For the discerning U.S. citizen living or working abroad, a critical truth must be acknowledged: international health insurance isn’t a discretionary expense, it’s a fundamental component of your asset protection strategy.

Your domestic policy, whether from an employer or Medicare, becomes functionally obsolete the moment you are outside the United States. Relying on it for meaningful protection is a profound financial risk, exposing you to potentially catastrophic medical and financial liabilities. The only method to guarantee access to premier medical care globally is through a dedicated international health plan.

Why Your US Health Plan Is Insufficient

Operating under the assumption that your U.S. health plan will provide adequate international coverage is a significant, and potentially costly, miscalculation. It is akin to attempting to navigate Tokyo's intricate street system with a map of Manhattan; the tool is fundamentally inappropriate for the environment.

American insurance policies are constructed around a specific network of U.S.-based hospitals, clinics, and physicians. Once you are abroad, that network ceases to be relevant.

This is not a subtlety buried in the fine print. It applies to nearly every form of U.S. coverage, from executive-level corporate plans to policies procured on the ACA marketplace. Most critically, U.S. Medicare offers virtually zero coverage for healthcare services rendered outside the United States—a fact the U.S. government makes very clear.

Without appropriate coverage, a minor illness or unforeseen accident can rapidly escalate into a significant financial event. You become personally liable for immediate, out-of-pocket payments that can easily amount to tens or even hundreds of thousands of dollars.

The Strategic Value of Global Coverage

Perceiving international health insurance for US citizens as merely a travel-related cost is to fundamentally misunderstand its purpose. It is a critical element of a sophisticated asset protection strategy, ensuring a medical event does not compromise your financial standing.

A premier international plan provides more than just emergency coverage. It ensures continuous access to high-quality medical support, wherever your professional or personal life may take you.

Consider this: a single medical evacuation, a standard benefit in most quality international plans, can easily exceed $100,000 if paid for out-of-pocket. That potential expense alone demonstrates the immense financial shield a proper global health policy provides.

This level of strategic planning affords several key advantages, particularly for individuals whose endeavors cannot tolerate disruption:

- Direct Access to Elite Facilities: Top-tier plans maintain vast direct-billing networks. This enables you to access the best private hospitals and specialists without the need for upfront payment and subsequent reimbursement claims.

- Comprehensive Wellness Management: Unlike short-term travel policies, a true international plan covers routine diagnostics, preventative care, and management for chronic conditions. It facilitates the maintenance of your health baseline, regardless of your location.

- Uncompromised Peace of Mind: True security is not merely possessing an insurance card. It is the absolute confidence that stems from knowing your health and financial assets are protected by a policy engineered for the realities of a global lifestyle.

Ultimately, securing a dedicated international health insurance plan is not about planning for a temporary trip. It is about constructing a framework of certainty and control. It ensures your health is managed with the same level of diligence and expertise as your investment portfolio—an essential measure for any American operating on the world stage.

What Exactly Is International Health Insurance for US Citizens?

When operating on a global scale, you require instruments that protect both your health and your wealth. International health insurance is one of the most critical, yet frequently misconstrued, of these instruments. Let us be unequivocal: this is not analogous to the short-term travel insurance one might purchase for a two-week holiday.

Consider the distinction: a travel medical policy is a disposable, single-use tool for an acute crisis during a brief trip—a fractured limb on a ski slope or a severe infection. It is designed for immediate stabilization and nothing more.

International health insurance for US citizens, by contrast, is your personal health infrastructure abroad. It is architected for a life lived across borders, providing continuous, comprehensive access to quality healthcare worldwide.

This type of plan is specifically designed for expatriates, global executives, and any individual spending a significant period outside the US, typically six months or longer. It functions as your primary health plan, supplanting the domestic one you would utilize in the United States.

It's All About Comprehensive, Long-Term Care

The entire purpose of a global medical plan is to maintain your standard of care, regardless of your geographic location. This extends far beyond mere emergency response and encompasses a much broader scope of services than any travel policy would contemplate.

A genuine international health plan provides robust coverage for services essential to maintaining your health:

- Routine and Preventive Care: This includes annual physicals, wellness checks, and screenings. The focus is on proactive health management, not merely reactive problem-solving.

- Chronic Condition Management: For individuals managing conditions such as diabetes or hypertension, these plans cover ongoing physician consultations and prescriptions, ensuring continuity of care.

- Major Medical Events: From oncology treatments to complex surgical procedures, a quality plan provides for care at premier international medical facilities.

- Specialist Consultations: You can access specialist care directly, without requiring an emergency referral, mirroring the convenience of a premium domestic plan.

