For discerning professionals, securing travel medical insurance for Vietnam is not merely an administrative task—it is a critical component of a sophisticated international strategy. While Vietnam does not mandate insurance for entry, a premium policy is the only mechanism to insulate against the significant financial and logistical challenges of navigating Vietnam's healthcare system as a foreign national.

Consider it this way: appropriate insurance provides immediate access to international-standard medical care, eliminating the need to personally front prohibitive cash payments.

Why Premier Medical Insurance Is Non-Negotiable in Vietnam

Whether your agenda in Vietnam involves a high-stakes business negotiation or a well-deserved respite, a strategic approach to risk management is paramount. The country is remarkable, but its medical infrastructure is profoundly different from what you likely experience at home. Your domestic health plan will almost certainly not be accepted for direct payment at the high-caliber private hospitals you would require in an emergency.

This creates a critical vulnerability that only a specialized travel medical insurance policy can effectively address. Without it, you are personally liable for immediate, and often substantial, out-of-pocket payments before a physician even begins treatment.

Protecting Your Health and Your Assets

The primary function of an executive-level travel medical insurance policy is to dismantle that financial barrier. It serves as your financial guarantee, authorizing premier international hospitals in Ho Chi Minh City or Hanoi to deliver immediate, world-class care. It operates less like a conventional insurance policy and more like a pre-arranged, high-limit line of credit for your health.

A robust insurance plan is the bedrock of a secure international itinerary. It transforms a potential medical crisis from a personal financial disaster into a manageable, professionally handled event, protecting both your health and your capital.

Beyond settling hospital bills, a superior policy functions as a logistical command center. It provides a direct line to a 24/7 global assistance network, staffed by multilingual experts who assume control of every aspect of your care.

They will:

- Liaise directly with physicians to ensure you receive the appropriate course of treatment.

- Arrange direct payment guarantees with hospitals, so you are not burdened with billing.

- Organize a medical evacuation to a regional center of excellence, such as Singapore or Bangkok, should local facilities be inadequate for your needs.

Ultimately, investing in the right travel medical insurance for Vietnam is an indispensable precaution. It ensures a medical issue remains a temporary setback, not a catastrophic event, allowing you to focus entirely on your recovery, confident that every detail is being expertly managed.

Choosing Your Coverage: Short-Term Plans vs. Global Medical Insurance

Selecting the appropriate insurance for a trip to Vietnam is a strategic decision contingent upon your international lifestyle and professional commitments. Your choice effectively lies between two distinct categories of protection, each engineered for a specific profile of traveler.

Short-term travel medical insurance is analogous to a high-performance rental vehicle: ideal for a single, defined journey, providing exceptional protection against sudden emergencies like an accident or illness.

In contrast, International Private Medical Insurance (IPMI) is akin to owning a premium, globally capable vehicle. It is the definitive solution for those on extended assignments, managing frequent international travel, or for executives who demand seamless, top-tier healthcare access not just in Vietnam, but anywhere their interests take them. This coverage extends far beyond emergencies, often encompassing routine diagnostics and preventative care to maintain your health regardless of your location.

