Think of secondary health insurance as your financial backstop—the layer of protection that activates when your primary health plan reaches its limits. For high-net-worth individuals and global finance professionals, this is not an optional extra. It is a strategic tool designed to eliminate unexpected out-of-pocket expenses and preserve your wealth. It serves as the second line of defense, ensuring access to premier medical care regardless of where a business engagement or personal journey takes you.

Securing Your Global Lifestyle With Secondary Health Insurance

If you operate in major global hubs like Singapore, London, or Hong Kong, relying solely on a standard domestic or even a generous employer-provided health plan can create a dangerous false sense of security. The reality is that these primary policies are often designed with limitations—such as restrictive geographic limits, surprisingly low coverage caps for major medical events, or no access to the elite specialists you would demand in a crisis. This is precisely where secondary health insurance demonstrates its value.

A useful way to visualize this is to think of your health coverage as a fortified structure. Your primary plan is the foundation; it is solid and handles routine, expected medical needs. But a secondary policy is the heavy-duty framework built upon it, engineered to withstand the kind of pressure that would fracture that foundation—a serious illness, a major accident abroad, or a lengthy, complex treatment.

The Strategic Value of Layered Coverage

For a portfolio manager, investment banker, or family office executive, calculated financial exposure is an integral part of your professional life. However, that logic should never apply to your personal health. A secondary health insurance policy is a deliberate move to de-risk your personal finances from healthcare shocks.

The entire purpose of this additional coverage is to ensure you never have to make a healthcare decision based on cost. It serves several critical functions:

- Gap Coverage: It covers the deductibles, co-insurance, and co-payments your primary insurer leaves for you to pay.

- Expanded Network Access: It can unlock a much wider network of premier hospitals and specialists that may be outside your primary plan's approved list.

- Catastrophic Protection: Crucially, it provides a high-limit safety net for severe medical events where costs can surpass a primary plan’s maximum payout in an instant.

This layered approach ensures a medical emergency does not spiral into a financial crisis. It allows you to focus on one thing—recovery—without the stress of disputing claims with insurers or facing six-figure medical bills.

Understanding the Market’s Importance

The growing demand for this kind of protection is not merely anecdotal; market data confirms the trend. The supplemental health insurance market—which often functions as secondary coverage—reached a value of US$38.62 billion in 2023. This is not a niche product; it is a vital tool for professionals navigating complex, expensive healthcare systems around the world.

Projections show this market is expected to expand to US$65.19 billion by 2034, a trend fueled by soaring medical costs and the undeniable need for specific protection against critical illnesses and significant hospital expenses. You can learn more about the supplemental health market growth here.

