Subrogation is a sophisticated financial mechanism within your health insurance policy, one that high-net-worth individuals should understand to appreciate its impact on their coverage and financial well-being.

In precise terms, subrogation is the legal right of your health insurer to pursue reimbursement from a third party who is legally liable for your injuries. Consider it a structured financial recovery process. Your insurer provides immediate liquidity to cover your medical expenses, then legally assumes your right to recover those funds from the responsible party. This ensures that the financial burden is correctly allocated without delaying your access to premier medical care.

Understanding the Subrogation Clause in Your Policy

Subrogation is a standard, non-negotiable clause in virtually every international private medical insurance (IPMI) policy. Its fundamental purpose is to maintain the financial integrity of the insurance system. Should another party's negligence—for instance, in a vehicular collision or a premises liability incident—result in significant medical costs, your insurer settles these expenses on your behalf.

The subrogation clause then contractually empowers your insurer to engage with the at-fault party's insurance carrier to recoup the exact amount expended on your medical treatment. This arrangement is advantageous, as it provides you with immediate access to necessary medical services without awaiting the conclusion of protracted legal proceedings.

The Financial Rationale Behind Subrogation

The core principle of subrogation is to prevent "unjust enrichment," commonly known as "double recovery." You cannot receive compensation for the same medical expenses from two different sources—once from your insurer and again from a settlement with the liable party.

Subrogation ensures that the ultimate financial responsibility is placed correctly. This practice also mitigates moral hazard by preventing individuals from profiting from an injury, which is critical for your insurer's risk management strategy. A clear understanding of the stakeholders is essential.

Key Stakeholders in the Subrogation Process

To fully grasp the mechanics of a subrogation claim, it is useful to delineate the roles of each entity involved following a liability incident.

| Party Involved | Role in the Subrogation Process |

|---|---|

| The Insured (You) | Receives immediate, high-quality medical care funded by your insurer and is contractually obligated to cooperate with the insurer's recovery efforts. |

| Your Insurer (e.g., IPMI Provider) | Disburses funds for your medical treatment and then initiates the subrogation process to seek full reimbursement from the liable third party. |

| The At-Fault Third Party | The individual or corporate entity determined to be legally responsible for causing the injury. Their liability insurance is the primary target for the recovery claim. |

| Third-Party's Insurer | The entity contractually obligated to reimburse your insurer for the medical costs if their policyholder is found liable. |

This structured process ensures financial accountability and systemic stability.

This financial recovery is increasingly critical. According to Swiss Re Institute's data, global non-life insurance claims saw a significant increase in recent years, compelling insurers to adopt more rigorous cost recovery strategies. For discerning expatriates, successful subrogation is instrumental in stabilizing premiums by offsetting escalating healthcare expenditures.

It is also important to recognize that certain contracts may include a waiver of subrogation, which fundamentally alters this dynamic. Mastering these distinctions is paramount, and further details can be found in our comprehensive guide to expat medical insurance policy terms explained.

How the Subrogation Process Actually Works

Subrogation is not an arbitrary action but a methodical sequence of events initiated under specific, legally defined circumstances. For example, if you sustain an injury in a traffic incident or a slip-and-fall at a commercial establishment where another party is demonstrably at fault, the subrogation process commences the moment your international private medical insurance (IPMI) provider disburses payment for your medical care.

The objective is unambiguous: to recover all funds from the entity legally responsible for your injury. This ensures the financial consequences are borne by the at-fault party, not by you or the broader pool of policyholders.

The Initial Investigation and Liability Assessment

Initially, your insurer's specialized recovery unit conducts a meticulous investigation. They systematically analyze the incident, compiling all relevant documentation to establish a definitive sequence of events. This involves a rigorous review of medical records, official incident reports, and any evidence that substantiates legal liability.

The objective is to construct an irrefutable case demonstrating that a third party's negligence was the direct and proximate cause of your injuries and the ensuing medical expenses. This phase is critical; without a robust case, a formal demand for reimbursement cannot be made to the at-fault party's insurer.

