Navigating medical insurance for France requires an appreciation for its renowned dual-system. For discerning expatriates, the optimal strategy is consistently a blend of the state-provided public insurance with a robust private top-up policy. This combination is the key to unlocking seamless, immediate access to one of the world's most sophisticated healthcare systems.

Navigating French Healthcare as an Expat

France is home to a healthcare system that consistently ranks among the best globally for quality and accessibility. For an expatriate accustomed to a superior standard of living, understanding its unique structure is the first step toward securing complete peace of mind. The system is not a monolithic entity but a refined partnership between the public and private sectors.

Consider it analogous to commissioning a bespoke automobile. The public system is the powerful, reliable engine and chassis—it provides the strong, essential foundation available to all legal residents. Your private insurance is the custom interior, the advanced technology, and the personalized features that deliver superior comfort, choice, and performance.

The Dual System Advantage

This two-tiered model is a significant benefit for anyone seeking truly comprehensive coverage. The two components you must understand are:

- Public Insurance (PUMA): Officially the Protection Universelle Maladie, this is the state-funded foundation. It guarantees access to necessary medical care for all legal residents after a mandatory residency period of three months.

- Private Top-Up Insurance (Mutuelle): This is the complementary policy, meticulously designed to cover the costs the public system does not, ensuring you have minimal—or zero—out-of-pocket expenses for an extensive range of services.

This structure allows you to benefit from the security of a universal system while layering on the choice and exclusivity that premier private insurance provides. It is a framework engineered for both universal access and individual preference.

For discerning individuals, the synergy between public and private insurance is key. It transforms excellent healthcare into an exceptional and seamless experience, eliminating financial friction and prioritizing personal well-being.

Crafting Your Healthcare Strategy

Your entry into the French system begins with a clear, strategic plan. The objective is to construct a seamless healthcare solution tailored to your specific needs and lifestyle, leaving no gaps in your coverage. This involves a clear understanding of the enrollment processes for both the public system and the private market.

We will detail how to enroll, what you can expect from each tier, and how to integrate them effectively. Executed correctly, this strategy ensures your health is protected by a world-class system, freeing you to focus on enjoying your new life in France. This guide provides the insights needed to build that strategy with confidence.

Understanding Your Public Health Insurance Options

The French public health system is a cornerstone of life in the country, built on the principle that every legal resident deserves quality medical care. This is managed through the Protection Universelle Maladie (PUMA), a system designed as a robust safety net for all, from French citizens to expatriates.

However, access is not immediate. A critical detail for your relocation plan is the requirement to establish stable and regular residency in France for at least three consecutive months before you are eligible to apply. This waiting period is non-negotiable and must be factored into your timeline.

The Path to Public Coverage

Once you have met the three-month residency requirement, your next step is to engage with the local health insurance authority, the Caisse Primaire d'Assurance Maladie (CPAM). The CPAM serves as your primary portal to the public healthcare system.

The application process is meticulous, and documentation must be precise. To secure approval, you will need to present a comprehensive file proving your identity, residency, and legal status in France.

The required documentation typically includes:

- Your passport

- A long-stay visa or residence permit (titre de séjour)

- Your birth certificate, accompanied by an official French translation

- Proof of address (justificatif de domicile), such as a recent utility bill

- Your French bank account details (a RIB, or Relevé d'Identité Bancaire) for reimbursements

Submitting a complete and correct file to your local CPAM office initiates your enrollment. Be prepared for the administrative process, which can take several weeks or even months. Patience is essential during this phase.

Understanding the Reimbursement System

The French system operates on a co-payment model. You typically pay for medical services or prescriptions upfront, and the state subsequently reimburses a significant portion. Mastering this cash flow is key to managing your finances effectively in France.

The Role of Your Médecin Traitant

A central concept is the parcours de soins coordonnés, or the coordinated healthcare pathway. This framework ensures your care is managed efficiently, beginning with your chosen primary care physician, the médecin traitant.

Declaring a médecin traitant to the CPAM is a mandatory step. This physician becomes your central point of contact for all health concerns, maintaining your medical records and providing referrals to specialists. Adhering to this pathway—consulting your primary doctor first—is how you secure the highest reimbursement rates from the state.

If you fail to declare a primary doctor or consult a specialist without a referral, your reimbursement rates will be substantially reduced. A standard consultation with your médecin traitant is reimbursed at approximately 70%. Bypassing this step significantly lowers the amount you receive back.