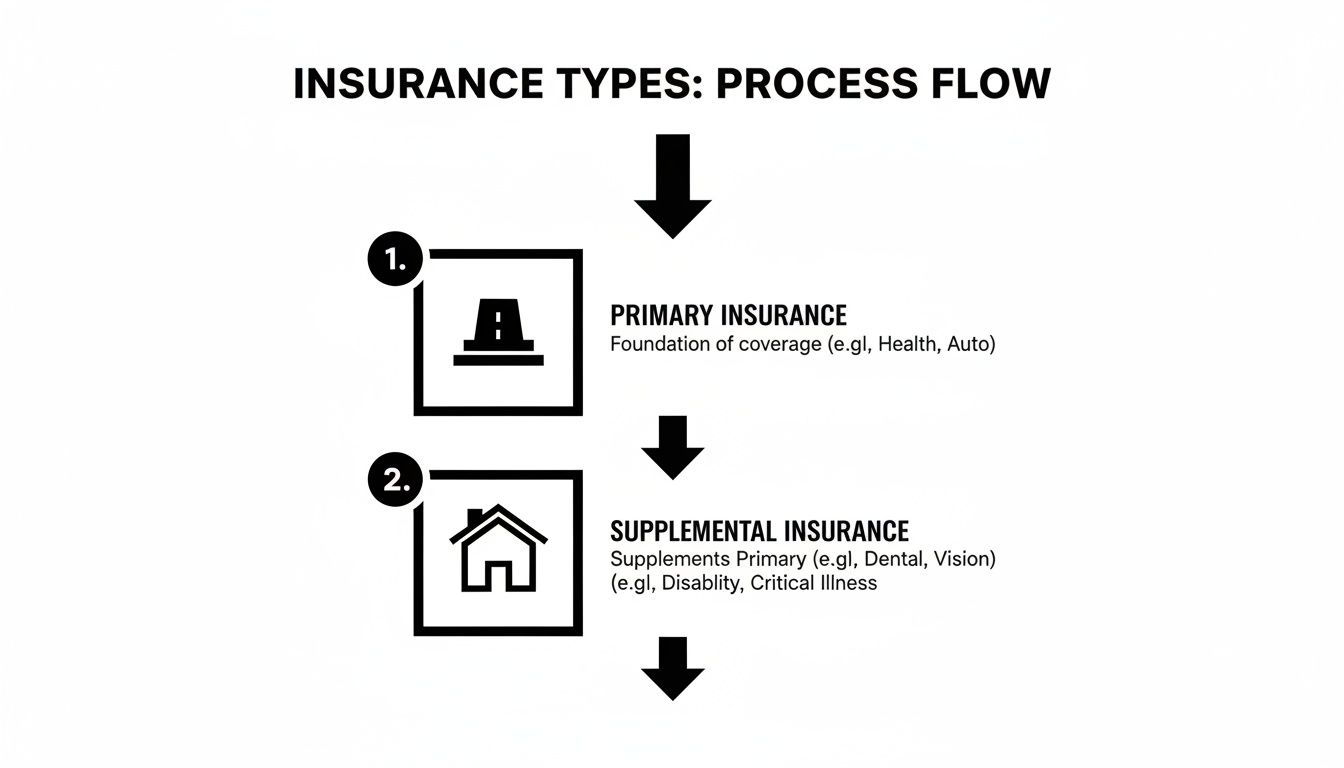

Distinguishing Primary, Secondary, and Supplemental Policies

In the world of finance, precision is paramount. A misplaced decimal point can be catastrophic. The same absolute clarity is required for your health insurance portfolio, because misunderstanding the terminology can expose you to crippling financial risk.

Let's dissect the distinct roles of primary, secondary, and supplemental health insurance. Consider it like constructing a fortress to protect your wealth and well-being.

Your primary health insurance is the foundation. It is the first line of defense, the policy that pays first on any medical claim. This could be your main international plan or an employer-sponsored group policy. It is built to handle the bulk of your expected medical expenses.

But even the strongest foundation has its limits. This is where secondary health insurance comes into play.

The Role of Secondary Coverage

If primary insurance is the foundation, secondary coverage is the structural framework—the walls and roof built upon it. It is a completely separate, comprehensive health plan designed to activate only after your primary plan has paid out its maximum benefit.

It is not a minor add-on; it is a strategic second layer of heavy-duty protection.

Imagine a major medical event costs $250,000, but your primary international plan has a coverage limit of $150,000. Your secondary plan is designed to step in and cover the remaining $100,000 balance (according to its own terms and conditions). This is how you defend your assets against a catastrophic health crisis that could otherwise deplete them.

Where Supplemental Policies Fit In

Now, what about the smaller, more predictable costs? This is the function of supplemental insurance. Think of these policies as the targeted security systems of your fortress—the alarms and reinforced doors.

Unlike a secondary policy, a supplemental plan is not a comprehensive health plan. Its purpose is much more specific: to help you pay for the out-of-pocket costs built into your primary plan.

These policies are surgical, designed to cover items such as:

- Deductibles: The amount you pay before your main insurance begins paying.

- Co-payments: The fixed fee you pay for a doctor’s visit or prescription.

- Co-insurance: The percentage of the bill for which you are responsible after the deductible is met.

A supplemental plan helps you manage the predictable, smaller costs of using your insurance. A secondary plan protects you from the unpredictable, massive costs that completely surpass your primary insurance's limits.

Understanding this distinction is crucial. Mistaking a limited supplemental policy for a comprehensive secondary plan is a common and incredibly expensive error. You can become more familiar with these critical differences by reading our guide on expat medical insurance policy terms explained.

