For high-net-worth individuals establishing a presence in Thailand, securing the right medical insurance is not merely an administrative task—it is a critical component of a comprehensive wealth preservation strategy. The decision typically comes down to two distinct options: a standard local policy, often fraught with limitations, or a sophisticated International Private Medical Insurance (IPMI) plan engineered for a global lifestyle.

Securing Premier Healthcare in Thailand

For executives, entrepreneurs, and global citizens residing in Thailand, medical insurance should be viewed as a core element of your asset protection framework. Your health, and the ability to access world-class care without hesitation, is an invaluable asset. The policy you select must adhere to the same exacting standards you apply to every other facet of your life.

Thailand is renowned for its outstanding private hospitals, such as Bumrungrad International and Bangkok Hospital. However, accessing this elite tier of care, particularly for a serious or chronic condition, can carry a formidable price tag. A standard local insurance plan can quickly prove inadequate, often encountering restrictive coverage caps or confining you to a network that does not extend beyond Thailand's borders.

The Strategic Advantage of Global Coverage

For any professional whose career and personal life are not confined to a single country, a purely local healthcare plan represents a significant strategic miscalculation. This is where International Private Medical Insurance (IPMI) becomes essential, and the distinction is profound. It is the difference between a local library card and a global access pass; one grants entry to a limited area, while the other opens the entire world.

An IPMI plan is specifically engineered to deliver:

- Geographic Freedom: True peace of mind with comprehensive coverage not just in Thailand but anywhere your business or personal life may take you. It ensures your care is seamless, whether you are on a business trip or relocating.

- Unrestricted Access: The power to choose from a vast network of the best hospitals and specialists, both in Thailand and internationally. You can learn more about why extensive medical networks are so crucial for your care.

- Superior Financial Protection: Substantially higher annual limits—often with no cap at all—that act as a firewall, protecting your personal wealth from the potentially devastating financial fallout of a major medical event.

Choosing the right health insurance is not just another expense—it is an investment in certainty. It guarantees that when a crisis occurs, your sole focus remains on recovery, not on the financial implications, geographic borders, or the quality of available care.

Ultimately, your decision must align with your international reality. For the discerning professional in Thailand, an IPMI policy offers the assurance that comes from knowing your health is protected by a plan as sophisticated and mobile as you are. This guide will delineate the key differences to help you make a truly informed choice.