This is a significant financial sector. The global subrogation services market was valued at approximately USD 4.7 billion in 2023. This valuation is driven by the fact that substantial funds are often left unrecovered. Industry analyses indicate that up to 15% of relevant insurance claims are closed with missed subrogation opportunities, representing a multi-billion dollar loss. The average recovery timeline of six months underscores the complexity of these financial negotiations. You can gain further insight into the scale of subrogation detection and recovery on shift-technology.com.

Formal Communication and Your Role

Once your insurer has established liability with a high degree of confidence, they will formally notify you of their intent to pursue subrogation. Concurrently, they will issue a formal demand letter to the third party's insurance carrier, detailing the total medical costs covered on your behalf.

This letter initiates a series of often intricate negotiations between the two insurance carriers. Your cooperation during this phase is not merely beneficial—it is a contractual obligation under your policy.

You may be required to provide documentation, offer a detailed deposition regarding the incident, or execute legal forms that authorize your insurer to act on your behalf. This is analogous to providing information for pre-authorisation and direct settlement; your timely input facilitates a seamless process.

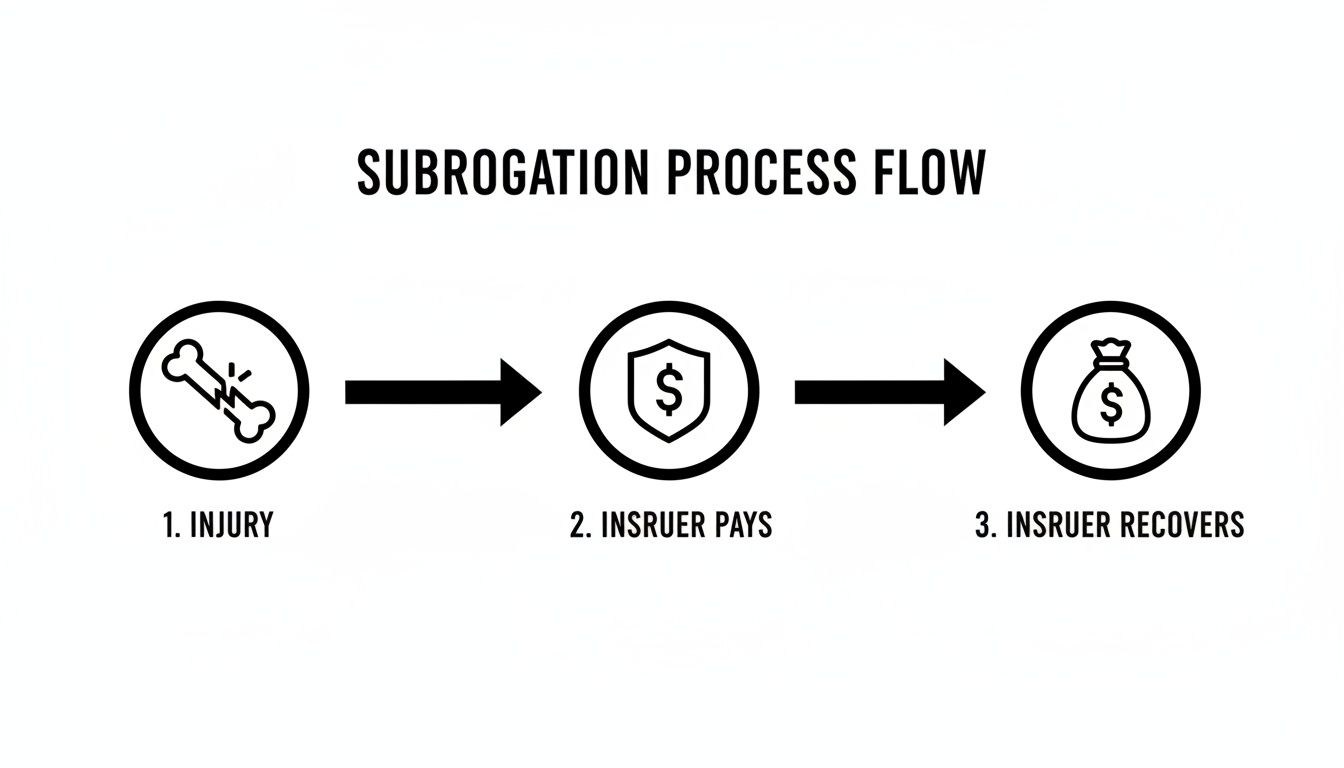

This flowchart illustrates the process, from the initial injury to the final recovery of funds.

As depicted, the critical sequence is that your insurer funds your medical care first. They only seek reimbursement from the responsible party after your health needs have been fully addressed.

Final Recovery and Claim Closure

The final stage involves negotiation and settlement. Your insurer’s legal or recovery department will negotiate to secure full reimbursement of the medical expenses paid. Upon receipt of payment from the third-party insurer, the subrogation file is formally closed.

The key takeaway is that this entire process operates in the background. While your cooperation is essential, your insurer manages the complex legal and financial negotiations, allowing you to focus exclusively on your recovery.

This sophisticated mechanism is a cornerstone of any prudently managed insurance plan, enforcing financial accountability and preserving the stability of the system for all policyholders.

Real-World Subrogation Scenarios for Global Citizens

While the definition of subrogation in health insurance is clear, its application in real-world scenarios for expatriates and high-net-worth individuals is often complex. These situations frequently involve multi-jurisdictional claims that extend beyond simple accidents.