To make this crystal clear, here is a simple breakdown of how these policies function.

Primary vs Secondary vs Supplemental Insurance At A Glance

This table outlines the core function and best application for each type of coverage, helping you see exactly where each piece fits into a robust protection strategy.

| Policy Type | Primary Function | Coverage Scope | Best Use Case For HNW Expats |

|---|---|---|---|

| Primary | Pays first on all medical claims. | Broad, covering a wide range of medical services up to a defined limit. | The foundational domestic or international plan covering day-to-day and major medical needs. |

| Secondary | Pays after the primary plan has paid its maximum benefit. | Comprehensive, mirroring or extending the primary plan's coverage. | Protecting against catastrophic expenses that exceed primary policy limits or accessing wider networks. |

| Supplemental | Reimburses for specific out-of-pocket costs. | Narrow, targeting costs like deductibles, co-pays, or specific events (e.g., cancer, accident). | Mitigating the known, smaller costs associated with using the primary health plan. |

For a global professional, mastering these distinctions is non-negotiable. It is the key to building a multi-layered, intentionally designed insurance strategy that shields both your health and your wealth, ensuring you are not left vulnerable by a single point of failure.

How Coordination of Benefits Actually Works

When you hold more than one health insurance policy, a critical question arises: how do they work together to cover your medical bills? The answer lies in a standard industry process called Coordination of Benefits (COB). This is not an optional feature; it is the universal rulebook insurers use to determine who pays first and to prevent duplicate payments for the same service.

Think of COB as the air traffic controller for your insurance claims. It directs which policy pays first (the primary) and which pays second (the secondary). This system ensures a smooth flow of payments, maximizing your coverage and minimizing what you pay out-of-pocket. Without these rules, the claims process would descend into chaos, leaving you caught in the middle.

The entire point is to ensure the total payout from all your plans never exceeds 100% of the actual medical bill. It is a cost-control mechanism that protects both you and the insurers from overpayment and potential fraud.

This visual shows how primary, secondary, and supplemental policies stack up to create layers of financial defense.

As you can see, the primary policy is your foundation. The other policies build upon it, reinforcing your financial protection against major medical events.

The Claims Workflow Step by Step

Let’s demystify how these layers of protection actually interact when a claim occurs. The process is logical and sequential, ensuring each policy performs its part in the correct order.

Here is how a typical claim flows:

- Initial Claim Submission: After you receive medical care, the claim is sent to your primary insurer first. This is the plan legally designated to pay before any others (for example, your own employer's plan pays before your spouse's).

- Primary Insurer Review: Your primary insurer processes the claim according to its terms. It pays its share, leaving a remaining balance that might include your deductible, co-insurance, or costs that exceed the policy's limits.

- Explanation of Benefits (EOB): The primary insurer sends you an EOB. This is a critical document that details what was billed, what they paid, and what you still owe.

- Submission to Secondary Insurer: You then submit the remaining bill, along with the EOB from your primary plan, to your secondary health insurance provider.

- Secondary Insurer Review: The secondary insurer reviews the EOB and the remaining charges. It then pays its portion based on its own policy terms, reducing your out-of-pocket costs even further.

The core principle is straightforward: the secondary plan assesses what the primary plan has already paid. It then calculates its liability on the remaining eligible balance, ensuring you receive the maximum possible benefit from holding both policies.

A Real-World Scenario In Hong Kong

Let's make this concrete. Imagine an investment banker on a long-term assignment in Hong Kong. He has a primary international health plan through his firm and a personal secondary policy for catastrophic events.

He requires unexpected emergency surgery that costs $120,000. His primary plan has a $75,000 limit for this procedure and a $5,000 deductible.

Here is the breakdown:

- First, the hospital submits the $120,000 claim to his primary insurer.

- The primary plan processes it. The banker is responsible for his $5,000 deductible. The insurer then pays its maximum of $75,000.

- This leaves a remaining balance of $40,000 ($120,000 – $5,000 deductible – $75,000 payment).