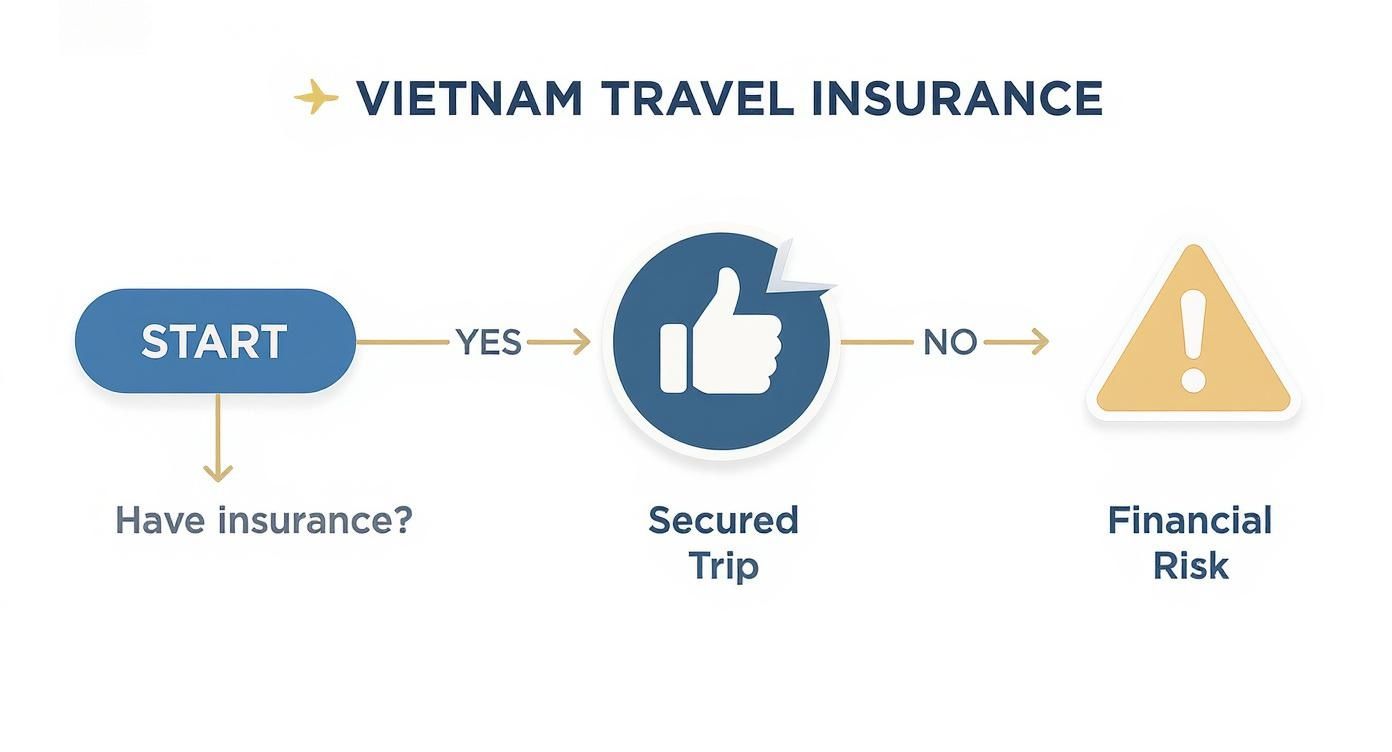

This visual decision tree clarifies how the right coverage secures your trip, while an inappropriate choice—or no choice—exposes you to significant financial risk.

The conclusion is simple yet powerful: securing the correct insurance in advance is the only way to shield your assets from the staggering costs a medical event abroad can generate.

To illustrate the differences clearly, here is a side-by-side comparison.

Short-Term Travel Insurance vs. International Private Medical Insurance (IPMI)

A direct comparison of key features to help you decide which policy type aligns with your travel needs for Vietnam.

| Feature | Short-Term Travel Medical Insurance | International Private Medical Insurance (IPMI) |

|---|---|---|

| Best For | Single trips (vacations, business travel) with set dates, typically under 6 months. | Long-term residents, expatriates, and frequent global travelers. |

| Coverage Scope | Primarily emergency medical events, accidents, and trip disruptions. | Comprehensive healthcare, including emergencies, routine check-ups, specialist consultations, and wellness. |

| Geographic Area | Specific to the trip destination(s) for a defined period. | Global or regional coverage that is continuous and portable across borders, often including the home country. |

| Pre-Existing Conditions | Almost always excluded or subject to significant restrictions. | Often coverable through medical underwriting, sometimes with an adjusted premium. |

| Renewability | Terminates with the trip; a new policy is required for each journey. | Annually renewable, providing continuous protection without new medical underwriting. |

| Cost | Lower, as it covers a limited duration and scope. | Higher, reflecting its comprehensive, continuous, and portable nature. |

Ultimately, the optimal choice depends entirely on your lifestyle. A short-term plan is a focused, tactical instrument, whereas IPMI is a long-term strategic asset for managing your global health.

