An insurance deductible is the predetermined amount you are responsible for paying toward a covered loss before your insurance policy begins to contribute. For high-net-worth individuals, this is not a peripheral detail but a strategic instrument for managing financial risk and optimising the cost of your insurance premiums.

What an Insurance Deductible Represents in Your Financial Strategy

Fundamentally, a deductible represents the portion of risk you agree to retain. When you secure an insurance policy, you are transferring the potential for a substantial, unpredictable financial loss to an insurer. The deductible is the predictable, manageable component of that risk that you hold in-house.

This structure serves two primary functions. Firstly, it discourages the filing of minor, high-frequency claims. If insurers were required to process every trivial claim, their administrative overhead would escalate, which would, in turn, increase premiums for all policyholders. Secondly, it provides you with direct control over your insurance expenditures, allowing you to align your policy with your personal risk tolerance.

The Core Financial Trade-Off

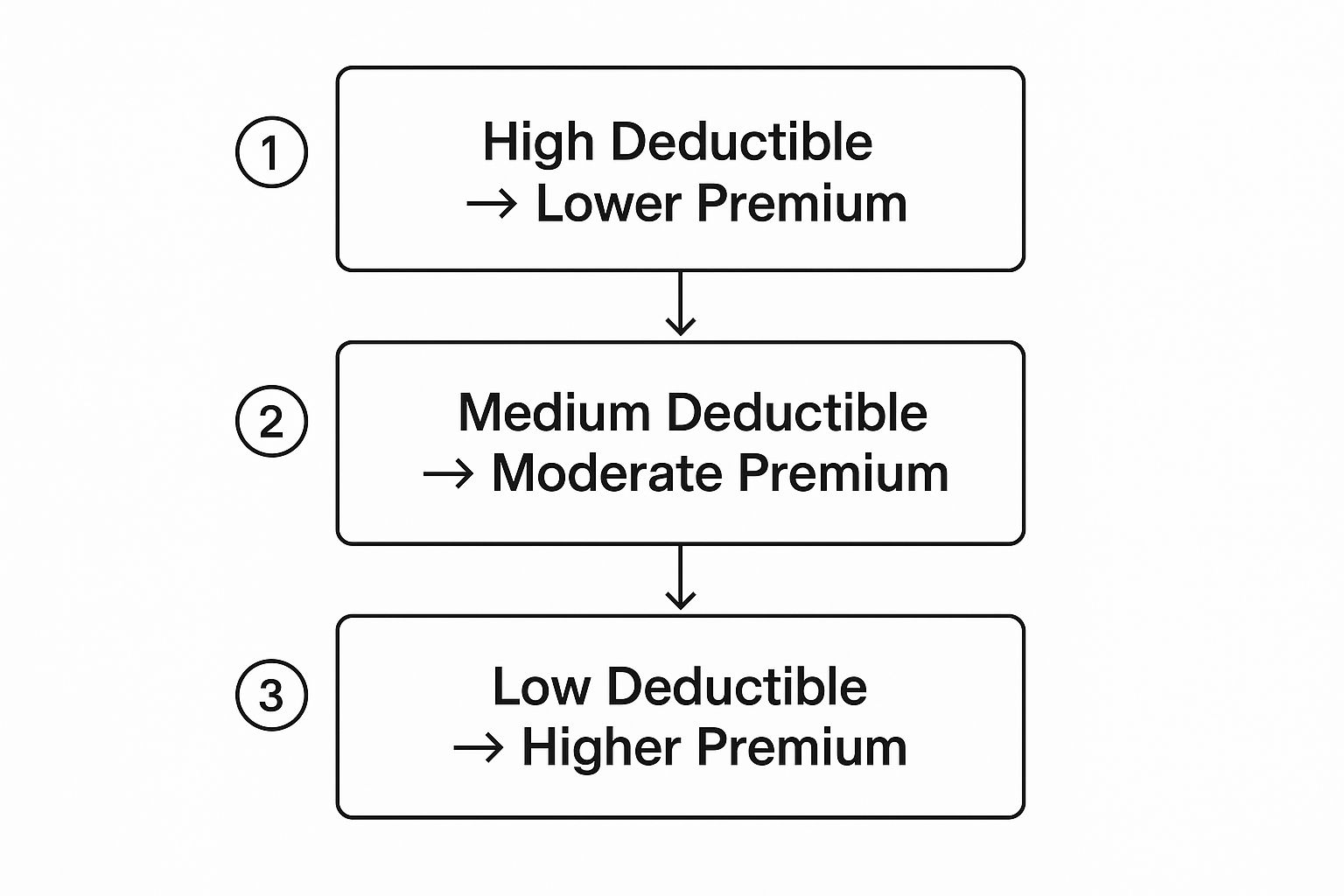

The relationship between your deductible and your premium is an inverse correlation.