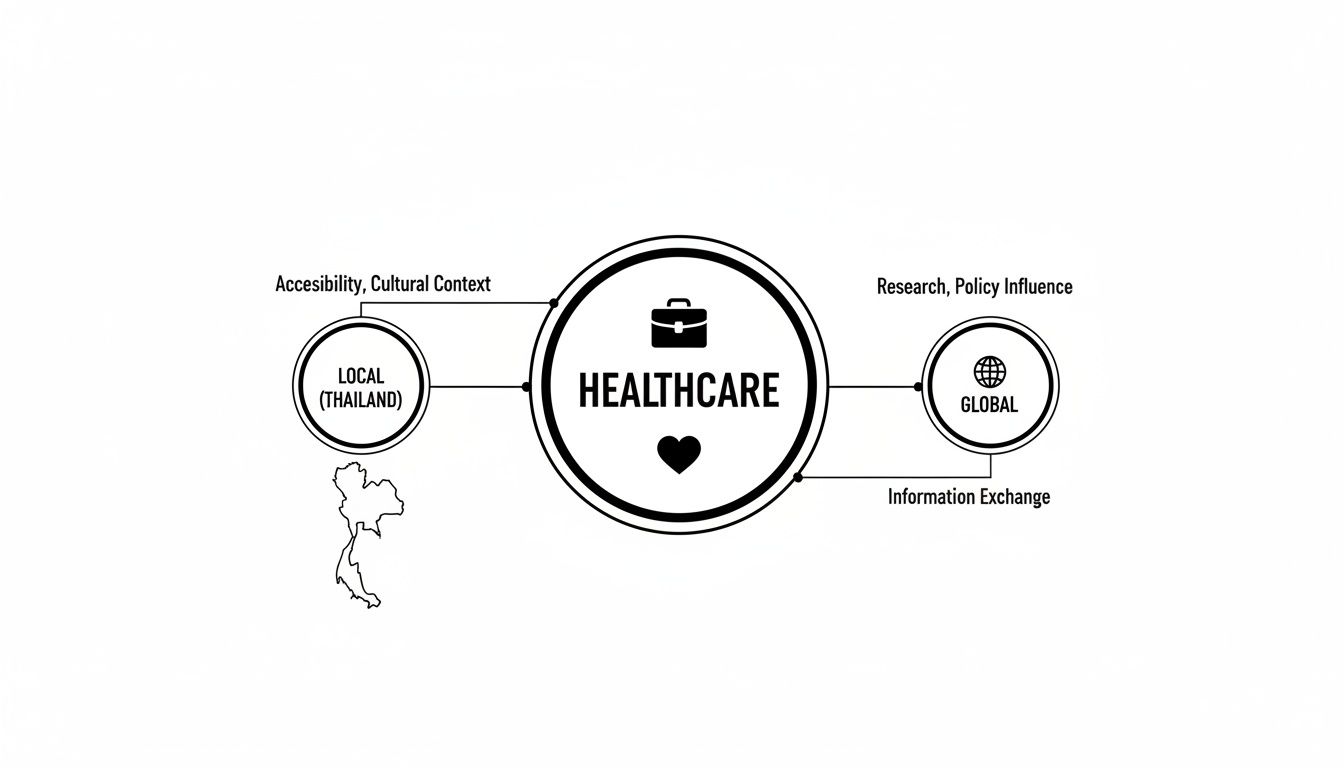

Comparing Local Plans and Global IPMI

When evaluating medical insurance options in Thailand, you will encounter two fundamentally different frameworks: local Thai plans and global International Private Medical Insurance (IPMI). Making the correct selection is not merely about cost; it is a strategic decision. You are choosing between a solution built for a single location and one designed for a life without borders.

This simple diagram illustrates the core difference. It shows how local healthcare operates as a contained system, whereas a global approach provides access and flexibility far beyond Thailand's jurisdiction.

For an internationally mobile professional, that worldwide access is not a luxury—it is a necessity.

The Architecture of Local Thai Plans

Local Thai insurance plans are precisely what their name implies: policies constructed for individuals whose healthcare needs remain within the country. They are often more budget-friendly, but this comes with significant limitations that can be untenable for a high-net-worth expatriate.

Consider these inherent constraints:

- Geographic Restriction: Coverage ceases at the border. Should you require medical care during international business travel or a family holiday, you would be without cover.

- Defined Network Access: You are typically restricted to a specific list of hospitals. This list may not include the premier international facilities you would prefer, such as Bumrungrad or Bangkok Hospital.

- Lower Coverage Limits: Local plans often feature low annual caps. A serious accident or a complex illness could exhaust these limits rapidly, leaving your personal assets exposed to substantial medical bills.

These plans serve a purpose, but for an executive whose life and work transcend national borders, they represent a considerable liability. They lack the scope required for genuine peace of mind.

The Global Standard: International Private Medical Insurance

On the other side of the spectrum is IPMI. It is the gold standard for global citizens, and for sound reason. To use an analogy: a local plan is a library card for one town, while IPMI is a pass that grants you access to every major library in the world. IPMI is an entirely different class of asset, built for portability and premium service.

The demand for this level of protection is growing substantially. The Thailand health insurance market was valued at USD 2.89 billion in 2023 and is projected to reach USD 4.71 billion by 2032, growing at a CAGR of 5.6%. This is unsurprising when considering that medical inflation in Thailand has recently been estimated at 13.5%. Discerning expatriates recognize this trend and demand the flexibility of a true international plan. For a deeper dive, read our comprehensive guide on international private medical insurance.

IPMI is built on a simple but powerful principle: your access to top-tier healthcare should not depend on your GPS coordinates. It provides continuity of care, regardless of where life or work takes you.

The advantages of a premium IPMI plan are transformative:

- Worldwide Portability: Your coverage accompanies you everywhere. This is non-negotiable for anyone who travels internationally.

