Consider your life, health, and disability insurance policies as your financial bedrock—the core foundation upon which your wealth is built. But what is the contingency for a sudden, catastrophic accident? This is the precise scenario for which Supplemental Accidental Death & Dismemberment (AD&D) insurance is engineered. It is not a replacement for your core policies; it is a highly specific reinforcement designed for a narrow but devastating set of circumstances.

The Role of Supplemental AD&D Insurance

For high-net-worth individuals and discerning professionals, particularly those operating internationally, understanding what supplemental AD&D insurance is is not an academic exercise—it is a critical component of sophisticated risk management. It functions as a targeted financial instrument that delivers a significant, lump-sum cash benefit at the precise moment it is most needed: immediately following a severe, life-altering accident.

Its function is brutally simple and precise. It pays out only for accidental death or a catastrophic injury resulting in dismemberment, such as the loss of a limb or eyesight. It does not cover death from illness or natural causes. This sharp focus is its greatest strength.

To put its role into perspective, let's examine its core features.

Here's a breakdown of what this coverage entails:

Supplemental AD&D at a Glance

| Attribute | Description |

|---|---|

| Coverage Trigger | A covered accident resulting in death or a specific catastrophic injury (dismemberment). |

| Benefit Payout | A significant, pre-determined lump-sum cash payment. |

| Purpose | Provides immediate liquidity to cover unforeseen costs without disrupting long-term assets. |

| Relationship to Other Policies | Supplements life and disability insurance; it does not replace them. |

| Typical Beneficiary | Policyholder (for dismemberment) or their designated beneficiaries (for accidental death). |

| Common Exclusions | Death or injury from illness, natural causes, suicide, or specifically excluded high-risk activities. |

This table illustrates how AD&D carves out a very specific niche within a comprehensive financial protection strategy.

A Strategic Tool for Asset Protection

For executives with demanding global travel schedules or individuals with active lifestyles, the risk of a serious accident, while statistically low, carries devastating financial consequences. A supplemental AD&D policy is designed to plug this specific vulnerability in your financial armor.

A sudden, severe accident can completely derail even the most carefully constructed financial plans. Supplemental AD&D provides an immediate capital injection, allowing your primary assets and investments to remain untouched while your family handles the crisis.

This injection of capital ensures that your estate plans and legacy objectives are not compromised. The funds can cover immediate costs—from medical bills your health insurance may not cover to estate settlement fees—without forcing your family into a distressed sale of properties or investments.

Many employers offer this coverage as a remarkably cost-effective voluntary benefit. A significant advantage is its guaranteed acceptance, meaning enrollment typically requires no medical examinations. With average costs ranging from just $0.50 to $2.00 per $1,000 of coverage per month, it is an incredibly efficient method for adding a powerful layer of protection. You can learn more about the value of AD&D insurance as an employee benefit for a deeper analysis. This makes it an intelligent component of a personal risk management strategy, particularly for those whose lifestyles or professions expose them to a higher probability of accidents.

How Benefit Structures and Payouts Work

To fully appreciate the utility of supplemental AD&D, one must understand its payout mechanics. Unlike insurance policies that can be buried in complex calculations, AD&D is refreshingly direct. The entire structure hinges on two key concepts: the principal sum and the benefit schedule.

Consider the principal sum as the policy's total face value. This is the maximum payout, reserved for the most severe outcome: an accidental death. If the insured person dies in a covered accident, their beneficiaries receive 100% of the principal sum. It is that straightforward.

The Dismemberment Benefit Schedule

For severe, life-altering injuries that are not fatal, the dismemberment benefit schedule comes into play. This is not a single number but a detailed list that assigns a specific percentage of the principal sum to different types of catastrophic injuries.

This is sometimes referred to as the capital sum, but it is more accurately described as a schedule than a singular amount.