The French system’s dedication to universal access is notable. Its statutory health insurance (SHI) model covers 100% of the resident population. In 2021, public and compulsory private schemes financed 85% of all health spending in France—well above the EU average of 81%.

While state coverage is a superb foundation, it does not cover all costs. This is why understanding the nuances of legal contracts is so vital when evaluating any insurance policy. To build a complete, worry-free healthcare strategy for your life in France, you must fill the gaps left by the state system.

Choosing the Right Private Top-Up Insurance

While France's public health insurance provides an excellent foundation, it is deliberately designed not to cover 100% of your medical bills. This is where private complementary insurance, known locally as a mutuelle, becomes absolutely essential for receiving first-rate care without incurring unexpected costs.

Consider the public system the sturdy framework of your healthcare journey. A premium mutuelle, in contrast, is your first-class upgrade—it adds the comfort, choice, and superior amenities that make the experience seamless and worry-free.

A mutuelle works in concert with the state system to cover the remaining costs, a gap known as the ticket modérateur. This is the co-payment left after the state reimburses its typical 70%. With the right plan, your visits to a general practitioner, specialist consultations, and prescriptions can be fully covered.

Elevating Your Coverage Beyond the Basics

For high-net-worth individuals, the true value of a premium mutuelle lies in its coverage for services where public reimbursement is minimal or non-existent. This is where you can truly align your insurance with your personal health priorities and lifestyle.

A top-tier plan moves far beyond simple co-payments. It offers robust financial protection for high-cost treatments, designed for those who expect the best without compromise.

Key areas where a premium mutuelle provides significant value include:

- Advanced Dental Procedures: Securing substantial coverage for treatments like dental implants, orthodontics, and complex restorative work, which are notoriously underfunded by the public system.

- Designer Eyewear: Gaining generous allowances for high-end frames and advanced lens technologies that fall well outside standard state coverage.

- Private Hospital Rooms: Guaranteeing your comfort and privacy during a hospital stay by covering a single room (chambre particulière).