- Extensive Global Networks: You gain access to a vast, worldwide network of elite hospitals and specialists. This provides the freedom to choose the best care available, anywhere on the planet.

- Significantly Higher Coverage Limits: We are referring to multi-million-dollar annual limits, with many top-tier plans offering effectively uncapped coverage. This ensures even the most advanced and expensive treatments are fully funded.

- Premium Services: Features such as international medical evacuation, direct cashless billing with hospitals worldwide, and 24/7 multilingual support are standard. It is a white-glove service experience that aligns with the expectations of a successful professional.

The table below breaks down the key differences at a glance, making the choice clearer.

Local Thai Insurance vs. International IPMI At a Glance

| Feature | Local Thai Medical Insurance | International Private Medical Insurance (IPMI) |

|---|---|---|

| Geographic Coverage | Typically Thailand only. | Global, including your home country and Thailand. |

| Annual Limits | Lower (e.g., THB 1-5 million). | Very high (e.g., USD 2-5 million or unlimited). |

| Hospital Network | Restricted to a specific list of local hospitals. | Extensive global network of top-tier hospitals. |

| Direct Billing | Usually limited to network hospitals in Thailand. | Widespread cashless access at hospitals worldwide. |

| Premium Services | Basic. Evacuation is rarely included. | Comprehensive (medical evacuation, 24/7 support). |

| Portability | Policy is tied to Thailand; not portable. | Fully portable as you move between countries. |

| Ideal For | Locals or long-term residents who do not travel. | Expatriates, frequent travellers, and global citizens. |

Ultimately, choosing between a local plan and a global IPMI policy is a strategic decision. It comes down to one question: is your health protection a localised utility, or is it a global asset designed to match your international footprint? For most executives and expatriates, the answer is self-evident.

Analyzing Critical Coverage Details

Once you have grasped the fundamental differences between insurance plans, it is time to examine the specifics. This is where you determine if a policy is merely a document or a genuine shield against catastrophic medical costs. For any discerning professional, the true value of a policy lies not in its price, but in the fine print that guarantees your financial security.

At the core of any robust policy are its inpatient and outpatient benefits. Inpatient care encompasses any treatment requiring hospital admission, such as major surgery or an extended stay for a serious illness. Outpatient care covers all other services: physician consultations, diagnostic tests, and prescriptions.

Local Thai plans often impose frustratingly low limits on both. In contrast, a top-tier IPMI policy will typically provide comprehensive, often unlimited, coverage for these essentials.

This distinction is absolutely critical. Imagine you require a complex cardiac procedure at a world-class facility like Bumrungrad International Hospital. The cost can easily run into the millions of baht. A plan with insufficient inpatient limits would leave you facing a massive financial shortfall, entirely defeating the purpose of having insurance.

Specialized Coverage for Uncompromising Protection

Beyond the basics, a truly superior insurance plan distinguishes itself with specialized benefits designed to handle worst-case scenarios. These are the features that provide peace of mind, knowing every eventuality is covered.

Key benefits to look for include:

- Chronic Condition Management: This ensures ongoing, long-term care for conditions like diabetes or hypertension is fully covered. Many standard policies either exclude this or cap the benefits severely.

- Advanced Cancer Treatments: You gain access to the latest therapies—chemotherapy, radiotherapy, immunotherapies—which can be prohibitively expensive without proper coverage.

- International Medical Evacuation: This is non-negotiable. It guarantees you can be transported to the nearest center of medical excellence, anywhere in the world, if local facilities cannot provide the required care.

- Comprehensive Maternity Benefits: This covers everything from prenatal consultations to delivery and postnatal care at the best facilities, ensuring a healthy start for your family.

The essence of a premium IPMI plan is not just to pay for treatment, but to remove all barriers to accessing the best possible care, wherever it may be. It is a tool for absolute risk management, ensuring a medical crisis never becomes a financial one.

Of course, it is equally important to understand what is not covered. It is imperative to review the policy documents meticulously. For a deeper understanding, it is helpful to be aware of the common medical conditions and policy exclusions that can present unforeseen challenges.