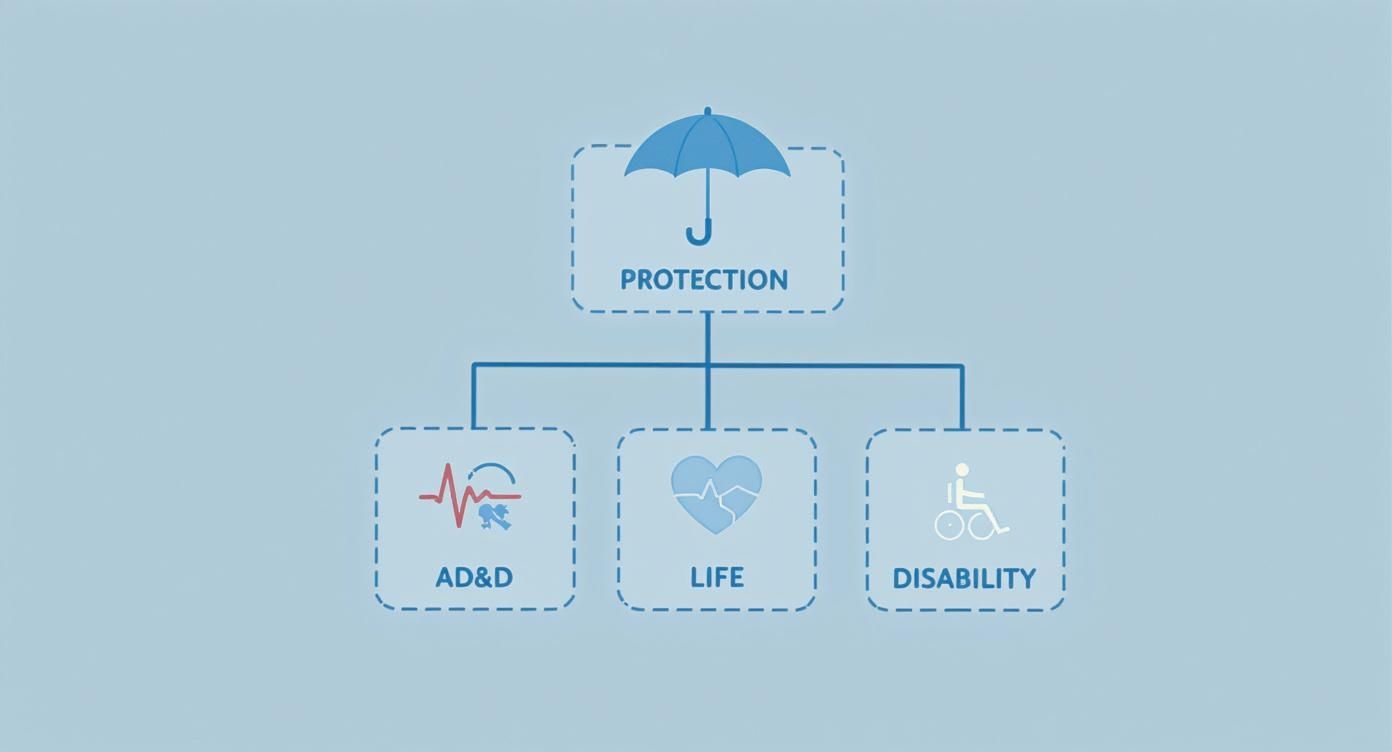

This diagram helps visualize where AD&D is positioned. It is a specialized instrument for accidents, working alongside the broader protection offered by life and disability insurance.

As illustrated, AD&D is not intended to replace life or disability coverage—it complements them by providing a significant financial buffer specifically for accident-related events.

Every policy’s schedule will have slight variations, which is why a thorough review of the policy document is non-negotiable. However, the general structure is quite consistent. For instance, the loss of two limbs is often considered so catastrophic that it triggers the same payout as an accidental death—100% of the principal sum.

A policy's benefit schedule is its foundational document. It removes ambiguity by assigning a clear, specific monetary value to a range of devastating injuries, ensuring you know exactly what financial support will be available.

Imagine a financial professional on an overseas assignment who is involved in a serious motor vehicle accident. Their supplemental AD&D policy would respond based on this schedule. An accidental death would pay out 100% of the policy's value. If they survived but lost both hands, the policy would almost certainly pay out the full 100%. The loss of a single hand, however, would typically trigger a 50% payout. Vehicle and workplace accidents are a significant driver of these claims. You can explore more details on typical AD&D payout schedules to see how these are structured.

Payout Scenarios in Practice

To make this concept perfectly clear, let's use a hypothetical schedule for a policy with a $2 million principal sum:

- Accidental Death: $2,000,000 (100%)

- Loss of Both Hands or Both Feet: $2,000,000 (100%)

- Loss of Sight in Both Eyes: $2,000,000 (100%)

- Loss of One Hand or One Foot: $1,000,000 (50%)

- Loss of Sight in One Eye: $1,000,000 (50%)

- Loss of Thumb and Index Finger on One Hand: $500,000 (25%)

This fixed-benefit approach provides absolute clarity. It allows you to quantify the exact financial safety net your policy provides for specific, life-altering events, leaving no room for guesswork when you require support the most.

