Understanding the nuances of insurance can be a complex endeavor. The most effective approach is to view the different types as the strategic pillars supporting your entire financial legacy. For high-net-worth individuals, insurance transcends its role as a mere expense; it becomes a foundational tool for preserving wealth, managing sophisticated risks, and ensuring the seamless transfer of assets to the next generation.

This framework is designed to help you protect what matters most—from your family’s well-being and security to your most significant professional accomplishments.

A Framework For Understanding Your Insurance Needs

At its core, insurance is a sophisticated mechanism for risk transfer. However, when managing substantial assets, this simple concept evolves into an essential component of a resilient financial strategy. A well-designed insurance portfolio functions like a bespoke security system, where each policy is precisely calibrated to guard a different facet of your life and legacy. This is not a reactive measure; it is a proactive strategy to ensure that an unforeseen event does not derail your long-term objectives.

The global insurance market is vast, but it can be distilled into three core areas of focus. According to global insurance market analysis, life insurance represents the largest segment by premium volume, followed by property and casualty (P&C), and then health insurance. These three pillars form the basis of a comprehensive protection strategy.

To provide a clearer perspective, here is a concise summary of how these primary categories interrelate.

Primary Insurance Categories At A Glance

This table delineates the main insurance types, their core functions, and their strategic importance for individuals managing significant wealth.

| Insurance Category | Core Function | Strategic Importance For HNWIs |

|---|---|---|

| Personal | Safeguards your health, life, and income-earning ability. | Protects human capital, ensures family continuity, and provides liquidity for estate planning. |

| Property & Casualty | Protects tangible assets like real estate, vehicles, and collections. | Shields physical wealth from loss and defends against high-stakes liability claims. |

| Business & Specialty | Covers professional liabilities, leadership risks, and unique exposures. | Secures business assets, protects personal wealth from professional lawsuits, and manages niche risks. |

Understanding these categories allows you to view your insurance portfolio not as a disparate collection of policies, but as a cohesive and integrated defense system.

The Three Pillars Of Coverage

To construct a portfolio that is truly effective, one must understand how these pillars function independently and, more critically, how they operate in synergy.

-

Personal Insurance: This is your foundation. It is entirely focused on protecting you—your health, your life, and your capacity to generate income. Key examples include life, premium health, and disability insurance.

-

Property & Casualty Insurance: This pillar is dedicated to protecting your assets. This encompasses everything from luxury residences and fine art collections to high-value automobiles and, most crucially, your personal liability.

-

Business & Specialty Insurance: For entrepreneurs, executives, and professionals, this addresses the risks inherent to your professional life—professional liabilities, director and officer (D&O) risks, and sophisticated modern threats such as cyber events.

Consider your insurance portfolio in the same way you would a diversified investment strategy. You would never allocate all your capital to a single stock. The same logic applies here. You cannot rely on a single policy to protect your entire net worth. Each type of insurance is engineered to address a specific vulnerability in your financial armor.

The real strategic value emerges from understanding how these categories interact. For instance, a robust personal excess liability policy (which falls under P&C) sits atop your home and auto policies, creating a formidable shield against litigation. For a more detailed examination of this integrated approach, our guide on comprehensive insurance cover offers further detail.

This mindset transforms insurance from a perfunctory exercise into a powerful engine for wealth preservation, paving the way for a truly secure financial future.

Securing Legacy And Wellbeing With Personal Insurance

Personal insurance forms the bedrock of a robust financial defense, shielding you and your family from life’s inevitable uncertainties. For successful professionals, these policies are far more than mere safety nets. They are precision instruments for preserving wealth, executing legacy plans, and ensuring the continuity of the life you have meticulously built.

This is not about basic protection. It is about leveraging insurance for strategic advantage at every stage of your life and career.

We will deconstruct the three pillars of personal insurance—life, health, and disability. Consider them a coordinated defense for your most valuable asset: your ability to create and sustain wealth.

Life Insurance As A Strategic Financial Tool

Most perceive life insurance as simply a payout for their loved ones. While true, this is a limited view. Within a sophisticated financial portfolio, it is a powerful tool for estate planning, tax-efficient wealth transfer, and even business succession.

