diabetes or hypertension. While your policy will likely cover an acute emergency or flare-up, the routine, day-to-day management is often not included.

It is absolutely essential to gain clarity on these limitations before committing to a policy.

Ultimately, the only way to ensure a policy aligns with your life and provides the robust protection you require is through a meticulous review of its terms, ideally guided by an expert who knows precisely what to look for.

To help you navigate the terminology, we have compiled a glossary of the most important terms you will encounter. Consider it your reference for decoding insurance contracts.

Essential Health Insurance Policy Terminology

A glossary of key terms and concepts found in UK private and international health insurance policies to help you understand your coverage.

| Term | Definition for HNWIs | Strategic Implication |

|---|---|---|

| Annual Limit | The maximum amount the insurer will pay for all claims in a single policy year. | A low limit can be exhausted by a single serious medical event. For HNWIs, a high or unlimited annual limit is essential for true security. |

| Deductible / Excess | A fixed amount you must pay out-of-pocket for treatment before the insurance begins to pay. | A higher deductible lowers your premium. It can be used strategically to self-insure for minor costs while retaining comprehensive coverage for catastrophic events. |

| Co-payment | A percentage of the claim cost that you share with the insurer after the deductible has been met. | While it lowers premiums, co-payments can lead to unpredictable out-of-pocket expenses, especially for high-cost treatments. |

| Pre-existing Condition | Any medical issue for which you had symptoms, treatment, or advice before your policy began. | This is the single most common area for claim disputes. Full, transparent disclosure during underwriting is critical to avoid future complications. |

| Medical Evacuation | Emergency transportation to the nearest adequate medical facility when local care is insufficient. | A non-negotiable for anyone who travels. Ensure it covers transport to your home country, not just the "nearest" appropriate facility. |

| Guaranteed Renewability | The insurer’s contractual promise to renew your policy regardless of your age or any claims you have made. | This is crucial. Without it, an insurer could decline to renew your coverage after you develop a serious chronic condition, leaving you uninsured when you need it most. |

Understanding these terms is the first step. It empowers you to ask the right questions and to see beyond marketing materials to the actual substance of the protection being offered.

Structuring Your Plan for Optimal Value

Crafting the right private health insurance plan is an exercise in financial precision. Your monthly premium is not an arbitrary figure; it is the direct result of an insurer’s risk calculation, influenced by a clear set of factors about you and your desired level of cover.

Understanding these levers is the key to constructing a policy that delivers exceptional value without allocating funds to superfluous benefits.

At its core, your premium is shaped by your personal profile. Age is a significant factor, as health risks naturally increase over time. Your medical history, particularly any pre-existing conditions, will be closely examined. Lifestyle choices, such as smoking, also play a substantial role in the final calculation.

Beyond your personal profile, the coverage choices you make have a direct impact on the cost. What is the required scope of the hospital network? Is your cover limited to the UK, or do you require European or global reach? What level of outpatient benefits do you need? Each of these variables directly influences your premium.

Demystifying the Underwriting Process

The method by which an insurer assesses these factors is called underwriting, and it is a pivotal stage in your application. As previously mentioned, moratorium underwriting is the faster option, automatically excluding recent conditions for a set period.

In contrast, full medical underwriting (FMU) requires a detailed health declaration upfront. While it is more time-consuming, it provides absolute clarity on what is covered from day one. For any individual who values meticulous financial planning and wishes to avoid future ambiguities, FMU is almost always the superior strategic choice.

This level of planning is becoming increasingly critical. The UK's private health market is expanding, partly due to a growing awareness of the potential costs of untreated health issues. With NHS delays, many individuals are accumulating a 'hidden health debt' where minor conditions can worsen. The cost of treating advanced illnesses privately can be substantial, making robust insurance an essential tool for early intervention and protection from significant out-of-pocket expenses. You can read the full analysis on the UK health cover market to better understand these financial dynamics.

Strategic Financial Levers in Your Policy

You have direct control over several financial components within your policy that can be adjusted to manage your premium. This is not about compromising on care; it is about intelligently sharing a small, manageable portion of the financial risk with the insurer.

Consider these as dials you can turn to align the policy with your financial strategy:

-

Deductible (or Excess): This is the fixed amount you agree to pay towards a claim before the insurer contributes. Opting for a higher excess—for example, £500 instead of £0—signals to the insurer that you will manage minor costs yourself. This can significantly reduce your premium, allowing you to self-insure for small expenses while retaining full protection for major medical events.

-

Co-payment: This is a percentage-based cost-sharing arrangement. For instance, you might agree to a 10% co-payment on all claims up to a specified cap, such as £1,000. Similar to a deductible, it lowers your premium because you are covering a small fraction of the treatment cost.

Strategically utilising a deductible is one of the most effective ways to lower premiums without compromising the quality of your core coverage. It allows you to reserve your premier insurance for significant health matters, which is its primary purpose.

By carefully considering these factors and financial levers, you and your advisor can architect a health insurance in United Kingdom plan that is both cost-effective and perfectly aligned with your need for comprehensive, high-level protection.

Your Strategic Checklist for Selecting a Plan

Selecting the right private health insurance is not a matter of reviewing marketing brochures. It requires a diligent analysis—matching your real-world needs against the contractual reality of a policy document.