Real-World Value: A High-Stakes Scenario

Let us make this tangible. Consider an executive in Bangkok who develops a severe neurological condition. The top physicians in Thailand recommend a highly specific surgical procedure, but the world's leading expert is based in Singapore.

Here is how different insurance plans would respond:

- With a Local Thai Plan: The policy would almost certainly deny coverage for treatment outside Thailand. The executive would be faced with a difficult choice: accept adequate care locally or pay hundreds of thousands of dollars out-of-pocket for superior treatment abroad.

- With a Premier IPMI Policy: The outcome is entirely different. The plan's global network and medical evacuation benefit would activate seamlessly. It would cover the consultation with the Singaporean specialist, the surgery itself, and all associated travel and accommodation costs. The focus would be entirely on recovery, not on the staggering bill.

This scenario is not merely hypothetical; it demonstrates the real, high-stakes value of a truly international plan. It transforms insurance from a simple payment mechanism into a powerful logistical and financial tool that guarantees access to the best healthcare the world has to offer. When evaluating any Thai medical insurance policy, ask yourself: does it provide that level of certainty?

Understanding Costs, Premiums, and Value

When evaluating top-tier medical insurance in Thailand, it is easy to focus solely on the premium. However, it is crucial to reframe this cost not as a monthly expense, but as a strategic investment in your financial security and peace of mind.

An International Private Medical Insurance (IPMI) policy is fundamentally different from a standard local plan, and its pricing reflects this. The cost is a direct result of the comprehensive, global access and high-touch service it provides.

Several key variables directly influence the premium you will pay. Understanding these allows you to tailor a policy that precisely fits your lifestyle and risk tolerance, ensuring you are not paying for protection you will never use.

Key Factors That Shape Your Premium

The premium for a world-class medical plan is not an arbitrary figure. It is calculated based on a handful of specific risk factors and the exact level of coverage you choose, which puts you firmly in control of the final cost.

The main drivers include:

- Your Age: This is a primary factor. Statistically, the likelihood of requiring medical care increases with age. Insurers structure premiums in age bands, which typically adjust every five years.

- Area of Coverage: Insurers offer different geographical zones. A policy covering only Southeast Asia will be more affordable than one providing worldwide coverage. The most significant price increase occurs when adding the USA, due to its exceptionally high healthcare costs.

- Deductible Level: A deductible (also known as an excess) is the amount you agree to pay out-of-pocket before the insurer begins to cover costs. Opting for a higher deductible can significantly reduce your annual premium, making it one of the most effective tools for managing costs.

- Chosen Benefits: Core coverage for hospital stays and outpatient visits forms the foundation. From there, you can add optional modules for services like dental, vision, wellness check-ups, and maternity care. Each addition will adjust the premium accordingly.

Think of an IPMI premium as an investment in unparalleled access and service. It's designed to shield your assets from the multi-million baht bills that come with major medical events at elite hospitals like Bumrungrad International or Bangkok Hospital. Suddenly, insurance becomes a vital financial planning tool.

Value Beyond the Price Tag

The true value of a premium IPMI policy becomes evident when you contrast its cost with the potential financial ruin of a single serious medical event. Local health riders attached to life insurance policies are common in Thailand, but discerning professionals are quickly discovering their limitations.

Recent industry data shows these health riders generated premiums of THB 61.22 billion (approximately USD 1.7 billion) in the first half of 2023, a figure largely driven by escalating medical costs. The issue is that these local plans often have strict residency requirements and geographical limits that are incompatible with a global lifestyle. You can read more about the growth and trends in the Thai insurance market to see the bigger picture. This reality check is precisely why investing in a robust, portable IPMI plan is the more prudent long-term strategy.

Ultimately, the cost of premier Thai medical insurance is a direct reflection of the security it provides. It ensures your focus can remain on your health and recovery, not on negotiating with a hospital's billing department or worrying about exceeding your coverage limit. By carefully selecting your coverage area, deductible, and benefits, you can construct a plan that delivers exceptional value and the freedom that comes with true peace of mind.