Grasping the main types is the first step toward unlocking their full strategic value.

There are three primary structures to understand:

-

Term Life Insurance: This can be likened to leasing protection. It covers you for a specific period—typically 10, 20, or 30 years—and provides a death benefit if you pass away during that term. It is clean, simple, and cost-effective, ideal for covering temporary yet significant obligations such as a mortgage or funding children's education.

-

Whole Life Insurance: This is akin to owning your protection. It covers you for your entire life, features fixed premiums, and—most critically—builds cash value that grows at a guaranteed rate. This cash value can be borrowed against, providing a flexible source of liquidity.

-

Universal Life Insurance: This policy offers the greatest flexibility among permanent options. Like whole life, it provides lifetime coverage but allows you to adjust your premiums and death benefit as your circumstances change. The cash value growth is often tied to market interest rates, offering the potential for higher returns.

Life insurance is more than a final payout; it is a strategic asset. A properly structured policy can provide the liquidity required to settle estate taxes, ensuring your heirs inherit assets, not liabilities. It can also fund a buy-sell agreement, guaranteeing a smooth transition of business ownership without liquidating company assets.

Understanding the full scope of various life insurance policies is critical to ensuring your final wishes are financially secure. The optimal choice is contingent entirely upon your long-term goals, whether simple income replacement or complex estate equalization.

Premium Health Insurance For Global Lifestyles

For professionals and families who live and operate across international borders, a standard health insurance plan is inadequate. Premium health plans are engineered to eliminate friction, providing access to world-class medical care wherever you are. They are distinguished by their extensive global networks, allowing you to consult top specialists without navigating restrictive referral bureaucracies.

A key feature for high earners is the Health Savings Account (HSA). An HSA is a tax-advantaged savings vehicle that allows you to set aside pre-tax funds for qualified medical expenses. It offers a triple tax advantage: contributions are tax-deductible, the funds grow tax-free, and withdrawals for medical costs are also tax-free. According to IRS Publication 969, the maximum annual contribution for 2024 is $4,150 for self-only coverage and $8,300 for family coverage, with a $1,000 catch-up contribution for those age 55 or older.

When your life spans continents, precision in your coverage is non-negotiable. To explore this topic further, our guide on international private medical insurance is an excellent resource for expatriates and global citizens.

Disability Insurance: Protecting Your Earning Power

This may be the most overlooked—and most critical—component of a personal insurance portfolio. Your greatest financial asset is not your investment portfolio or real estate holdings; it is your ability to generate income. Disability insurance protects that asset by providing a consistent income stream if an illness or injury prevents you from working.

The statistics are compelling: the Social Security Administration estimates that just over one in four of today's 20-year-olds will become disabled before reaching retirement age. For a high-income professional, the financial consequences of such an event would be devastating without a contingency plan.

The gold standard in this category is a robust "own-occupation" policy. This type of policy defines disability as the inability to perform the material and substantial duties of your specific profession. This is a critical distinction. It means you are eligible for benefits even if you are able to work in a different, lower-paying field. For specialists such as surgeons, attorneys, or financial traders whose entire earning potential is linked to a unique skill set, this level of protection is absolutely vital.

Protecting Tangible Assets With Property And Casualty Insurance

While personal insurance secures your health and legacy, Property and Casualty (P&C) insurance is the fortress that guards your tangible wealth. This coverage protects the physical assets you have worked diligently to acquire—from your custom residence and valuable art collection to your high-performance automobiles.

For high-net-worth professionals, a standard, off-the-shelf policy is insufficient. Such policies are designed for the average consumer, and your assets are anything but. Specialized coverage is not a luxury; it is a necessity. It is about constructing a financial bulwark against loss from damage, theft, or litigation, ensuring your accumulated wealth remains under your control.

Let's dissect the key components of a formidable P&C strategy. We will begin with bespoke coverage for your home and collections, proceed to specialized auto insurance, and conclude with the ultimate shield against lawsuits: the personal excess liability policy.