When you select a higher deductible, you signal to the insurance company your willingness to absorb a larger initial cost in the event of a claim. This reduces their potential payout, and they reciprocate with a lower premium.

This dynamic transforms the deductible from a mere policy term into a powerful lever for managing your finances. It enables you to precisely calibrate your coverage to match your strategic objectives.

Here is a concise summary of how this trade-off functions in practice.

The Deductible and Premium Relationship at a Glance

| Your Chosen Deductible | Your Insurance Premium | Your Initial Outlay for a Claim |

|---|---|---|

| Higher | Lower | Higher |

| Lower | Higher | Lower |

This table illustrates the fundamental choice you make when selecting a deductible. The decision is a balance between your recurring premium payments and your potential out-of-pocket exposure during a claim.

By strategically adjusting your deductible, you can directly influence your cash flow, freeing up capital that could be directed toward other investments while maintaining robust protection against significant financial disruption.

Achieving the correct balance is paramount. The fine print in insurance policies can be complex, particularly regarding terms like "excesses" and "deductibles," which have specific definitions that can affect your financial obligation. You can explore these nuances in our article on spotlight on the fine print excesses and deductibles. For a more foundational perspective, consult a simple guide to understanding what a deductible is.

How a Deductible Functions in a Real-World Claim Scenario

Abstract definitions are useful, but the true test of a deductible's function occurs during a claim. The real measure of its impact comes when a significant event occurs—for instance, major storm damage to a primary residence.

Let us posit that a severe storm inflicts $75,000 in damage to your property. Your homeowners insurance policy includes a $10,000 deductible. At this juncture, the claims process is initiated with a clear financial sequence.

Your Responsibility and the Insurer’s Obligation

Your deductible is your contractually agreed-upon contribution. It is the initial amount you cover before your insurance company intervenes to assume the much larger, potentially financially debilitating cost.

- Damage Assessment: A claims adjuster evaluates the damage and officially confirms the total repair cost is $75,000.

- Your Contribution: Your responsibility is to cover the first $10,000 of that cost. This is your deductible.

- Insurer's Payment: Once your deductible has been met, your insurance policy activates. The insurer then pays the remaining $65,000 to complete the property repairs.

This system ensures you cover a predictable portion of the loss, while the insurer absorbs the substantial financial impact, protecting your assets from severe depletion. It is a financial partnership.

This infographic captures the essential relationship between your deductible and the cost of the policy itself.

The principle is straightforward. When you agree to assume more of the initial risk out-of-pocket (a higher deductible), your ongoing policy costs (your premium) will be lower.

For health insurance claims, the principle is identical, but the process often involves additional steps, such as network pre-authorisations. It is imperative to understand the specific procedures for your plan, as this knowledge is critical for a seamless experience, particularly during major medical events. You can review a full breakdown of pre-authorisation and direct settlement in our guide.

Understanding the Different Types of Deductibles

It is common to view a deductible as a single, static figure, but this is an oversimplification. Not all deductibles are structured identically. For any individual managing a portfolio of significant assets, understanding the distinctions between them is fundamental to sound risk management.

The structure of what are insurance deductibles can vary significantly depending on the type of policy and the asset it is designed to protect. Correctly interpreting this distinction is key to aligning your coverage with your financial strategy.

Most are familiar with the fixed deductible, also known as an absolute deductible. This is a specific, predetermined dollar amount you pay before your insurer's contribution begins—for example, $1,000 on an auto policy or $5,000 on a health insurance plan. Its simplicity provides predictability for most common claims.

Specialized Deductible Structures

However, when insuring high-value assets, the structures become more sophisticated. Consider the percentage-based deductible. This is not calculated based on the amount of the loss but as a percentage of your property's total insured value.

For example, if you own a $3 million coastal residence with a 2% hurricane deductible, you are responsible for the first $60,000 of damage from a named storm. This structure is prevalent for properties exposed to specific, high-severity perils like hurricanes or earthquakes, where potential losses are substantial.