Consider the following scenarios. In each case, your international private medical insurance (IPMI) provider prioritizes your care by covering all costs upfront. Subsequently, their recovery teams work diligently to ensure the financially responsible party is held liable.

The Skiing Incident in the Swiss Alps

Imagine you are enjoying a ski holiday in Verbier when a negligent skier collides with you, causing a severe leg fracture that requires immediate surgery and extensive rehabilitation.

Your IPMI policy performs as expected, covering the helicopter evacuation, surgery at a private clinic in Geneva, and all subsequent physiotherapy. The costs escalate into six figures, but your focus remains on recovery, not financial administration.

Simultaneously, your insurer's subrogation team commences its work:

- Evidence Compilation: They procure official ski patrol reports, witness statements, and complete medical documentation.

- Liability Establishment: The evidence unequivocally indicates the other skier's negligence. The team identifies the individual and their liability insurance provider.

- Recovery Initiation: Your insurer formally contacts the at-fault skier's insurance carrier, presenting a detailed claim for the €150,000 expended on your medical care.

This is a textbook example of subrogation. Your insurer is not seeking funds from you; they are exercising their legal right to recover costs from the party whose negligence caused the injury, expertly navigating Swiss liability statutes to do so.

The Commercial Venue Accident in Dubai

Consider another frequent scenario: you are attending a business conference at a five-star hotel in Dubai. You slip on a wet, unmarked floor, resulting in a serious spinal injury.

Your health remains the primary concern. Your IPMI covers the ambulance, hospitalization, diagnostic imaging, and specialist consultations, totaling $95,000. You receive exceptional care without any out-of-pocket expenditure.

Concurrently, the insurer’s recovery specialists understand that the hotel has a legal "duty of care." Their investigation confirms a breach of this duty, as staff failed to place warning signs—a clear instance of negligence.

Your insurer then initiates a subrogation claim against the hotel’s commercial general liability (CGL) insurance. This involves complex negotiations guided by UAE premises liability law. Your insurer manages the entire legal process, transferring the financial liability from your policy to the at-fault corporate entity.

These examples underscore a vital principle: Subrogation ensures the ultimate financial responsibility for an injury rests with the negligent party, not with the innocent policyholder or their insurance plan.