Bespoke Coverage For High-Value Homes And Collections

Standard homeowners insurance is designed for a typical suburban dwelling. Consequently, it falls dangerously short when protecting a unique residence, a fine art collection, or other irreplaceable valuables. High-value property insurance is a fundamentally different product, engineered from the ground up to manage the complexity of your assets.

One of its most critical features is the agreed-value endorsement. Unlike a standard policy that pays out based on a depreciated value at the time of loss, an agreed-value policy allows you to establish and lock in the payout amount for a specific item on the day you sign the policy.

This approach is essential for unique assets where value is subjective or appreciates over time.

- Fine Art and Antiques: Insurers will almost invariably require professional appraisals to establish an agreed value. This ensures that a priceless painting is covered for its true market worth, not what a standard formula might dictate.

- Jewelry and Wine Collections: Specialized riders or entirely separate policies can provide worldwide coverage, protecting these items whether they are at home, in transit, or housed in a secure storage facility.

- On-Site Risk Surveys: Many high-value insurers do more than just sell policies; they dispatch experts to your property. These specialists conduct on-site surveys to identify risks—such as fire hazards or security vulnerabilities—and help you mitigate them before a loss occurs.

Consider this analogy: insuring a one-of-a-kind sculpture with a standard policy is like attempting to value it with a simple calculator. An agreed-value policy is akin to engaging a team of expert appraisers who understand its true worth and lock that value in from day one.

Specialized Auto Insurance For Unique Vehicles

Just as your home requires specialized attention, so do your vehicles. Whether you own exotic sports cars, a meticulously restored classic, or a fleet of corporate vehicles, standard auto insurance is simply not structured to provide adequate protection.

Agreed-value coverage is equally important here. Following a total loss, a standard policy might only pay the "book value" for a classic car, which could be a fraction of its actual market worth. A specialized policy ensures you receive the full, pre-determined value. It is also crucial to understand precisely what liability insurance covers in the event of an accident.

These policies are also designed with the owner's lifestyle in mind, offering features that standard plans lack:

- Generous Liability Limits: Coverage that extends far beyond typical state minimums to properly shield your significant net worth.

- Original Manufacturer Parts: A guarantee that repairs will be made with authentic parts, preserving your vehicle's integrity and value.

- Flexible Usage Terms: Policies can be tailored for show cars, limited-use classics, or high-performance vehicles that are not your daily driver.

The Ultimate Shield: Personal Excess Liability Insurance

This may be the single most important P&C policy for any high-net-worth individual. A personal excess liability policy, commonly known as an umbrella policy, provides a substantial, additional layer of liability protection on top of your existing home and auto insurance limits.

Imagine your home and auto policies as individual shields, each with its own limit. An umbrella policy acts as a vast canopy that stretches over both, activating only after the limits of the underlying policies have been completely exhausted.

For example, if you are found liable for $3 million in damages from an auto accident, but your auto policy has a limit of $500,000, your umbrella policy would cover the remaining $2.5 million. Without it, your personal assets—investments, real estate, and even future earnings—would be exposed.

Determining the appropriate limit is key. Most advisors recommend coverage at least equal to your total net worth, creating a formidable defense against catastrophic lawsuits that could otherwise prove financially ruinous.

Navigating Complex Risks With Business And Specialty Insurance

For entrepreneurs and executives, personal wealth and business interests are often inextricably linked. While you have policies to protect your home and family, the professional sphere of your life—the company you have built, the decisions you make, the digital ecosystem in which you operate—carries its own set of substantial risks.

This is the domain of business and specialty insurance. These are not generic, off-the-shelf policies; they are highly specific shields designed for the complex, modern threats that can move from the boardroom to your personal bank account. Consider them the critical firewall between a professional misstep and your personal net worth.

Safeguarding Your Expertise With Professional Liability Insurance

If you provide advice or expert services for a living, this coverage is indispensable. Professional liability insurance, often called Errors & Omissions (E&O) insurance, is essentially malpractice coverage for non-medical professionals. It is designed for consultants, financial advisors, attorneys, and any professional whose expertise is their product.