Short-Term Travel Insurance: For The Focused Itinerary

A short-term plan is precision-engineered for a journey with a clear beginning and end, such as a two-week business engagement or a month-long project in Ho Chi Minh City. Its primary function is to act as a powerful shield against sudden, unforeseen medical crises.

These policies excel at covering high-cost, low-probability events. Key features typically include:

- Emergency Medical Treatment: Covers expenses from accidents or sudden illnesses that arise during your trip.

- Trip Interruption & Cancellation: Reimburses you for non-refundable costs if your trip is curtailed or cancelled for a covered reason.

- Medical Evacuation: Manages the substantial cost and logistical complexity of transferring you to a better-equipped hospital if local care is insufficient.

However, because they are laser-focused on emergencies, they are not designed for routine care or managing chronic health conditions. Pre-existing conditions are almost universally excluded or subject to strict limitations, making these plans unsuitable for anyone with ongoing health requirements.

IPMI: The Global Standard for Executive Health

For the global professional whose work and life span multiple jurisdictions, International Private Medical Insurance offers a far more robust and flexible solution. An IPMI policy is not tied to a single trip; it provides continuous, comprehensive medical coverage globally, often including in your home country.

An IPMI plan is an asset for managing your global lifestyle. It ensures continuity of care, from annual physicals in Singapore to specialist consultations in London, providing a consistent standard of elite medical access wherever you are.

This level of coverage is essential for:

- Expatriates and Long-Term Residents: For any stay exceeding six months, IPMI is the only viable choice for complete health management.

- Frequent International Travelers: It eliminates the inefficiency of purchasing a new policy for every trip, providing seamless, year-round protection.

- Individuals with Pre-Existing Conditions: These plans are medically underwritten and can be structured to include coverage for chronic conditions, offering a level of assurance that a standard travel policy cannot provide.

- Executives Demanding Premier Access: IPMI plans grant access to extensive direct-billing networks, allowing for cashless treatment at top-tier international hospitals in Vietnam and around the world.

The depth and portability of IPMI are simply unmatched. For anyone embracing a more permanent international life or a sophisticated remote work arrangement, securing the right insurance is as fundamental as curating the ultimate digital nomad packing list.

Making the correct choice between these two coverage models ensures your health and finances are protected with a level of precision that mirrors your professional life. You can delve deeper into the world of international private medical insurance in our detailed guide.

Core Components of an Executive-Level Insurance Policy

When operating at a high level in Vietnam, a standard, off-the-shelf travel insurance plan is dangerously insufficient. A premium policy is constructed from several non-negotiable components, each designed to manage specific, high-stakes risks with logistical and financial precision. The objective is to ensure any disruption is managed seamlessly, allowing you to maintain focus.

The absolute cornerstone is the emergency medical benefit. While some plans may present lower limits, a prudent minimum for Vietnam is USD 500,000. This figure is not arbitrary; it is a realistic assessment of the potential costs of intensive care, major surgery, and a prolonged stay at a top-tier international hospital in Ho Chi Minh City or Hanoi. Anything less exposes you to a significant financial liability should a serious accident or sudden illness occur.

The Critical Importance of Medical Evacuation and Repatriation

The single most vital component of your travel medical insurance for Vietnam is medical evacuation and repatriation. This is your lifeline if local medical facilities—even the best available—cannot provide the highly specialized care your condition demands.

Imagine requiring urgent neurosurgery or advanced cardiac intervention. The logistical operation to move you from a hospital in Da Nang to a world-class facility in Singapore or Bangkok is extraordinarily complex. It necessitates a dedicated air ambulance, a specialized medical team, international clearances, and ground support at both ends.

The cost is astronomical, easily exceeding USD 100,000. Without this specific coverage, you would be left to coordinate and fund this entire operation personally, during a moment of extreme crisis.