A critical distinction, particularly in health and liability insurance, is whether your deductible is applied on a per-incident or calendar-year basis. A per-incident deductible resets for each separate claim, whereas a calendar-year deductible aggregates all your covered expenses toward a single total for the year until the threshold is met.

These structures are not arbitrary; they adapt to risk environments globally. For instance, recent analysis from Aon's global insurance market overview indicates a trend of rising deductibles in Asia and Latin America as insurers respond to escalating climate-related events. Conversely, deductibles have remained relatively stable in North America and Europe.

Understanding these different types allows you to look beyond the premium and critically assess the true nature of a policy's coverage. It is the only way to ensure you achieve the optimal balance between your recurring costs and your capacity for out-of-pocket expenditure.

The Strategic Interplay Between Deductibles and Premiums

Managing your insurance coverage involves a continuous balancing act. It is a direct trade-off between your regular payments—your premium—and your potential out-of-pocket liability in the event of a claim—your deductible. This is not merely a policy detail; it is the primary financial lever you can adjust to structure your coverage.

If you opt for a higher deductible, you are communicating to the insurer your willingness to retain a larger portion of the initial risk. Insurers favour this arrangement and, in return, provide a significantly lower premium. For many, this is a sophisticated financial decision that frees up capital for other purposes, such as investments or liquidity management.

Conversely, choosing a lower deductible is a strategy for securing financial certainty. While your premiums will be higher, you gain the assurance that a major claim will not necessitate a sudden, large-scale liquidation of assets. It is a method of protecting immediate cash flow from unexpected financial shocks.

Calculating Your Financial Break-Even Point

So, which approach is optimal for your situation? The decision hinges on your personal financial structure and your tolerance for risk.

Let's perform a simple calculation. Assume that by increasing your deductible from $5,000 to $10,000, you achieve an annual premium savings of $1,000. In this scenario, your break-even point is five years. If you remain claim-free for five years, the premium savings have fully offset the additional risk you assumed.

This straightforward calculation empowers you as the policyholder. It transforms a standard policy choice into a strategic financial decision, allowing you to balance short-term capital efficiency with long-term security.

This dynamic is not exclusive to policyholders; it is integral to the insurance industry itself. Globally, non-life insurance premiums experienced real-term growth of approximately 3.9% in 2023. A contributing factor is the industry trend of insurers increasing deductibles to manage their own risk exposure, a practice detailed in Deloitte's 2024 insurance outlook.

To gain a more comprehensive understanding of the factors influencing your premiums, our guide on why medical insurance premiums rise year after year provides valuable insights.

How to Select the Optimal Deductible for Your Financial Position

Choosing the correct deductible is not an arbitrary decision—it is a strategic choice that must align precisely with your financial architecture. There is no universally correct answer. The process requires an honest assessment of your liquid assets, the robustness of your emergency fund, and your capacity to absorb financial risk without compromising your long-term objectives.

If you maintain substantial liquid reserves and a well-funded emergency account, a higher deductible can be a prudent financial strategy. The resulting premium savings can be significant, freeing up capital for reallocation. However, this approach is only viable if you can comfortably cover the higher out-of-pocket expense without disrupting your financial stability should a claim arise.

Aligning Deductibles with Your Asset Portfolio

For individuals managing a diverse portfolio of assets, the decision becomes more nuanced. The nature of the asset being insured should be a primary factor in your deductible selection.

Consider these distinct scenarios:

- Primary Residence: For your main home, a moderate deductible typically offers the most sensible approach. It establishes a favourable balance between premium savings and manageable repair costs for common claims, such as plumbing failures or storm damage.

- Vacation Property: For a secondary residence that may be unoccupied for extended periods, a higher deductible is often a logical choice. It reduces your ongoing holding costs while preserving protection against catastrophic events, such as a fire.

- Luxury Vehicles or Collections: For high-value personal property—such as exotic automobiles, fine art, or jewellery—a lower deductible can provide essential peace of mind. These assets often face unique risks, and you will want the ability to facilitate immediate repair or replacement without a substantial upfront capital outlay.

The optimal deductible is one that protects you from a catastrophic financial event without creating a liquidity crisis or compelling you to overpay in premiums. It is a calculated decision based on your ability to self-insure the initial portion of a potential loss.

Ultimately, the goal is to select a deductible you could pay tomorrow without hesitation or financial strain. This requires a clear-eyed analysis of what an insurance deductible means within the context of your personal balance sheet. By methodically evaluating your financial position and the specific assets you are protecting, you can transform your insurance coverage from a simple expense into an efficient component of your overall wealth management strategy.