The Defective Medical Device in Singapore

Let us examine a more complex product liability case. You undergo a planned procedure at a premier hospital in Singapore. However, the implanted medical device fails due to a manufacturing defect, necessitating emergency revision surgery and a prolonged, costly hospitalization.

Your IPMI covers the substantial costs, which exceed $250,000. The cause of injury is not a simple accident but a defective product.

This triggers a sophisticated, multi-front subrogation action. Your insurer’s legal team will:

- Identify All Liable Parties: The chain of liability may include the device manufacturer, the distributor, and potentially the hospital if it had prior knowledge of device issues.

- Engage Technical Experts: They will likely retain engineers to conduct a forensic analysis of the failed device to prove the defect.

- Navigate International Product Liability Law: A single claim could involve legal counsel and statutes in Singapore (locus of incident), Germany (locus of manufacturing), and your country of domicile.

This is a formidable legal undertaking, far beyond the capacity of an individual to manage. Your insurer pursues it tenaciously because every dollar recovered contributes to the long-term stability and affordability of high-caliber insurance plans like yours.

Your Rights and Obligations During a Claim

When your insurer initiates a subrogation claim, your role transitions from that of a patient to a key participant in the recovery process. This is not an adversarial position; it is a collaborative effort defined by your policy terms. Understanding your responsibilities is critical for a favorable outcome that protects your financial interests.

The process is governed by a standard provision in most international private medical insurance (IPMI) policies known as the duty to cooperate. This clause obligates you to assist your insurer by providing a factual account of the incident, executing necessary legal documents, and forwarding any correspondence received from the at-fault party.

Your Duty to Cooperate

Cooperation is not merely a suggestion; it is a contractual obligation fundamental to a successful subrogation claim. Failure to comply may be construed as a breach of your policy terms. Your insurer relies on your firsthand account and documentation to construct a legally sound case against the liable party.

Your cooperation typically involves:

- Providing Accurate Information: Furnishing a truthful and comprehensive account of the incident leading to your injuries.

- Signing Authorizations: Executing documents such as a Subrogation Agreement or a Release of Information, which grant your insurer the legal authority to pursue the claim on your behalf.

- Forwarding Communications: Immediately informing your insurer of any direct contact from the third party or their insurance carrier and forwarding all related correspondence.

It is equally important to understand the limits of this duty. You are not expected to conduct investigations, negotiate with attorneys, or manage litigation. Those functions are the exclusive domain of your insurer’s recovery specialists. Your role is to provide the necessary support.

Understanding Your Fundamental Rights

While you have obligations, you also possess critical rights designed for your protection. The most significant of these is the legal principle known as the "made whole" doctrine. In many jurisdictions, this doctrine provides a powerful safeguard.

The "made whole" doctrine stipulates that your insurer cannot claim any portion of a settlement until you have been fully compensated for all your losses—not just the medical expenses they covered. This includes non-medical damages such as lost income, pain and suffering, and property damage.

This is a crucial distinction. If a settlement is insufficient to cover both your comprehensive losses and the insurer's medical lien, your right to be "made whole" takes precedence.

For example, if your total damages amount to $200,000, but the final settlement is only $150,000, your insurer may receive no reimbursement, as recovering their costs would prevent you from being fully compensated first.

When navigating subrogation following a personal injury claim, understanding the nuances of negotiating medical liens is essential to securing the best possible financial outcome.

Conversely, should you receive a payment from the at-fault party designated specifically for medical expenses that your insurer has already paid, you are obligated to reimburse your insurer. This prevents "double recovery" and maintains fairness. A clear understanding of your rights and duties empowers you to navigate the process with confidence while upholding your contractual commitments.

How Subrogation Impacts Your Insurance Premiums

While subrogation may appear to be a technical insurance term, it functions as a potent financial tool that directly benefits you. When an insurer successfully recovers costs from a liable third party, it has a direct, positive effect on the long-term stability and predictability of your insurance premiums.