Imagine a client alleges that your advice led to a significant financial loss. Regardless of whether negligence occurred, a defense is required. E&O insurance intervenes to cover legal defense costs, settlements, or judgments. Even a meritless claim can be financially draining to contest, and this policy ensures that a client's lawsuit does not deplete your business or personal accounts.

Defending Leadership With Directors And Officers Insurance

Leading a company places every decision under intense scrutiny. Directors & Officers (D&O) insurance is designed to protect the personal assets of corporate leaders from lawsuits arising directly from those management decisions.

Potential litigants can include shareholders, employees, creditors, and regulatory bodies. The claims often involve allegations such as:

- Breach of Fiduciary Duty: Accusations that leaders failed to act in the company's best interests.

- Mismanagement of Funds: Claims of negligent financial oversight or impropriety.

- Regulatory Non-Compliance: Lawsuits arising from failures to adhere to industry regulations.

D&O insurance funds the legal defense. Without it, executives are personally liable, placing their homes, investments, and retirement savings at risk.

This is not exclusive to large public corporations. Leaders of private firms and non-profit organizations face similar exposures. D&O coverage provides leadership with the confidence to make the bold, strategic decisions necessary for growth, knowing a safety net is in place.

Protecting Digital Assets With Cyber Insurance

In today's digital landscape, a cyberattack is a matter of when, not if. Cyber insurance is the modern necessity designed to manage the financial fallout from digital threats—risks that your standard liability policies almost universally exclude. The coverage is broad, protecting you from both your own direct losses and claims brought by others.

A robust cyber policy typically covers these essentials:

- Data Breach Response: Funds for forensic investigation, customer notification, and credit monitoring services.

- Business Interruption: Reimbursement for lost income and extra expenses if an attack forces your business offline.

- Ransomware Response: Access to expert negotiators and funds to manage extortion demands.

- Regulatory Fines: Coverage for penalties levied under data protection laws such as GDPR or CCPA.

It is well-documented that supervisory bodies are flagging cyber risk as a significant challenge for the global insurance sector, influencing how all types of policies are underwritten. As attacks grow in frequency and sophistication, this coverage becomes non-negotiable. You can find more insights on the evolving risk landscape and its industry impact. It is the definitive line of defense against a threat that can devastate a business virtually overnight.

Constructing A Custom Insurance Portfolio

Acquiring several different insurance policies does not constitute a strategy. True financial resilience is achieved by weaving individual policies into a single, cohesive portfolio that protects the entirety of what you have built.

Think of it less as collecting separate safety nets and more as designing an integrated security system for your entire net worth. Each policy must work in concert with the others, creating overlapping fields of protection that leave no critical asset exposed.

When you approach insurance with this mindset, you transition from reactive protection to proactive risk architecture. It is about ensuring your defenses are as meticulously planned as your investments.

Conducting A Personal Risk Assessment

The first step is a thorough personal risk assessment. This is not a simple checklist; it is a deep dive into your unique liabilities, assets, and lifestyle to map precisely where you are most vulnerable.

A proper assessment compels you to look beyond the obvious and consider the nuanced threats that standard, off-the-shelf policies almost always miss.

Key areas to analyze include:

- Liability Exposure: Do you serve on a non-profit board? Do you host large events at your home? These activities dramatically increase your personal liability risk.

- Asset Concentration: Are your most valuable assets physical, like real estate and fine art, or are they primarily financial? Understanding this balance determines whether property or liability coverage should be your priority.

- Lifestyle Risks: Frequent international travel, owning a yacht, or employing domestic staff all introduce specific risks that require specialized endorsements or entirely distinct policies. For those living or working abroad, understanding your options for expat medical insurance is a critical piece of this assessment.

- Business Interconnectivity: For entrepreneurs and executives, where does your business liability end and your personal liability begin? Pinpointing this intersection is absolutely crucial.

Understanding Policy Interplay

Individual policies are powerful, but their true strength is unlocked only when they work together. A classic example is the relationship between your home, auto, and personal umbrella policies.