This distinction is paramount. While most affluent Americans possess domestic health insurance, that coverage often becomes irrelevant once they are on foreign soil. International health insurance for US citizens is engineered to address the unique challenges of accessing care abroad, covering everything from emergency evacuations to hospitalizations in countries with vastly different healthcare costs and standards. You can review key US health coverage statistics from the Census Bureau to better understand the domestic landscape these plans are designed to replace.

More Than a Health Plan—It's a Financial Shield

Viewing this type of coverage as a simple expense is a significant strategic error. For any individual with substantial assets, a premier international health plan is a core component of a global financial strategy. It functions as a firewall, protecting your portfolio from the catastrophic costs of a major medical event abroad.

An international health plan isn't just about healthcare; it's about control. It provides the certainty that you can access the best possible care without needing to liquidate assets or derail your financial objectives. It secures both your physical and fiscal well-being.

The best plans eliminate financial friction at the point of care by establishing direct-billing networks with elite hospitals. You present your insurance credentials, and the provider liaises directly with the hospital for payment. This seamless process is essential for individuals who cannot afford delays or administrative complexities when their health is at stake.

Ultimately, this specialized insurance provides the essential framework for a secure and healthy international life.

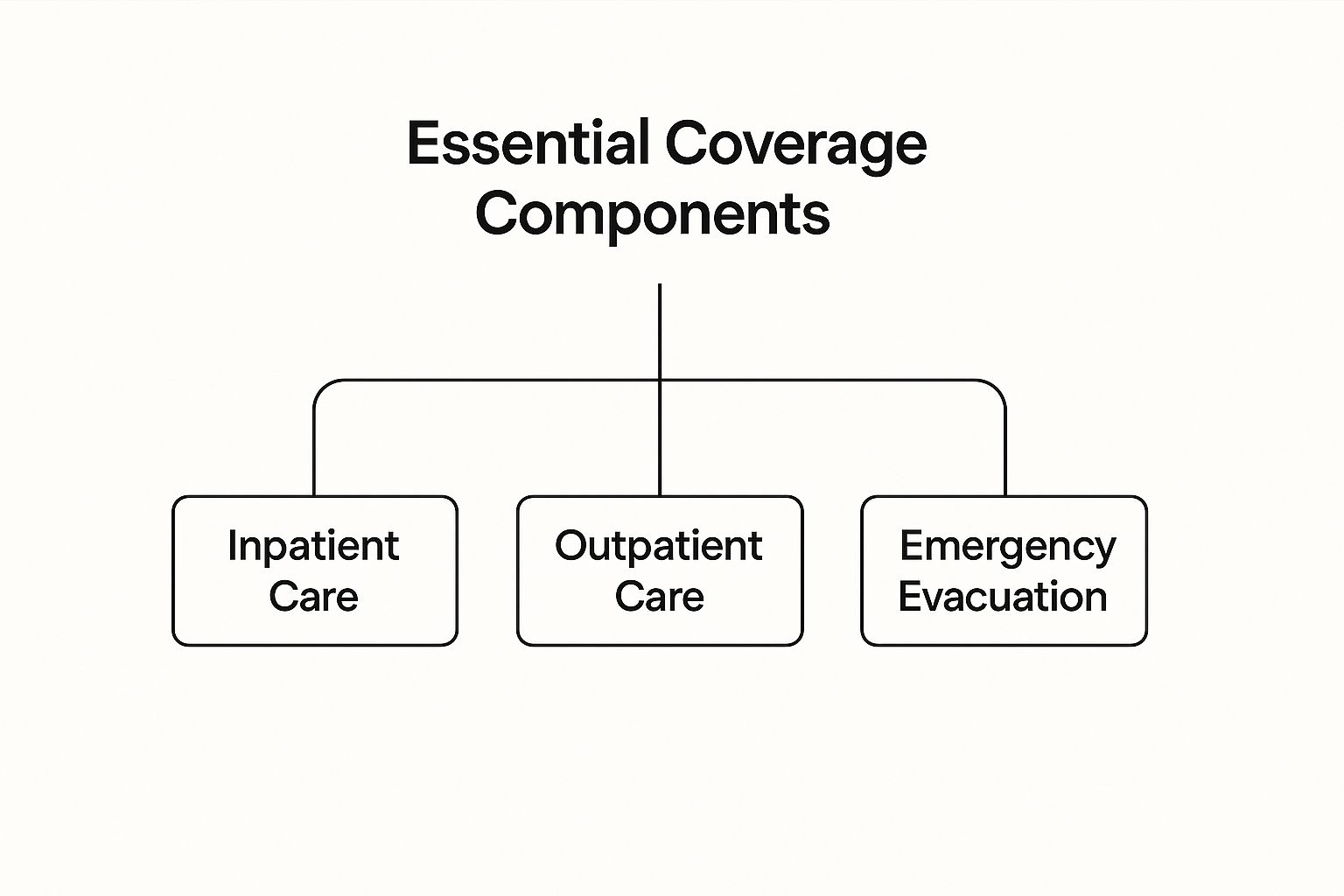

Evaluating Essential Coverage Components

Selecting the right international health insurance is not a matter of comparing superficial features. It requires an analysis of the plan's core architecture. Not all policies are constructed with the same integrity, and understanding the non-negotiable elements is the first step toward securing genuine global protection.

Think of it as inspecting a building's foundation. If certain key elements are deficient, the entire structure is compromised. A premier plan is built upon three critical pillars: comprehensive inpatient care, robust outpatient services, and emergency medical evacuation. These form the bedrock of any policy worthy of your investment.

The infographic below illustrates how these components integrate to form a truly superior health plan.

As you can see, a top-tier policy is not defined by a single feature. Its value lies in the seamless integration of inpatient, outpatient, and emergency response capabilities.

Inpatient And Outpatient Care: The Core Engine

The distinction between inpatient and outpatient care is fundamental. Inpatient coverage applies when you are formally admitted to a hospital for an overnight stay. This covers major events—surgery, anesthesia, nursing care, and hospital-administered diagnostics. This is your primary shield against significant medical events.

Conversely, outpatient coverage pertains to medical care that does not require hospital admission. This includes consultations with your general practitioner or a specialist, prescription medications, and diagnostic imaging such as MRIs or CT scans. For proactive health management, robust outpatient benefits are what ensure consistent, high-quality care.