When your insurer pays a claim, that amount is recorded as a loss. However, if those funds are recovered through subrogation, the loss is effectively erased from their financial statements. This improves their loss ratio—the critical metric comparing claims paid out to premiums collected. A healthy, stable loss ratio is the foundation of any prudently managed insurance plan.

The Link Between Recovery and Premium Stability

This financial discipline enables premier international private medical insurance (IPMI) providers to offer superior benefits without imposing exorbitant price increases. Without the ability to pursue subrogation, the immense costs arising from third-party negligence would be socialized across the entire pool of policyholders.

This would inevitably result in higher, more volatile premiums for all clients. Insurers proficient in subrogation are better equipped to forecast their financial liabilities, creating a more sustainable and predictable pricing environment.

In essence, every dollar an insurer recovers through subrogation is a dollar that does not need to be offset by future premium increases. This practice helps insulate your policy from the financial impact of claims that are not your fault.

A Proactive Approach to Cost Containment

Subrogation is a proactive form of cost containment. By ensuring that financially responsible parties are held accountable, insurers actively counteract the inflationary pressures driving up healthcare costs. This is particularly vital for international plans, where medical expenses can be substantial and unpredictable.

This disciplined approach allows your insurer to:

- Mitigate Rising Costs: By recovering significant claim expenditures, subrogation helps moderate the rate of premium increases.

- Maintain Comprehensive Benefits: A stronger financial position enables the insurer to continue offering the high-level, comprehensive benefits you expect, without compromising on quality.

- Ensure Long-Term Viability: A robust recovery program enhances the insurer's overall financial strength, providing you with the assurance that your coverage will be reliable when you need it most.

Ultimately, an effective subrogation clause is an indicator of a well-managed insurance company. It demonstrates a commitment to financial prudence that benefits every client. For a more detailed analysis of premium determinants, please refer to our guide on why medical insurance premiums rise year after year. This sophisticated, behind-the-scenes process is one of the many ways a top-tier insurer works to protect both your health and your financial portfolio.

Common Questions About Health Insurance Subrogation

Following an injury, clarity is paramount. Subrogation often raises practical questions. We will now address the most frequent inquiries from our clients to ensure you can navigate the process with confidence.

Will I Have to Pay Money Back if My Insurer Subrogates?

No, you will not be required to reimburse your insurer from your personal funds. Subrogation is a process by which your insurer recovers its expenditures from the at-fault party's insurance carrier. The objective is to prevent the duplicate payment of medical bills.

Consider a settlement from the liable party. It is typically allocated into categories. Funds designated for non-medical damages, such as pain and suffering, belong to you exclusively. However, if a portion of the settlement is explicitly allocated for medical bills—expenses your insurer has already covered—you are contractually obligated to remit that specific amount to them.

What Happens if the At-Fault Party Is Uninsured?

This presents a challenge for your insurer, but not for you. While they may attempt to recover funds directly from the uninsured individual's personal assets, a successful recovery is often unlikely if the person lacks significant assets.

The critical point is that this contingency does not impact your coverage. Your medical expenses will be paid by your policy as contracted. This scenario underscores the importance of subrogation; successful recoveries from insured parties help maintain premium stability for the entire client base.

Can I Refuse to Cooperate With My Insurer?

This course of action is strongly discouraged. Refusing to cooperate with your insurer’s subrogation efforts constitutes a breach of your policy. Nearly every insurance contract contains a cooperation clause, which legally obligates you to provide information and execute documents necessary for pursuing the claim.

Non-compliance could lead to severe consequences. At a minimum, your insurer could legally demand that you reimburse them for the medical costs they have paid. In a worst-case scenario, it could jeopardize your future coverage. It is always in your best interest to cooperate fully. Engaging a trusted advisor ensures the process is managed correctly, protecting both your financial interests and your relationship with your insurer.

Navigating the complexities of international private medical insurance requires expert guidance. The team at Riviera Expat provides the clarity and support needed to secure a policy that aligns perfectly with your global lifestyle, ensuring you are protected no matter where you are. Get a free expert consultation today at riviera-expat.com.