A policy without a high-limit medical evacuation benefit is fundamentally incomplete. This coverage is the mechanism that guarantees your access to the best possible medical outcome, regardless of your location within Vietnam.

For this reason, you must scrutinize the evacuation limit. Your policy requires a minimum of USD 500,000 for evacuation and repatriation. This ensures that cost will never be a barrier between you and the highest standard of care in the region or back in your home country.

Essential Riders and Additional Benefits

A truly executive-level policy anticipates disruptions beyond purely medical events. These add-ons provide a comprehensive safety net that protects your entire travel investment and offers flexibility when circumstances change.

- Trip Interruption and Cancellation: This reimburses your non-refundable costs if a covered emergency forces you to cancel your trip beforehand or curtail it. For high-value itineraries with prepaid luxury accommodations and business class flights, this protection is indispensable.

- 'Cancel for Any Reason' (CFAR) Option: For ultimate control, a CFAR rider allows you to cancel your trip for any reason not covered by the base policy and still recover a significant portion (typically 75%) of your prepaid costs. It is an invaluable tool when business priorities shift unexpectedly.

- Specialized Activities Coverage: Your plans may involve more than boardrooms. Ensure your policy explicitly covers activities like golf, yachting, scuba diving, or trekking in Sapa, as these are often excluded from basic plans.

Securing this level of protection is more straightforward than it once was. Industry analysis indicates that quality plans for Vietnam typically include at least USD 100,000 in emergency medical cover and USD 500,000 for medical evacuation. While the Vietnamese government does not mandate insurance for entry, the universal practice of demanding upfront payment at quality hospitals makes robust coverage a practical necessity. You can explore these benchmarks further by reviewing these travel insurance insights for Vietnam.

By ensuring these core components are adequately funded within your policy, you build a powerful shield against the tangible risks of international travel. This allows you to focus on your objectives, confident that a professional support system is prepared to manage any crisis that may arise.

Navigating Vietnam's Healthcare System as a Foreign National

The primary characteristic of healthcare in Vietnam is its dual-system structure. Understanding this distinction is not merely academic—it is fundamental to accessing prompt, high-quality care. Your travel medical insurance for Vietnam is the key that unlocks the system you will want and need to use.

The public hospital system, which serves the local population, is not equipped for international visitors. You would likely encounter overcrowding, significant language barriers, and a standard of care that does not align with Western expectations. For these reasons, foreign nationals almost exclusively utilize the second tier.

This second tier consists of private, international-standard hospitals and clinics, concentrated in major hubs like Ho Chi Minh City, Hanoi, and Da Nang. These facilities are comparable to Western hospitals, featuring modern equipment, immaculate facilities, and English-speaking physicians. However, there is a critical protocol.

The Pay-First Mandate

There is one critical, non-negotiable rule at these top-tier facilities: they operate on a pay-first basis. To be clear—treatment will not commence, even in an emergency, until they have a guarantee of payment.

This means you will either be required to use a personal credit card for the full estimated cost or provide a Letter of Guarantee (LOG) from your insurance company. Your domestic health plan will not be recognized for direct billing. Without a proper international policy, you are personally responsible for what could be tens of thousands of dollars before a doctor even sees you.

Think of your travel medical insurance as your financial first responder. A reputable insurer can issue a LOG to the hospital within minutes, removing the payment barrier so the medical team can immediately focus on your treatment.

This direct-billing capability is, without question, the most vital feature of an insurance plan for Vietnam. It transforms a potential nightmare of upfront payments and stress into a simple, cashless process. You present your insurance card, and your provider liaises directly with the hospital's administration.

How to Access Emergency Services the Right Way

If you are facing a medical emergency, your first action should be to proceed to the nearest reputable international hospital. Do not delay by attempting to contact your insurer en route.

Once you are at the facility and in a stable condition, you or an associate must call the 24/7 emergency assistance number on your insurance card. This single phone call activates a critical support process.

A team of assistance experts will immediately:

- Speak with the medical staff to understand your diagnosis and the proposed treatment plan.

- Arrange for direct payment with the hospital, issuing the vital Letter of Guarantee.