To execute this correctly, you need a clear-headed approach that cuts through promotional language. This checklist will help you focus on what truly matters, ensuring the plan you choose is the optimal fit for you and your family.

First, conduct an honest assessment of your family's health profile. What are your needs today, and what might they be in the future? Are specific paediatric specialists a requirement? Is there a family history of cardiac conditions or cancer that makes top-tier cover for those specialisms non-negotiable? Your answers form the bedrock of your search.

Next, turn your attention to the insurer’s network. A policy's value is directly tied to the doctors and hospitals it provides access to. You must confirm that the hospitals you would prefer to use are in-network, both within the UK and, for IPMI plans, in any other countries where you spend significant time.

Evaluating Coverage Depth and Limits

Beyond the network, the financial limits on specific treatments are what separate a truly premium policy from an average one. It is insufficient to see that a plan covers specialist consultations; you must investigate the annual limit for that outpatient care. A low cap can be exhausted by just a few diagnostic tests and follow-up appointments, leaving you with an unexpectedly large out-of-pocket expense.

Mental health services also demand close scrutiny. The best policies offer discreet, rapid access to leading therapists and psychiatrists, often with a separate financial limit that does not diminish your main medical allowance.

Critically, examine how the policy addresses chronic conditions. While most plans will not cover the routine costs of a pre-existing chronic illness, a superior one should absolutely provide robust cover for an unexpected acute episode or a newly diagnosed condition.

The true measure of a policy's strength is found in its fine print. A plan that appears comprehensive on the surface may contain subtle limitations on specialist access or chronic care that only become apparent when you need to make a claim.

The Value of a Specialist Broker

Attempting to navigate this complex landscape independently is a formidable task, and it is easy to make a costly error. The market for health insurance in United Kingdom is intricate, and insurer policy documents are filled with jargon designed to protect them, not you. This is where engaging a specialist broker provides a significant strategic advantage.

An independent broker works for you, not the insurance company. Their role is to:

- Survey the Entire Market: A specialist has a comprehensive view of all available options, comparing policies from dozens of insurers to find the one that truly fits your needs, rather than promoting a single company's products.

- Negotiate Favourable Terms: Brokers cultivate long-term relationships with insurers. This often enables them to secure better terms or underwriting conditions than you could obtain by applying directly.

- Ensure the Right Fit: Most importantly, a good broker ensures the policy you choose aligns with your long-term health requirements and financial strategy. They prevent dangerous gaps in coverage and deliver genuine peace of mind.

Ultimately, this methodical evaluation, guided by an expert, transforms the process from a speculative choice into a prudent investment in your health. It ensures the plan you select is not just a document, but a powerful asset you can rely upon.

Frequently Asked Questions

For those accustomed to a different healthcare system, navigating the UK's arrangements can generate numerous questions. We have compiled the most common queries from expatriates and high-net-worth individuals to provide clear, direct answers.

Do I Need Private Cover If I Can Use The NHS?

For the majority of our clients, the answer is an emphatic yes. The issue is not one of clinical quality—the NHS is excellent for true emergencies. The determining factor is time. The system is under immense strain, resulting in long, often unpredictable, waiting times for specialist appointments, diagnostic scans, and non-urgent surgeries.

Private cover is your mechanism to bypass those queues. It is about speed, choice, and control. You gain immediate access to top consultants and premier private hospitals on your schedule, with the level of privacy that is essential when managing a demanding career and personal life.

What Is The Core Difference Between PMI And IPMI Plans?

Consider it the difference between a domestic travel pass and a global passport.

Domestic Private Medical Insurance (PMI) is designed for a single jurisdiction: the UK. It is an excellent fit if you are permanently based here and do not travel extensively.

International Private Medical Insurance (IPMI), conversely, is engineered for a life that crosses borders. It provides global or regional cover, making it indispensable for expatriates, executives who travel frequently, or anyone who desires the freedom to seek treatment in another country. IPMI plans are typically far more comprehensive, often including high-value benefits such as medical evacuation and repatriation.

IPMI doesn't just cover you in one country; it provides a global safety net for elite medical care. It's healthcare that moves with you, aligning with a lifestyle that isn’t confined to a single post code.

How Do UK Insurers Handle Pre-Existing Conditions?

This is determined entirely by the type of underwriting you select when initiating the policy. There are two primary paths.

With 'moratorium' underwriting, any condition for which you have had symptoms, treatment, or advice in the recent past (usually the last 5 years) is automatically excluded for an initial period, typically two years. If you complete that two-year period without any flare-ups, treatment, or advice for that specific condition, it may then become eligible for cover. It is a "wait and see" methodology.

The alternative is 'full medical underwriting'. This is a much more transparent process. You provide your complete medical history upfront, and the insurer issues a clear, unambiguous decision on exactly what is and is not covered from day one. For any individual who values absolute certainty and wishes to avoid future surprises, this is always the superior route.

Navigating the premier tier of health insurance requires specialist expertise. At Riviera Expat, we act as your independent advocate, comparing elite plans to find the one that perfectly aligns with your global lifestyle and ensures your peace of mind. Schedule your complimentary consultation with Riviera Expat today.