Your home and auto plans provide the frontline liability defense, but their coverage limits can be exhausted in seconds by a major lawsuit. This is where an umbrella policy acts as high-level reinforcement, kicking in to extend your liability protection by millions of dollars after the primary policies are exhausted.

This strategic layering is the very essence of a well-constructed portfolio. It ensures a single catastrophic event does not cascade through your entire financial structure.

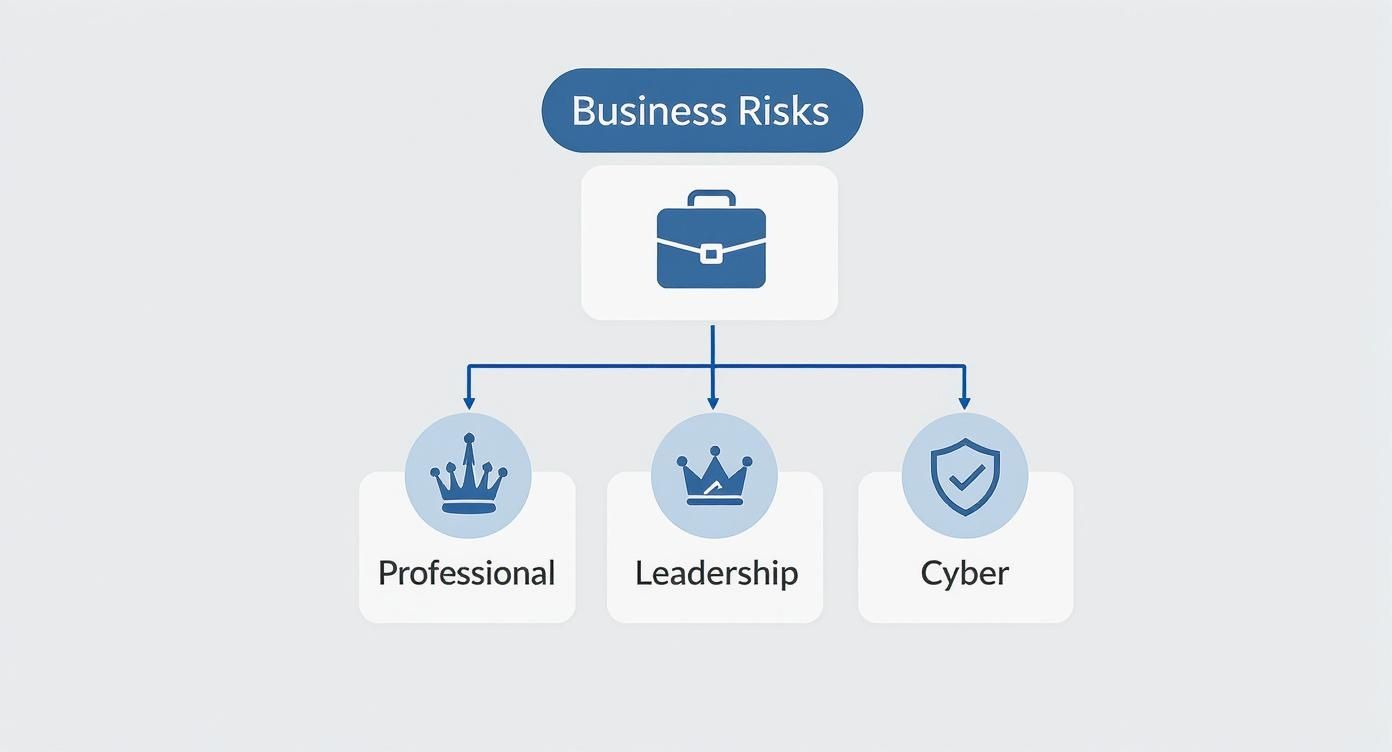

The following infographic shows just how layered business and specialty risks can be, illustrating why you need different types of coverage to protect against professional, leadership, and digital threats.

As you can see, comprehensive business protection requires distinct policies for professional negligence (E&O), leadership decisions (D&O), and cyber vulnerabilities, because each one addresses a completely unique risk category.