Distinguishing AD&D From Life and Disability Insurance

For astute investors and high-net-worth expatriates, a common point of confusion is determining precisely where supplemental AD&D insurance fits into a robust personal protection plan.

The key is to cease thinking of these policies as competitors. They are not. They are highly specialized financial tools, each designed to neutralize a very specific and different kind of risk. Think of them as different instruments in a surgeon's kit—each is precise, non-interchangeable, and absolutely critical for its intended purpose.

Let's draw sharp, clear distinctions between AD&D, traditional life insurance, and disability income insurance. Understanding this is fundamental to strategic financial planning, ensuring you do not leave dangerous gaps in your safety net.

AD&D Versus Life Insurance: The Distinction Is the Cause of Death

The single most important distinction is the coverage trigger—the event that prompts the payout.

A traditional life insurance policy is your broad financial backstop. It pays a death benefit for nearly any cause, whether it is an illness, a chronic disease, or natural causes. Its purpose is to secure your beneficiaries' financial future, regardless of how your life ends.

Supplemental AD&D, by contrast, is a precision instrument. It pays out only if death is the direct result of a covered accident. This policy is constructed for the specific, catastrophic shock of an accidental fatality. It will not pay a single dollar for a death caused by cancer, a heart attack, or any other illness.

Think of life insurance as a wide-angle lens, capturing almost any cause of death. Supplemental AD&D is a powerful telephoto lens, zeroed in exclusively on the narrow, high-impact scenario of a fatal accident.

This intense focus is precisely why AD&D is a supplement. It is not meant to replace the foundational security of a comprehensive life insurance policy; it adds a potent layer of protection against a particular kind of sudden, unexpected financial trauma.

AD&D Versus Disability Insurance: A Lump Sum vs. an Income Stream

The difference between AD&D and disability income insurance is equally stark. Here, the defining factor is the nature and purpose of the payout.

Disability insurance is designed to replace your income. If an injury or illness prevents you from working, it provides a steady, ongoing stream of payments—usually monthly—to cover your living expenses while you recover. Its scope is broad, covering everything from a debilitating back injury to a serious illness that puts you out of commission for months or years.

Supplemental AD&D performs a completely different function. It delivers a one-time, lump-sum payment for a catastrophic, permanent injury specified in the policy, such as the loss of a limb, sight, or hearing. It is not designed to replace income during a temporary recovery. It is a massive capital injection intended to cover the immediate and staggering long-term costs of a life-altering event.

To fully grasp how these policies are structured, it's worth taking a moment to review common expat medical insurance policy terms explained in more detail.

This distinction is critical. AD&D provides immediate, substantial liquidity to handle enormous, unforeseen capital costs. Disability insurance protects your regular, ongoing cash flow. Each policy solves a completely different financial problem that can arise from a health crisis.

Comparing AD&D, Life, and Disability Insurance

To make the differences unequivocally clear, let's break them down side-by-side. Each policy has a distinct role within your overall financial protection strategy.

| Feature | Supplemental AD&D | Life Insurance | Disability Insurance |

|---|---|---|---|

| Primary Trigger | Death or specific catastrophic injury caused by a covered accident. | Death from nearly any cause (illness, accident, natural causes). | Inability to work due to a covered injury or illness. |

| Payout Type | One-time, lump-sum payment. | One-time, lump-sum payment to beneficiaries. | Ongoing, periodic payments (e.g., monthly) to replace lost income. |

| Main Purpose | Provide capital for costs of a catastrophic accidental injury or death. | Provide financial security for beneficiaries after the insured's death. | Replace a portion of the insured's income during a period of disablement. |

| Coverage Scope | Narrow and specific: Only covers listed accidental events. | Broad and comprehensive: Covers most causes of death. | Broad: Covers a wide range of injuries and illnesses that prevent work. |

| Example Scenario | A motor vehicle accident results in the loss of a leg, triggering a partial payout. | Death due to a heart attack triggers a full payout to the surviving spouse. | A serious back injury prevents a surgeon from working, triggering monthly payments. |

As you can see, these policies do not overlap; they are complementary. Relying on just one creates significant vulnerabilities. A well-designed financial plan utilizes all three to create a comprehensive shield against life’s most severe and unpredictable events.

Who Truly Requires AD&D Coverage?