How Health Insurance Deductibles Integrate into the Broader Financial Picture

Health insurance operates with more complexity than property or auto insurance. When you incur a medical expense, your deductible is merely the first component of your financial responsibility. It functions as part of a cost-sharing framework that also includes copayments and coinsurance, and a comprehensive understanding of their interplay is essential.

Consider the process sequentially. First, you must satisfy your deductible. This is the amount you pay out-of-pocket for most covered medical services before your insurance plan begins to pay its portion. Once this threshold is met, your financial responsibility lessens, but does not cease.

After your deductible is met, you enter the coinsurance phase. Here, you pay a specified percentage of the cost (e.g., 20%), while your insurer pays the remainder (e.g., 80%). Every payment you make—your deductible, copayments for physician visits, and your coinsurance share—contributes toward your out-of-pocket maximum. This figure acts as your annual financial safeguard; it is the absolute most you will pay for covered, in-network medical services in a policy year. Once you reach it, your insurer covers 100% of subsequent eligible costs.

High-Deductible Health Plans: A Strategic Consideration

Certain individuals strategically select plans with higher deductibles. Known as High-Deductible Health Plans (HDHPs), these can be a powerful financial tool when paired with a Health Savings Account (HSA). The arrangement is simple: you accept a higher deductible in exchange for a lower monthly premium.

This strategy is optimised when you direct the premium savings into a tax-advantaged HSA. Contributions to an HSA are tax-deductible, the funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free. An HSA is not merely a healthcare payment account; it is a long-term investment vehicle with a unique triple tax advantage.

An HDHP and HSA combination can transform your health insurance from a purely defensive expenditure into an active component of your wealth-building strategy, unlocking tax efficiencies unavailable with other plan types.

However, one must be prepared for the "high-deductible" reality. A 2025 analysis found that some silver-tier marketplace plans can carry deductibles from $5,000 to $6,000, with certain bronze plans approaching $7,500. This represents a substantial increase from the average $1,800 deductible for employer-sponsored plans. You can discover more about these high deductible trends on commonwealthfund.org. The critical takeaway is that this strategy is only suitable for those with sufficient liquidity to cover the significant initial deductible should a serious medical need arise.

Answering Your Top Questions About Deductibles

Let us clarify some of the most frequent questions regarding deductibles. A clear understanding of these scenarios is crucial for leveraging your insurance policy effectively and avoiding unwelcome surprises.

Is My Deductible Payable if I Am Not At Fault?

This is a common point of confusion. The answer is typically: Yes, you are still required to pay your deductible to initiate your claim, even when another party is clearly liable. Your insurance company advances the remaining cost to expedite your recovery and minimise disruption.

However, this does not mean the cost is permanently yours. Your insurer will then pursue the at-fault party's insurance company to recover its total outlay through a process called subrogation. Upon successful recovery, they will also reclaim your deductible and refund it to you in full. This process, however, can take time.

Should I File a Claim for Minor Damage?

A prudent rule of thumb is that if the cost of repair is close to or less than your deductible amount, it is often more financially sound to pay for it directly. Filing a claim in such a situation will yield a minimal or zero payout from the insurer.

Furthermore, filing a claim, however small, is recorded in your insurance history. A pattern of frequent claims can classify you as a higher risk, which may lead to a premium increase upon renewal. In the long run, the small payout is unlikely to be worth the potential increase in future costs.

Once your deductible, copayments, and coinsurance payments have accumulated to meet your annual out-of-pocket maximum, your health plan is obligated to cover 100% of all eligible, in-network medical services for the remainder of the plan year.

How Do Deductibles and Out-of-Pocket Maximums Interact?

In health insurance, your deductible is the first financial threshold you must cross. After you have paid this amount for medical services, your plan's other cost-sharing mechanisms, such as coinsurance, become active.

From that point forward, every dollar you spend on your deductible, copayments, and coinsurance is aggregated toward your out-of-pocket maximum. This figure represents your total financial exposure for the year. Once you reach this limit, your plan assumes 100% of the cost for all covered, in-network care, thereby protecting you from the financial consequences of catastrophic medical expenses.

Navigating the complexities of international health insurance requires expert guidance. At Riviera Expat, we provide the clarity and control you need to make confident healthcare decisions. Explore our tailored IPMI consultation services at https://riviera-expat.com.