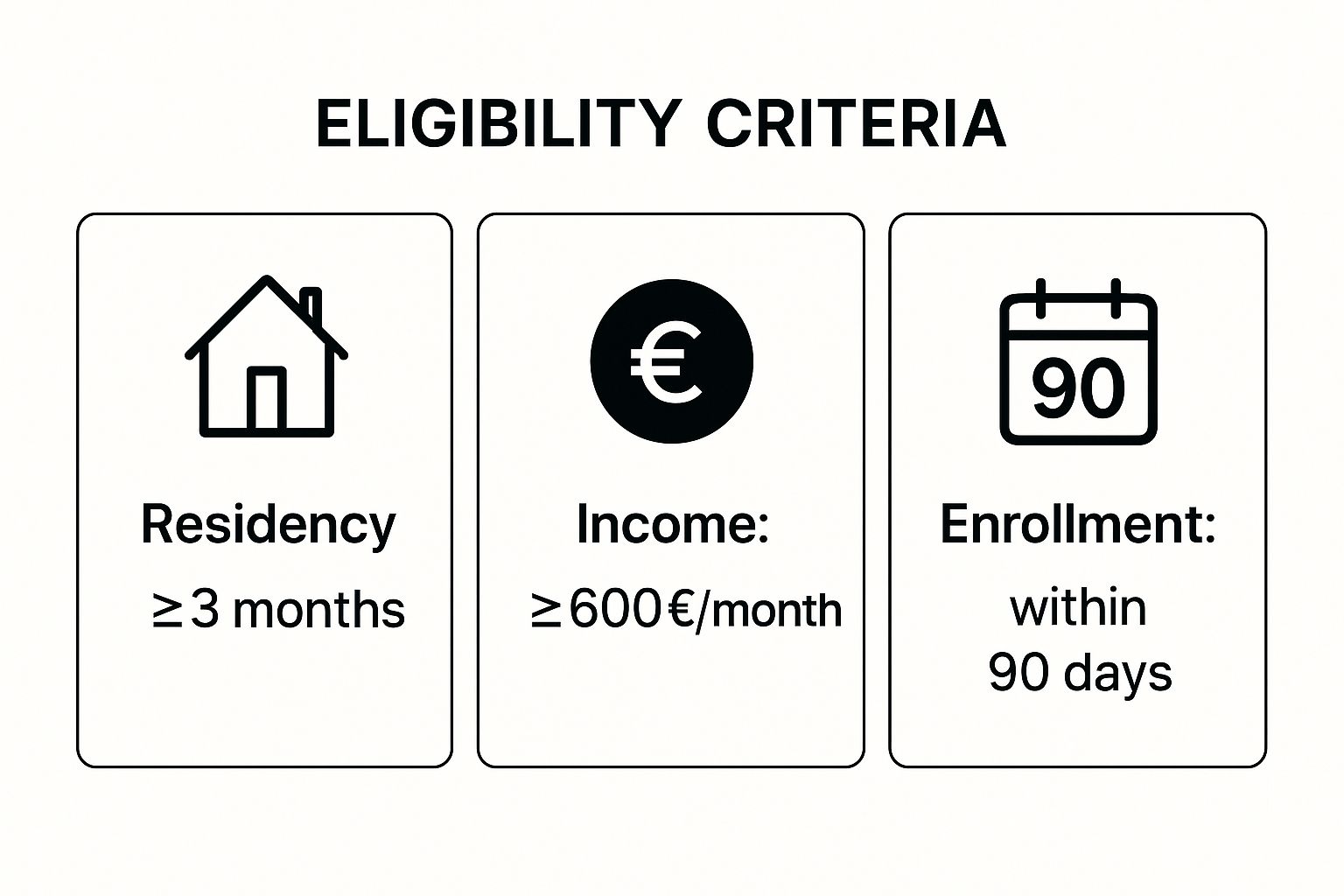

The infographic below outlines the core eligibility criteria for public insurance, which is a prerequisite before adding a private mutuelle.

This reinforces the foundational requirements—residency, legal status, and enrollment timelines—that serve as your gateway into the French healthcare system.

Comparing Mutuelle Tiers for Optimal Selection

Not all mutuelles are created equal. They are typically offered in tiers, with reimbursement levels expressed as a percentage of the state's official base rate for a procedure, the Base de Remboursement (BR). A plan offering "100% BR" will only cover the basic co-payment (ticket modérateur) and nothing more.

Premium plans, however, fundamentally change the scope of coverage. They offer 200% BR, 300% BR, or even higher. These multiples are crucial for covering specialists who charge above the standard rate (known as dépassements d'honoraires) and for high-cost items like premier dental work.

Selecting the right tier requires a realistic assessment of your potential healthcare needs. Consider your family's health history, any planned medical procedures, and your desire for comfort-enhancing services such as osteopathy or private nursing care.

To help you visualize this, here is a breakdown of what you can generally expect from different levels of mutuelle coverage.

Comparing Private Health Insurance (Mutuelle) Tiers

| Coverage Level | Typical Reimbursement Rate | Best For | Example Coverage Areas |

|---|---|---|---|

| Basic | 100% – 150% BR | Healthy individuals needing a simple safety net for standard co-payments. | GP visits, standard prescriptions, basic hospitalization. |

| Mid-Range | 150% – 250% BR | Individuals and families wanting better coverage for specialists and common extras. | Specialist fees with moderate overages, standard eyewear, basic dental work. |

| Premium | 300% BR+ | High-net-worth individuals who demand access to top specialists and private facilities without financial constraints. | Private hospital rooms, advanced dental implants, designer eyewear, alternative therapies. |

Choosing the right plan is a strategic decision. It is about matching your investment to your expectations for healthcare quality and access.

A well-chosen mutuelle is more than just insurance; it’s a strategic tool for managing your health with precision and control. It grants you the freedom to choose leading specialists and access premium facilities without a second thought about the cost.

For those navigating these choices, exploring the different policy types is a vital next step. You can dive deeper into this with our detailed guide on choosing the ideal health insurance plan for expatriates.

Making a Strategic Decision

When you are ready to select your private medical insurance for France, seek a provider specializing in serving expatriates. These firms are invaluable, often providing English-speaking support, streamlined administrative processes, and plans designed to meet the expectations of an international clientele.

Ultimately, your choice should reflect a clear understanding of your personal risk tolerance and healthcare philosophy. By investing in a high-tier mutuelle, you are not just filling a coverage gap—you are securing certainty, choice, and a superior healthcare experience tailored to meet your exacting standards.

Securing Health Insurance Before You Arrive

A critical detail that often surprises prospective expatriates is that arranging your health insurance before you arrive in France is a non-negotiable requirement for your visa. For long-stay visas such as the VLS-TS (visa de long séjour valant titre de séjour), proof of sufficient coverage is an absolute prerequisite.

Securing this in advance ensures you are covered from day one, eliminating dangerous gaps and providing peace of mind. French authorities will demand proof of comprehensive health insurance before approving your visa, so this must be a priority on your pre-move checklist.