While supplemental AD&D insurance can offer an additional layer of financial security for almost anyone, it is not a universal necessity. Instead, it should be viewed as a precision instrument for a select group whose lifestyles, professions, or financial situations expose them to a higher risk of accidental loss. It is for individuals who understand the value of hedging against low-probability, yet incredibly high-impact, events.

For high-net-worth individuals, frequent business travelers, and expatriates, this coverage is a particularly astute choice. It addresses a specific vulnerability that other policies, such as life or health insurance, may not fully mitigate.

Professionals and Lifestyles with a Higher Risk Profile

Certain professions and avocations naturally involve greater exposure to accidental risk. For people in these roles, supplemental AD&D is a surprisingly cost-effective way to protect their financial legacy against the unique dangers they face.

A few examples include:

- Executives with Global Travel Schedules: Constant flights, reliance on ground transport in unfamiliar countries, and demanding schedules all contribute to a statistically higher probability of being involved in an accident.

- Pilots and Aviation Professionals: The nature of their work presents a direct and obvious risk of a catastrophic accident where AD&D would be essential.

- Adventure Sports Enthusiasts: Individuals who participate in activities like skiing, mountaineering, or motorsports are willingly accepting a higher level of personal risk. Supplemental coverage is simply a prudent measure.

For these individuals, an AD&D policy is not just insurance; it is a calculated element of a personal risk management strategy.

Supplemental AD&D also serves as a powerful liquidity tool for an estate. In the event of an accidental death, it injects immediate cash to beneficiaries. This prevents the forced liquidation of assets like real estate or private equity, often at unfavorable prices, simply to cover immediate financial needs.

This instant capital is crucial, especially for primary breadwinners with significant financial responsibilities. It ensures their family and estate are not thrown into chaos by a sudden tragedy.

The Critical Gap for Expatriates

For expatriates, particularly financial professionals operating in global hubs like Singapore or London, supplemental AD&D fills a unique and vital role. Their primary health coverage is typically an International Private Medical Insurance (IPMI) plan, which is excellent for covering medical treatment costs.

The deficiency, however, is that IPMI does not address the immense financial fallout of a catastrophic accident. It will pay hospital bills but offers no compensation for the permanent loss of a limb or the economic devastation of an accidental death. This is precisely the gap that supplemental AD&D is engineered to fill.

The market for this type of voluntary coverage has grown steadily. Many larger firms recognize its value, with a significant majority of employers offering some form of AD&D. When employers contribute to the premium, employee participation often rises substantially, indicating a clear perceived value. You can find more insights on the rise of supplemental insurance benefits and how they fit into modern compensation packages.

For the globally mobile professional, it is a crucial financial backstop that standard medical plans simply cannot provide.

Navigating Key Policy Exclusions and Limitations

Any sophisticated investor knows that the true value of a financial product is found within its contractual details. Supplemental AD&D insurance is no different. Its power derives from its focused nature, and understanding its boundaries is key to using it effectively. This coverage is built for one thing: accidents. This means it will not pay out for losses caused by illness or disease.

The most fundamental exclusion is death from natural causes. If a death is the result of a heart attack, a stroke, cancer, or any other medical condition, it is not covered. This is the clearest demarcation between AD&D and a traditional life insurance policy. Grasping this distinction is the first step to integrating supplemental AD&D correctly into your overall financial plan.

Common Exclusions to Understand

Beyond illness, a handful of standard exclusions sharpen the policy's focus. The precise wording may differ between insurers, but most supplemental AD&D plans will not pay benefits for losses tied to specific situations. A clear-eyed view of these limitations prevents surprises when it matters most.

Here are the events you will almost always find excluded:

- Self-inflicted injury or suicide: Policies are designed for accidents, not intentional acts of self-harm.

- Committing a felony: If the injury or death occurs while the insured person is committing or attempting to commit a felony, the claim will be denied.

- Influence of non-prescribed substances: Accidents that occur while under the influence of illegal drugs or alcohol (often defined as being over the legal driving limit) are typically excluded.

- Acts of war: Death or injury resulting from declared or undeclared war is a standard exclusion.

It is critical to be aware of these stipulations. For a complete picture, it is always wise to review materials that explain how medical conditions can be affected by different policy exclusions.

The purpose of exclusions is not to weaken the policy. It is to define its function with precision. They keep premiums affordable by concentrating the policy on its core mission: delivering a major payout for a purely accidental, unforeseen catastrophe.