Evolving Your Coverage Over Time

An insurance portfolio is not a static document. It is a living strategy that must adapt as your life evolves. Any significant life event—a major asset acquisition, the sale of a business, a change in marital status, or children reaching adulthood—should automatically trigger a full portfolio review.

Your insurance needs are a direct reflection of your current life and net worth. A portfolio designed for a rising professional is fundamentally different from one built to protect a multi-generational estate. Periodic reviews are non-negotiable for maintaining relevant and robust protection.

Working with a specialized broker who truly understands the needs of high-net-worth individuals is essential. They can facilitate these reviews and provide access to bespoke products that are simply not available on the mass market.

To illustrate how dramatically needs can change, consider this comparison.

Sample Insurance Portfolio By Client Profile

This table demonstrates how insurance needs evolve, comparing the typical portfolio of an early-career professional against that of an established high-net-worth individual.

| Insurance Need | Early-Career Professional Portfolio | High-Net-Worth Individual Portfolio |

|---|---|---|

| Life Insurance | Term life to cover mortgage and income replacement. | High-value permanent life policies for estate tax liquidity and wealth transfer. |

| Liability | Standard auto and home liability limits. | $10M+ personal excess liability (umbrella) policy; specialized vehicle and property coverage. |

| Health | Employer-sponsored group health plan. | Global private medical insurance with access to top specialists worldwide. |

| Specialty | Basic disability insurance. | High-limit "own-occupation" disability, D&O liability, and cyber insurance. |

This comparison makes it clear: as your assets grow, your insurance strategy must shift from basic protection to sophisticated wealth preservation.

Frequently Asked Questions

When managing significant assets, the world of insurance presents very specific questions. Let's address some of the most common inquiries from successful professionals to bring clarity to the construction of a truly protective portfolio.

How Much Umbrella Insurance Do I Need?

Determining the appropriate amount of umbrella coverage is a strategic calculation, not a guess. The absolute baseline is to secure coverage that at least matches your total net worth.

However, that is merely the starting point. You must also consider future earning potential and unique lifestyle risks. Do you host large gatherings? Sit on a non-profit board? Maintain a high public profile? Any of these factors can dramatically increase your liability exposure, suggesting a limit that extends far beyond your current net worth may be necessary to truly shield yourself from a catastrophic lawsuit.

Is Life Insurance A Good Investment?

This is an excellent question. Certain types of permanent life insurance, such as whole and universal life, can be much more than just a death benefit. They accumulate a tax-deferred cash value over time.

Consider it a conservative growth vehicle with an additional benefit. You can borrow against this cash value or use it to supplement retirement income, providing valuable liquidity. For estate planning, it is a powerful tool—the policy’s death benefit provides tax-free funds to cover estate taxes, ensuring your assets pass to your heirs intact.

Are Collectibles Covered Under Homeowners Insurance?

This is a dangerous assumption. No, they are not adequately covered. A standard homeowners policy provides exceptionally low coverage for high-value items like fine art, wine collections, or jewelry.

These policies often have strict sub-limits—for instance, $2,500 for an entire jewelry collection—and typically will not cover specific risks like accidental breakage or mysterious disappearance.

To properly protect these prized possessions, a specialized plan is required. This means either adding a scheduled personal property rider to your existing policy or, preferably, obtaining a separate, standalone collections insurance policy for an agreed-upon value.

When Should I Review My Insurance Portfolio?

Your insurance portfolio is not a "set it and forget it" component of your financial life. It requires a review annually, at a minimum, or whenever you experience a major life milestone.

What events trigger a review? A few key examples:

- A significant change in your net worth.

- The purchase or sale of a major asset, such as a home, boat, or business.

- Changes in your family structure, like marriage or the birth of children.

- Assuming a new role that increases your liability, such as joining a corporate board.

Regular check-ins ensure your coverage remains perfectly aligned with your current life circumstances.

At Riviera Expat, we specialize in providing expert guidance on international private medical insurance for high-net-worth professionals. Let us help you secure the clarity and confidence you deserve in your healthcare decisions. Explore your options with us at https://riviera-expat.com.