- The EOB from the primary plan and the remaining $40,000 bill are then submitted to his secondary insurer.

- The secondary plan, designed for exactly this kind of gap, covers the remaining $40,000 in full.

In this case, the COB process worked perfectly. The banker’s total out-of-pocket cost was just his $5,000 deductible, shielding his personal assets from a substantial medical bill. Understanding this process is vital, especially when navigating features like pre-authorisation and direct settlement, which can make the payment process even smoother.

When Does a Second Health Policy Become a Necessity?

For professionals operating at the highest levels, a standard, single insurance policy is rarely sufficient. Even a generous plan from your employer often contains limitations that only become apparent during a crisis. It is in these high-stakes moments that the value of a well-planned secondary health insurance policy becomes undeniable.

These are not far-fetched "what-if" scenarios. They are the realities for global professionals whose careers are built on mobility, flexibility, and access to the absolute best resources—including healthcare. A secondary policy is not a luxury; it is a critical financial backstop, protecting both your health and your wealth when your primary coverage inevitably falls short.

Let’s examine a few real-world situations where this second layer of protection is non-negotiable.

The Digital Nomad Trader With Cross-Border Needs

Consider a quantitative trader who divides her time between Bangkok and Kuala Lumpur. Her primary insurance is a top-tier domestic plan from her home country, but it is designed for that country alone. It treats international care as a last-resort emergency option, imposing severe limits on anything out-of-network.

While in Bangkok, she develops a condition requiring specialized, ongoing treatment. The premier facility for her specific issue is located in Kuala Lumpur. Her primary plan resists, agreeing to cover only a small fraction of the costs at what they classify as a non-preferred, out-of-country hospital.

This is exactly where a secondary health insurance plan built for an international lifestyle proves its worth. It can be structured to create a seamless, in-network experience across multiple countries. The secondary policy steps in to cover the significant portion of the treatment costs in Kuala Lumpur that her primary plan denied. She receives the best care without derailing her finances or her career.

The Executive Requiring Elite Specialist Access

Think of a family office executive in Singapore. His employer provides a solid group health plan, but it is tied to a rigid network of local hospitals and physicians. It is perfectly adequate for routine check-ups, but it becomes a major obstacle when something complex arises.

He is diagnosed with a rare condition. The world’s leading specialist for it practices in London—well outside his primary insurer's network. The primary plan flatly refuses to cover the consultation and treatment, classifying it as an elective, out-of-network procedure. He is suddenly facing a potential bill exceeding $200,000.

A robust secondary policy resolves this instantly. It can be selected specifically for its broad, open-network access, giving him the freedom to choose any doctor, in any location. The secondary plan coordinates with the primary, covering the costs for the London specialist and ensuring he receives world-class care without having to liquidate assets or jeopardize his family's financial security.

In these situations, secondary coverage is not just about money; it’s about control. It provides the freedom to make healthcare decisions based on medical excellence, not on the restrictive terms of a primary insurance contract.

The Expat Banker Facing Catastrophic Coverage Gaps

An investment banker relocates to Hong Kong with what appears to be a comprehensive health plan from his firm. The policy looks excellent on paper, with a coverage limit of $500,000 per year. However, a sudden, severe accident leads to a prolonged stay in intensive care, multiple complex surgeries, and a grueling rehabilitation period.

The total medical bill surpasses the $500,000 annual limit of his primary plan. Without another layer of protection, that banker is now personally liable for every single dollar above that cap—an amount that could easily spiral into six or even seven figures.

This is the classic scenario where secondary insurance is indispensable. A secondary policy with a high catastrophic limit (for instance, $2,000,000 or more) is designed to activate the moment the primary plan is exhausted. It seamlessly covers all subsequent costs, shielding the banker from a financially ruinous event. For any high-net-worth individual, this protection is just as vital as any other component of their wealth management strategy.

Evaluating Critical Features in a Secondary Health Policy

When constructing a financial portfolio, you scrutinize every asset for its real value, not just its price tag. Your secondary health insurance policy demands the exact same discerning eye. Disregard the headline premium for a moment; the true worth of a policy lies buried in its structure—the features that dictate how, when, and where your coverage will actually perform when a crisis occurs.