Navigating the Application and Underwriting Process

Once you have selected a potential policy, you will encounter a critical step known as underwriting. This is the process where the insurer assesses your health profile to determine the precise terms of your coverage. For busy professionals, this can seem like a bureaucratic formality, but understanding its function makes it a clear and manageable path to securing protection.

Think of it as the insurer's due diligence. The entire process is predicated on one core principle: full and transparent disclosure. During the application, you will be asked to provide a detailed medical history. Attempting to conceal pre-existing conditions is a grave error. It can lead to denied claims or, in the worst-case scenario, the cancellation of your policy when you need it most. Honesty is not just best practice; it is the foundation of your insurance contract.

Full Medical Underwriting vs Moratorium

Insurers in Thailand generally use one of two methods to assess your application, and the choice has significant implications for how they handle past health issues.

- Full Medical Underwriting (FMU): This is the most common and thorough approach. You complete a detailed health questionnaire, providing the insurer with a comprehensive picture of your medical history from the outset. This upfront clarity ensures you know exactly what is covered and what is excluded from day one. There are no surprises.

- Moratorium Underwriting: This path is simpler initially as it does not require a full medical declaration. However, it comes with a major caveat. Any pre-existing conditions you have had in the last five years are automatically excluded until you complete a set period (usually 24 months) without symptoms, treatment, or advice for that specific condition.

While a moratorium may seem faster, FMU provides certainty, which is invaluable. For high-net-worth individuals who require clarity and control, knowing the precise terms of your coverage from the beginning is always the superior strategic choice.

Understanding Potential Underwriting Outcomes

After you submit your application under Full Medical Underwriting, the insurer’s team will review your history and provide a decision. This is not a simple "yes" or "no"—there are several possible outcomes, and an expert broker can often negotiate these on your behalf.

The purpose of underwriting is not to deny coverage; it is to accurately price the risk. A skilled broker can communicate directly with the underwriting team to advocate for the most favorable terms, ensuring your specific health situation is evaluated fairly.

Your application will likely result in one of three main outcomes:

- Full Coverage at Standard Terms: The ideal scenario. If you have a clean bill of health, the insurer accepts your application without any modifications or additional costs.

- Coverage with an Exclusion: If you have a specific pre-existing condition, the insurer might offer a policy that covers everything except issues related to that one condition.

- Coverage with a Premium Loading: The insurer agrees to cover your pre-existing condition but will add a surcharge to your premium to compensate for the higher associated risk.

This is where working with a specialist brokerage provides a distinct advantage. They can present your medical profile to several insurers simultaneously to determine which one will offer the best terms. This transforms a potentially frustrating process into a streamlined negotiation that secures the optimal Thai medical insurance plan for you.

Choosing Your Ideal Thai Medical Insurance Partner

Making the final decision on your health insurance in Thailand is the last and most critical piece of the puzzle. This is not simply a transaction; it is about selecting a long-term partner who will advocate for your best interests. The firm you choose will determine the quality of advice you receive and the level of support you can expect when you need it most.

Attempting to navigate this landscape alone, or with a generalist agent, is a significant risk. You might achieve a marginal cost saving upfront, but you could pay for it later in suboptimal coverage and poor advice. A generalist simply lacks the deep market knowledge required to secure the best terms, particularly when dealing with the complexities of underwriting for pre-existing conditions.

The Brokerage Advantage

The most effective strategy is to partner with a specialized, independent insurance brokerage. Unlike a captive agent from a single insurance company who is limited to their own products, a specialist broker works for you. Their sole objective is to provide unbiased, expert guidance tailored to your unique circumstances.

For any discerning professional, this approach offers several non-negotiable benefits:

- Objective Advice: A broker has no allegiance to any single insurer. Their loyalty is to you, the client. This ensures their recommendations are based purely on your needs, not on fulfilling a sales quota.

- Market Access: They provide a comprehensive comparison of plans from all top-tier global insurers. You receive a complete, unbiased view of the entire market, not just a single provider's offerings.

- Underwriting Negotiation: This is where a true specialist demonstrates their value. They have established relationships with underwriting teams and can negotiate directly on your behalf to secure the best possible terms, even with a complex medical history.