Differentiating Travel Policies from Expat Health Plans

It is a common mistake to assume a standard travel insurance policy will suffice. It will not.

A typical travel insurance plan is designed for short-term trips to cover emergencies like lost luggage or holiday medical incidents. It is fundamentally inadequate for an individual establishing residency and will be rejected by the visa authorities.

What you require is a dedicated international health plan specifically designed for expatriates. These policies are structured to meet France’s strict visa requirements and provide the robust, ongoing coverage expected by a high-net-worth individual. For a seamless transition, it is the only viable option.

Think of a proper international health insurance plan as your bridge into the French system. It gives you immediate, high-quality coverage that satisfies visa officials and protects you while you wait out the three-month residency period to become eligible for public healthcare.

The Essential Features of a Premier International Policy

When selecting your plan, a basic, budget policy will not meet your needs. You require a plan that delivers certainty and access to the best care available, without compromise, when it matters most.

Here are the non-negotiable features to look for:

- High Coverage Limits: The policy must provide substantial financial protection, typically €1,000,000 or more, to handle any medical eventuality without financial concern.

- Medical Evacuation and Repatriation: This is a crucial safety net. It guarantees that in a severe medical crisis, you can be transported to a center of excellence or returned to your home country if necessary.

- Zero Deductible Options: The best plans allow you to eliminate out-of-pocket costs on claims, creating a smooth and predictable financial experience.

- Direct Billing Networks: A premium policy should facilitate direct payment to hospitals and clinics. This means the insurer settles the bill on your behalf, so you are not required to pay large sums upfront and await reimbursement.

Ensuring a Seamless Transition

The right international health policy does more than satisfy a visa requirement; it provides genuine peace of mind. It acts as your shield, ensuring that during the initial months before you are integrated into the French public system, both your health and your finances are completely secure.

A significant advantage is choosing a plan with a strong network of English-speaking doctors and support staff. This simple feature dismantles language barriers and makes accessing trusted medical care a straightforward process. By securing this level of coverage before you relocate, you are laying the foundation for a confident and stress-free start to your new life in France.

How Good Is French Medical Care, Really?

When you evaluate health insurance in France, you are not merely purchasing a policy. You are securing access to one of the world's most respected healthcare systems. The quality of care here is a global benchmark and a decisive factor for anyone serious about their long-term health.

The system is engineered to do more than treat illness. It is designed around the patient experience, ensuring you feel heard, respected, and involved in your own treatment from start to finish.

A Focus on Patient-Centered Results

The true measure of any healthcare system is patient satisfaction. On that front, France delivers exceptional results.

Recent data from the OECD indicates that an impressive 91% of patients rate the quality of the care they receive as good or very good. That figure alone speaks to the system's high standards.

Even more telling is that 92% of patients feel their care is person-centered, meaning clinicians actively involve them in the decision-making process. Furthermore, 61% of patients with chronic conditions report their care is well-managed, a testament to the system's ability to handle complex, long-term health issues. You can review the specific data here: the patient experience in the French healthcare system.

The Hallmarks of a World-Class System

Beyond positive patient reports, the quality of the French system is evident in its daily operations. These are the elements that provide peace of mind, knowing your health is in expert hands.

Several key indicators stand out:

- Efficient Access to Specialists: The coordinated care pathway is not mere bureaucracy; it ensures timely referrals to leading specialists in any field required.

- Superior Chronic Care Management: The system is structured to provide proactive and consistent support for individuals managing long-term health conditions.

- Modern Technology Integration: Digital platforms for booking appointments and managing health records are standard, enhancing convenience and efficiency.

For those interested in how sophisticated systems like France’s maintain such high standards, it is worth exploring the principles of knowledge management in healthcare. This is the underlying discipline that powers efficiency and patient-centric care.

The real value of French medical care isn’t just in its clinical excellence—it’s in its reliability. You have the assurance that whatever health challenge comes your way, a sophisticated and responsive network of professionals is there to support you.

Ultimately, whether you rely on the public system, a premium private plan, or a combination, you are connecting to a framework engineered for excellent outcomes. The proof is in the data and the patient experiences: choosing to receive your medical care in France is a sound strategic decision.

Your Optimal Insurance Strategy for France

Structuring your medical insurance for France correctly is not about selecting a single policy. It is about building a multi-layered defense for your health and finances that adapts as you transition from newcomer to long-term resident.