High-Risk Activities and Special Considerations

Many standard AD&D policies also exclude certain high-risk hobbies or professions. This may include activities like motor racing, scuba diving, or piloting a private aircraft (being a fare-paying passenger on a commercial flight is covered). These activities often fall outside a base policy's coverage.

However, participation in these activities does not preclude coverage. It simply means you will likely need to add a special rider to your policy or secure a specialized plan designed to underwrite these specific risks.

Complete transparency about your hobbies and profession during the application process is non-negotiable. It is the only way to ensure your policy will perform as expected when needed. This upfront honesty guarantees your supplemental AD&D insurance can serve its purpose as a reliable financial backstop for genuine accidents.

Integrating AD&D into Your Global Financial Strategy

For those managing substantial assets across different jurisdictions, supplemental AD&D is far more than just another policy. It is a strategic component of your financial fortress. The key is to cease viewing it as a standalone product and instead see it as a critical gear in your wider wealth preservation machine, working in perfect concert with all other elements.

This process begins with determining the appropriate coverage amount. A proper calculation extends well beyond simple income replacement. It must factor in your global assets, outstanding debts, family obligations, and long-term financial objectives. For high-net-worth expatriates, this also means accounting for potential estate taxes and the considerable costs of international repatriation.

A Holistic Approach to Risk Assessment

This is where specialized advisory services become invaluable, as they can properly assess a client’s entire risk profile. It involves a detailed analysis of how supplemental AD&D insurance interacts with your existing life insurance, investment portfolios, and especially your International Private Medical Insurance (IPMI). While an IPMI plan is non-negotiable for covering medical expenses, it does nothing to soften the devastating economic blow of a permanent disability from an accident.

A truly effective financial plan is one where every component has a defined purpose. Supplemental AD&D's role is to provide a massive, immediate injection of liquidity following a catastrophic accident, shielding your core assets from being liquidated under duress.

This ensures your family has immediate access to capital without being forced to disrupt carefully constructed investment strategies. You can explore the core international private medical insurance benefits uncovered to get a clearer picture of how these two policy types work in tandem to create comprehensive protection. At its core, a robust financial strategy must prioritize strength against shocks, much like applying stoic principles for financial resilience to protect your wealth.

Ultimately, by treating what is supplemental AD&D insurance as an integral part of your global financial framework, you transform it from a simple policy into a powerful tool. It becomes a mechanism for securing your legacy and protecting your family’s future, no matter where in the world your life or business takes you.

Frequently Asked Questions

When evaluating any insurance policy, the critical details require careful examination. Securing clear, direct answers to your questions is the only way to make an informed decision. Here are a few of the most common inquiries regarding supplemental AD&D insurance.

Can I Designate More Than One Beneficiary?

Yes, absolutely. You have complete control over who receives the benefit. You can name a single individual, divide it among several people, or direct the funds to a trust or your estate.

If you choose to name multiple beneficiaries, you will specify the percentage of the payout each is to receive. It is imperative to review your choices every few years—major life events such as a marriage, divorce, or the birth of a child should be an immediate trigger to update your designations and ensure the funds are distributed according to your current intentions.

Is the Claims Process Complex?

No, the claims process for AD&D is typically much more straightforward than for other types of insurance for one simple reason: the triggering event is a clear-cut accident. There is very little ambiguity.

Generally, the process involves submitting a claim form, a certified copy of the death certificate for a death claim, or detailed medical records from the treating physician that confirm the specifics of a dismemberment.

Because the payout criteria are objective and based on verifiable events, claims are often settled much more rapidly than with life or disability policies, which can require extensive investigations of medical history.

The primary objective is to get funds into the hands of your family quickly, providing critical liquidity at the moment it is needed most.

What Happens to My Coverage if I Change Jobs?

This is a critical question for any professional, particularly for those who move between countries and companies. Portability is key. If your AD&D coverage is part of an employer's group plan, you may lose it upon termination of employment.

However, many providers now offer a conversion privilege, allowing you to convert your group policy into an individual one when you leave. An even better strategy is to purchase a private, individual AD&D policy from the outset. This completely decouples your coverage from your employment, giving you continuous protection no matter where your career takes you. For a globally mobile professional, this is not a convenience—it is an essential element of a sound financial plan.

At Riviera Expat, we provide the clarity and expert guidance needed to integrate specialized insurance products into your global financial strategy. We help you find the right protection to secure your assets and legacy. Discover how we can assist you with your international insurance needs.