- Assess the need for a medical evacuation in the rare event the local hospital cannot provide the necessary level of care.

The efficiency of this process depends entirely on the quality of your insurer and their established relationships on the ground. Insurers with robust medical networks can secure payment guarantees much faster, cutting through administrative hurdles when every minute is critical.

Ultimately, accessing quality healthcare in Vietnam as a foreign national is a matter of preparation. Choosing an insurance policy with a strong direct-billing network is not a luxury—it is the core of your strategy for ensuring you receive the best possible care, immediately, without financial complications.

How Vietnam's Booming Insurance Market Benefits You

Vietnam's dynamic economy is not just reshaping skylines; it is fundamentally transforming its insurance sector. For the astute international professional, this development is exceptionally positive. The market is evolving beyond basic, one-size-fits-all coverage toward sophisticated, responsive insurance products engineered for discerning clients.

The metrics are compelling. The market for travel medical insurance in Vietnam was valued at approximately USD 88.4 million in 2024. Projections indicate an expansion to USD 221.23 million by 2033, reflecting a compound annual growth rate of 10.73%. This growth is fueled by a heightened post-pandemic awareness of risk, with industry reports suggesting a significant majority of travelers now intend to purchase insurance.

For you, this domestic boom translates into increased competition among international insurers. This competition compels them to offer superior products, enhanced benefits, and more refined service. You can learn more about the drivers behind this market expansion should the underlying economics interest you.

The key takeaway is that this market maturation places better, more flexible insurance tools directly at your disposal.

The Rise of Traveler-Centric Digital Services

Insurers now understand that for a busy executive, time is the most valuable commodity. The antiquated processes of managing paperwork and enduring long-hold-time international calls are obsolete. Intense competition in the Vietnamese market has accelerated the deployment of digital services designed for convenience and efficiency.

Here are several game-changing advancements you should now expect as standard:

- Instant App-Based Claims: Eliminate mailed receipts. Simply photograph your documents with your smartphone, upload them to a secure app, and receive real-time updates on your reimbursement. The process is both rapid and efficient.

- 24/7 Telehealth Consultations: Address a minor health concern at any hour. Instead of locating a clinic, you can engage in a video consultation with a qualified, English-speaking physician for immediate advice.

- Digital Policy Management: Your entire policy—including coverage details, proof of insurance, and directories of in-network hospitals—now resides within a dedicated mobile application on your phone.

These tools transform your insurance from a passive document into an active support system, delivering immediate, practical value on the ground.

More Flexible and Tailored Policy Structures

As the market matures, insurers are abandoning the one-size-fits-all model in favor of more intelligent product designs. They are now crafting policies for specific travel patterns, demonstrating a nuanced understanding of the needs of individuals who are constantly mobile or undertaking longer-term assignments.

The modern insurance product for Vietnam is no longer just a policy; it's a service package. This shift means you can now select coverage that mirrors your exact travel agenda, whether it's a series of short-term business trips or an extended semi-residential stay.

This evolution is most apparent in the rise of specialized plans like annual multi-trip policies. These provide continuous coverage for a full year, removing the repetitive task of purchasing a new plan for each departure. We are also seeing a proliferation of long-stay plans, offering robust protection for multi-month assignments or sabbaticals.

This level of flexibility ensures your protection is both cost-effective and perfectly synchronized with your international lifestyle. While many leverage leading travel blogs for destination inspiration, it is this new generation of insurance products that makes such diverse and demanding journeys strategically viable.

The Strategic Advantage of Using a Specialized Insurance Broker

Candidly, selecting the right medical insurance for Vietnam is a complex undertaking. The market is saturated with policies laden with technical jargon and nuanced exclusions that can render a plan ineffective at the moment of need.

For busy professionals, the time required to properly vet these options is a luxury few can afford, and the consequences of an incorrect choice are significant.

This is where a specialized insurance broker becomes not just helpful, but an essential strategic partner. A broker functions less like a salesperson and more like your personal risk advisor. Their role is to understand your specific circumstances—your health profile, travel patterns, and risk tolerance—and then survey the entire market to identify the optimal solution.