Let’s be clear: not all secondary policies are created equal. You can have two plans with nearly identical premiums offering vastly different levels of real-world protection. For a global professional, identifying these differences is the key to choosing a policy that acts as a genuine safety net, not a costly liability with hidden deficiencies.

We will move past the glossy brochures to dissect the critical elements that determine a policy's strength. This is about understanding the core features that directly impact your annual costs and, more importantly, the quality of care and financial security you can rely on.

Deconstructing the Core Coverage Components

At the heart of any policy are the financial levers that control your exposure and the insurer's liability. These are the first things you must examine because they form the foundation of your protection. An error here could result in a huge, unexpected bill—completely defeating the purpose of your secondary plan.

Here are the key financial features to put under the microscope:

- Deductible Levels: This is the amount you pay out-of-pocket before your secondary insurer begins to pay. A higher deductible means a lower premium, but it must align with your primary plan's limits to avoid a dangerous gap where you are liable for all costs.

- Coverage Limits: This is the maximum amount the policy will pay, either per year or over the policy's lifetime. For a secondary plan designed to handle catastrophic events, this number needs to be substantial—often in the millions—to be a true safety net.

- Co-insurance and Out-of-Pocket Maximums: Even after your deductible is met, some plans require you to pay a percentage of the costs (co-insurance) until you reach a certain cap. A strong policy will have a clearly defined and reasonable out-of-pocket maximum.

Understanding how these three elements work together is vital. If you wish to go deeper, we have broken down these terms in our detailed article on excesses and deductibles in the fine print.

Assessing Operational and Geographic Scope

For an international professional, a policy's real-world utility is determined by its operational flexibility. The best financial terms on paper are worthless if the plan does not allow you to receive care where you actually live, work, and travel. This is where the fine print on geographic scope and provider access becomes non-negotiable.

Your policy must match your global footprint. Ask these questions:

Geographic Scope: Does the policy offer true worldwide coverage, or does it exclude certain regions? The USA is the most common exclusion due to its high healthcare costs. Ensure the "area of cover" explicitly includes every country you frequent.

Provider Network Access: Are you restricted to a defined network of hospitals, or does the plan offer "open access," allowing you to see any licensed provider you choose? For anyone who desires access to the best specialists without compromise, an open-access plan is essential.

Examining Exclusions, Riders, and Waiting Periods

Finally, you must investigate the clauses that detail what is not covered, what you can add, and when your coverage actually begins. This is often where unwelcome surprises are hidden.

- Exclusions: Every policy has them. Look for specific exclusions related to pre-existing conditions, so-called high-risk activities, or certain types of treatments.

- Waiting Periods: Some benefits, especially for major procedures or maternity care, will not be active until you have held the policy for a specified period.

- Riders: These are optional add-ons that can fill critical gaps. Consider riders for critical illness, dental, and vision, or—crucially for expats—emergency medical evacuation. If you reside far from your home country, an evacuation rider is not a luxury; it is a necessity.

By methodically reviewing these features, you can look past the premium and see the true strategic value of a secondary health insurance policy. It is how you ensure your plan provides the control and security your global lifestyle demands.

A Decision Framework for Selecting the Right Policy

Choosing the right secondary health insurance is not a matter of chance. It demands the same structured, deliberate approach you would apply to managing a high-value asset. A methodical process ensures the policy you select delivers the precise protection your global lifestyle requires. It cuts through the noise, eliminates ambiguity, and places you in absolute control of your healthcare choices.

This framework breaks the process down into a logical self-assessment and a critical provider evaluation. Think of it as your blueprint for making a strategic choice, not just a purchase.

Phase One: Your Personal Risk Profile

Before you consider speaking to an insurer, you must conduct a rigorous internal audit. Your personal and professional life dictates the architecture of the ideal policy. This first step is about quantifying your needs with precision.

This internal data allows you to filter the market effectively. It prevents you from overpaying for benefits you will never use or, far worse, being underinsured against the risks you actually face.

Start with these core areas:

- Geographic Footprint: Detail your annual travel frequency. List every country in which you work or visit regularly, paying special attention to high-cost healthcare regions like the USA.