For a discerning expat, the most intelligent strategy combines three distinct layers of coverage. This approach ensures you are fully protected from the moment of arrival, through any administrative waiting periods, and into your established life in France.

Consider it akin to designing a bespoke security system for your well-being. Each component has a specific function, and together they provide total peace of mind.

The Three Pillars of Your Health Coverage

The optimal strategy follows a logical sequence, matching your insurance to each stage of your relocation. By layering your coverage in this manner, you eliminate critical gaps and guarantee access to top-tier care whenever needed.

Here is how the plan unfolds:

- Initial Coverage with International Health Insurance: Before your relocation, secure a comprehensive international policy. This is not merely a visa formality; it is your primary shield for the first few months before you are eligible for the state system. It provides immediate access to high-quality private care from day one.

- Enrollment in the Public System (PUMA): Once you have legally resided in France for at least three months, your next action is to apply for PUMA. This becomes the robust, reliable foundation of your long-term healthcare, covering the majority of your standard medical costs.

- Supplementing with a Premium 'Mutuelle': After you are enrolled in the public system, you add the final, crucial layer: a top-tier private insurance plan, or mutuelle. This policy covers the co-payments and unlocks the premium services that define a superior healthcare experience.

This three-tiered strategy is more than just a safety net; it's an investment in certainty. It gives you the freedom to use one of the world's best healthcare systems entirely on your own terms—with maximum comfort, choice, and financial control.

It is also a strategy that adapts to the realities of French healthcare. With 21.5% of the population aged 65 or over, the demand for specialized care is high. The system is innovating to meet this demand, with platforms like Doctolib® managing an incredible 200 million appointments in 2023.

A flexible insurance plan is essential to navigate this environment, ensuring you can access the best specialists without long delays. You can learn more about these evolving healthcare trends in France.

By layering your insurance this way, you gain the freedom to choose your preferred doctors, secure private hospital rooms, and keep out-of-pocket costs to an absolute minimum. It is how you create a completely effortless healthcare experience in your new home.

Frequently Asked Questions

When arranging medical insurance for France, several key questions invariably arise. Clarifying these details is essential to building a healthcare plan that functions effectively, without unforeseen complications.

Here are precise answers to the most common questions from expatriates.

Do I Need Private Insurance if I Have PUMA?

Yes, it is highly advisable. Consider the public system, PUMA (Protection Universelle Maladie), an excellent foundation. It is robust, but it is not designed to cover 100% of costs.

PUMA typically reimburses approximately 70% of standard medical expenses. This leaves a 30% co-payment that you are responsible for. A private top-up policy, known as a mutuelle, is specifically designed to cover that remainder.

Furthermore, a premium mutuelle offers significant value beyond this gap. It provides far superior coverage for services where public reimbursement is minimal, such as major dental procedures, high-quality optical wear, or the comfort and privacy of a single hospital room.

How Long Does It Take to Get a Carte Vitale?

Obtaining a Carte Vitale—the green card that streamlines reimbursements—is not an immediate process. It is directly linked to your residency status.

First, you must prove you have been living in France legally and continuously for at least three months. Only then can you begin the application to join the public health system (PUMA).

Once you submit your application file to the local CPAM (Caisse Primaire d'Assurance Maladie), the timeline can vary. Depending on the workload of your local office, receiving your social security number and official approval can take from a few weeks to several months. Following approval, you can then apply for the physical Carte Vitale.

Your Carte Vitale is not the insurance itself. It is the key that unlocks the system's efficiency. It automates your reimbursements from the state, simplifying your financial interactions with doctors and pharmacies.

Can I Choose My Own Doctor in France?

Yes, absolutely. The French system provides complete freedom to choose your primary care physician, known as a médecin traitant. In fact, selecting one is one of the most important initial steps you will take.

You must formally declare your chosen doctor to the CPAM. This officially registers you in the parcours de soins coordonnés (coordinated care pathway), which is essential for receiving the highest reimbursement rates.

Your médecin traitant functions as your healthcare coordinator, managing your records and providing referrals to specialists. If you do not declare one, or if you consult a specialist directly without a referral, your reimbursement rates from the public system will be significantly reduced.

As you begin your long-term financial planning in France, it is also prudent to understand how insurance costs evolve. For a detailed analysis, please see our article on why medical insurance premiums tend to rise year after year.

For expert, objective guidance in selecting the ideal international health insurance plan for your transition to France, trust the specialists at Riviera Expat. We provide white-glove service to help you secure the perfect coverage with clarity and confidence. https://riviera-expat.com