This expert guidance saves a considerable amount of time and eliminates the guesswork from securing premier protection.

An Advocate in Your Corner

The true value of a skilled broker is most evident during a crisis. They are more than an intermediary during the procurement process; they become your dedicated advocate, particularly during a claim.

Imagine a medical emergency in Vietnam. Instead of searching through policy documents, your first call is to your broker. They possess an intimate knowledge of the system, can liaise directly with the insurer's assistance teams, and ensure your case receives the urgent, professional attention it warrants.

A specialized broker is your advocate and translator in the complex world of international insurance. They simplify the selection process and, more importantly, champion your interests during a claim, ensuring a seamless experience from start to finish.

This advocacy is an invaluable asset, transforming a potentially stressful and confusing event into a managed, controlled process. The service we provide at Riviera Expat is founded on this exact white-glove approach, offering clarity and confidence for every healthcare decision. You can learn more about our client-focused philosophy.

Market Intelligence and The Best Solutions

An expert broker is immersed in this market daily. They are privy to trends and innovations that can directly benefit you.

For example, the Vietnam travel insurance market is experiencing a wave of digitally integrated products that offer exceptional convenience. These include policies with features like cashless hospital admissions and access to vast global medical networks, which dramatically reduce logistical burdens for travelers.

An experienced broker knows which insurers are offering these advanced products and can align them with your needs, ensuring you secure the best possible terms and features available. You can find out more about these innovative market trends.

Ultimately, engaging a broker is about ensuring your policy is not merely "adequate," but perfectly optimized for your specific requirements in Vietnam. This strategic approach provides peace of mind, knowing your health and finances are properly protected by a hand-selected plan. It frees you to concentrate on what truly matters—your professional objectives and your time in this dynamic country.

Your Questions, Answered

Navigating the complexities of international insurance can be daunting, but a few direct answers can provide significant clarity. Here are the most common and pressing questions we receive from professionals planning travel to Vietnam.

These responses are designed to be practical and direct, empowering you to make confident, well-informed decisions.

Is Travel Medical Insurance Mandatory for Entry into Vietnam?

No, the Vietnamese government does not currently require proof of travel medical insurance for entry. However, this legal technicality should not be mistaken for prudent counsel.

For any high-net-worth individual, robust insurance is a non-negotiable component of intelligent travel planning. International-standard hospitals in Vietnam operate on a "pay-first" basis. Without insurance, a serious medical event or an emergency evacuation could result in catastrophic personal expense. A premium policy is the only effective tool for neutralizing that substantial financial risk.

What Is the First Step in a Medical Emergency in Vietnam?

Your immediate priority is to get to the appropriate medical facility. In major cities such as Ho Chi Minh City or Hanoi, this invariably means a private international hospital.

Then, as soon as is practical, you or an associate must call the 24/7 emergency assistance hotline provided by your insurer. This single phone call activates a critical support system. The assistance team will immediately begin coordinating with the hospital, arranging payment guarantees to ensure treatment commences without delay, and assessing if a medical evacuation may be required.

How Are Pre-Existing Medical Conditions Typically Handled?

This is a crucial detail, and the answer varies significantly between policy types. Most standard, short-term travel insurance plans will explicitly exclude pre-existing conditions.

Some may offer a "pre-existing condition waiver," but this typically comes with stringent conditions: the policy must be purchased within a narrow window, often just 14-21 days after making your initial trip deposit. For professionals with chronic or ongoing health concerns, an International Private Medical Insurance (IPMI) plan is a far superior solution. These global health plans are specifically designed to cover both emergency and routine care for such conditions, providing a level of security that short-term policies cannot match.

Executing these details correctly is precisely where expert guidance makes a definitive difference. At Riviera Expat, we specialize in matching high-level professionals with international medical insurance that aligns with their unique needs, ensuring total clarity and confidence for every journey. Contact us for a complimentary consultation.