- Family Requirements: Assess the current and future healthcare needs of your spouse and children. Are specialized pediatric needs on the horizon? What about aging parents who might join you abroad?

- Provider Preferences: Do you have non-negotiable doctors or hospitals? If you require unrestricted access to specific world-renowned specialists or medical institutions, an open-access policy is not a luxury—it is a requirement.

- Financial Risk Tolerance: Define the maximum out-of-pocket expense you are willing to personally absorb in a worst-case medical scenario. This figure will directly shape the ideal deductible and co-insurance structure for your policy.

Phase Two: Vetting the Insurer and Policy

With a crystal-clear picture of your needs, you can now critically evaluate potential insurers and their offerings. This phase is about looking past the marketing materials to scrutinize an insurer’s operational integrity and the real substance of their contracts.

The strength of an insurance policy is ultimately determined by two things: the insurer's ability and its willingness to pay claims promptly and fairly. An insurer’s financial stability rating (from agencies like A.M. Best or S&P) is a crucial, non-negotiable indicator of their long-term reliability.

When you begin discussions with providers, your goal is to demand clarity and accountability. Do not hesitate to pose direct questions designed to expose any potential weaknesses in their coverage or service model.

Key Questions for Providers:

- Claim Processing: What is your average turnaround time for processing a secondary claim after you receive the primary insurer’s Explanation of Benefits?

- Direct Billing Network: Can you provide a list of hospitals within my key geographic areas that offer direct billing, signifying truly cashless service?

- Emergency Assistance: Describe the exact support process for an emergency medical evacuation. Who coordinates the logistics on the ground, and what are the specific limitations or exclusions?

- Integration Protocol: How, precisely, will this new secondary policy integrate with my existing primary plan? What specific steps must I take to ensure a seamless Coordination of Benefits process when a claim occurs?

By following this two-phase framework, you transform a complex, often confusing purchase into a managed, strategic process. This systematic approach ensures your secondary health insurance selection is an informed decision that provides one thing above all else: complete peace of mind.

Common Questions About Secondary Health Insurance

When you begin layering your financial protection, numerous questions arise. For high-net-worth individuals and finance professionals, getting the details right is paramount. Here are the direct answers to the most common questions we receive about secondary health insurance.

Let's clarify what this type of coverage is, and what it is not.

Can I Just Buy a Secondary Policy on its Own?

No, and this is a critical point. A secondary health insurance policy is not designed to be your sole line of defense. It can only function after your primary policy has processed a claim.

It simply cannot work as a standalone plan. Its entire purpose is to activate after your primary insurer has processed a claim, paid its share, and issued an Explanation of Benefits. It is a supplementary layer, not the foundation.

How is This Different From a Health Savings Account (HSA)?

These two serve completely different purposes in your financial toolkit. Secondary health insurance is a risk-transfer product. You pay a premium to an insurance company, and in return, they assume the risk of covering specific, potentially massive, medical costs.

A Health Savings Account (HSA), on the other hand, is a tax-advantaged savings account that you own and fund. You contribute pre-tax dollars to pay for qualified medical expenses.

An insurance policy is about protecting you from catastrophic costs that could run into hundreds of thousands, potentially paying out far more than you ever contributed. An HSA is an excellent tool, but its utility is limited to the exact amount of money you have deposited into it.

Will My Secondary Health Insurance Cover Me Outside My Home Country?

This depends entirely on the policy. For expats and global professionals, this is the most important question to ask. A standard secondary plan purchased for domestic use in your home country will almost certainly offer no coverage once you cross the border.

This is where specialized International Private Medical Insurance (IPMI) is essential. These plans are designed from the ground up for a global lifestyle and can be structured to act as either primary or secondary coverage worldwide. You must verify the geographic scope of any policy you consider. For an international professional, this is the central feature.

At Riviera Expat, we build bespoke international health insurance solutions specifically for financial professionals living and working in global hubs. We deliver the clarity you need to construct a healthcare strategy that’s as resilient and mobile as you are. Secure your expert consultation today.