- Ongoing Claims Support: The relationship does not end after the policy is in place. A dedicated broker acts as your advocate during the claims process, ensuring it is as smooth and efficient as possible.

Working with a specialist brokerage fundamentally changes the dynamic. It elevates the process from a simple transaction to a strategic partnership. You gain clarity and confidence, knowing your insurance is a solid pillar of your financial plan, managed by an expert who understands your world.

The final step is straightforward. By engaging a specialist for a complimentary consultation, you gain access to this expertise with no obligation. It is the most efficient way to develop a clear, actionable plan, allowing you to move forward with confidence that your choice of Thai medical insurance is the right one.

Burning Questions Answered

When dealing with premier medical insurance in Thailand, the stakes are high, and the questions that arise are specific and important. For successful professionals, obtaining clear, direct answers is essential before making a commitment. Here are the straightforward answers to the questions we encounter most frequently.

Is My Corporate Health Plan Sufficient in Thailand?

Relying solely on your company's health plan can be a significant oversight. That coverage is tied directly to your employment. The moment you change roles, begin consulting, or decide to retire, it ceases to exist, leaving a critical gap in your protection precisely when you might need it most.

Furthermore, most corporate plans are designed to meet the company's budget, not your ultimate security. This often translates to lower coverage limits, restricted access to premier hospitals, and inadequate or non-existent global coverage—a critical flaw for anyone living an international life. A personal IPMI policy serves as your true safety net. It provides continuous, superior coverage that you control, entirely independent of your employer. That is genuine peace of mind.

Can I Obtain Coverage for My Pre-Existing Conditions?

Yes, it is often possible, but this is where the process becomes nuanced and professional advice is invaluable. How an insurer addresses a pre-existing condition is determined by their specific underwriting guidelines.

The most common process is Full Medical Underwriting (FMU). You will provide your complete health history, and the insurer will respond with one of several decisions:

- They may cover you but exclude that specific condition.

- They may agree to cover the condition but at a higher cost (premium loading).

- If the condition is minor and well-managed, they might offer full coverage at the standard price.

Another option is moratorium underwriting. With this method, you do not declare your medical history upfront, but the policy automatically excludes any condition for which you have had symptoms or treatment in the last five years. This exclusion is only lifted after you complete a set period, typically 24 consecutive months, without any symptoms or treatment for that condition. A skilled broker is critical here; they know which insurers have more favorable guidelines for specific health profiles and can navigate the process to avoid declined applications.

What Are the Health Insurance Requirements for Thai Visas?

This is a detail you cannot afford to overlook. Thailand mandates health insurance for certain long-stay visas. For instance, applicants for the Non-Immigrant O-A (retirement) visa must have a policy with a minimum of THB 3,000,000 (approximately USD 80,000) in medical coverage.

The Long-Term Resident (LTR) visa program has its own set of stringent insurance requirements. It is absolutely vital that your policy meets or, preferably, exceeds these government minimums. Any premium IPMI plan will easily satisfy these stipulations, and the best insurers for expatriates provide the precise documentation needed to ensure your visa application process is seamless and successful.

How Does a Claim Actually Work with IPMI?

A seamless claims process is a hallmark of premium IPMI providers. The entire system is designed to remove financial stress so you can focus solely on your recovery.

For any inpatient treatment at a major hospital within their network, such as Bumrungrad International or Samitivej Hospital, the process is almost always cashless. The hospital communicates directly with your insurer for pre-authorization and payment. You will not be required to pay upfront for your approved medical care.

For outpatient services, like consulting a specialist or undergoing a lab test, the standard procedure is to pay first and submit a claim for reimbursement. Insurers facilitate this with user-friendly online portals or mobile apps, and reimbursement is typically processed within a few business days. One of the most significant advantages of using a dedicated broker is having an expert on your side to resolve any claim issues, ensuring the process remains entirely stress-free for you.

At Riviera Expat, we bring clarity and expert guidance to help you choose a premier IPMI policy that's a perfect match for your life in Thailand. We invite you to secure your complimentary consultation and build a healthcare strategy you can be confident in.