A policy strong in one area but weak in the other creates a dangerous gap in your protection. You require a plan that provides the same level of coverage for a specialist consultation as it does for a major surgical procedure requiring an extended hospital stay.

Emergency Medical Evacuation: The Ultimate Failsafe

For any U.S. citizen living or working internationally, emergency medical evacuation is an absolute non-negotiable. This benefit covers the substantial cost of transporting you from a location with inadequate medical facilities to the nearest center of excellence capable of managing your specific condition.

Without it, you could face a liability exceeding $100,000 for a single transport. A premier plan removes that financial risk, ensuring that your geographic location never dictates the quality of care you receive. It is the ultimate guarantee of access to world-class treatment, irrespective of where an emergency occurs.

The Strategic Decision Of US Coverage

One of the most significant decisions you will make is whether to include the United States in your geographic area of coverage. Due to the exceptionally high cost of U.S. healthcare, adding it to your plan can easily double your annual premium.

- Worldwide Excluding USA: This is a prudent choice for expatriates who spend minimal time in the States or maintain separate domestic insurance for visits. It yields significant cost efficiencies without compromising the quality of your care anywhere else in the world.

- Worldwide Including USA: This option provides complete global portability, allowing you to seek treatment anywhere, including back in the U.S. It is the preferred choice for those who travel frequently to the U.S. or demand the certainty of unrestricted access to American medical facilities.

Customizing Your Plan With Optional Riders

Beyond the core essentials, the best plans allow for customization through optional add-ons, or riders. This is how you tailor a plan to your specific life requirements.

To help you distinguish between standard inclusions and optional enhancements, here is a breakdown of common features in premier plans.

Essential Versus Optional Coverage Features

| Coverage Feature | Standard Inclusion | Optional Add-On (Rider) | Key Consideration for US Citizens |

|---|---|---|---|

| Inpatient Hospitalization | ✅ | The core of any plan; ensure high or unlimited annual maximums. | |

| Outpatient Care | ✅ | Essential for managing day-to-day health proactively. | |

| Emergency Evacuation | ✅ | Non-negotiable for anyone living or working overseas. | |

| Comprehensive Dental | ✅ | Often includes major restorative work like crowns and root canals. | |

| Vision & Eyewear | ✅ | Covers examinations, prescription glasses, and contact lenses. | |

| Maternity Care | ✅ | Crucial for family planning; typically subject to a waiting period. | |

| Wellness & Preventive | ✅ | Extends beyond basic check-ups to include advanced screenings. |

Careful selection of these components transforms a generic policy into a bespoke strategy for protecting both your health and your assets. Common riders include:

- Comprehensive Dental and Vision: Covers everything from routine prophylaxis and examinations to major dental procedures and corrective eyewear.

- Maternity Care: Provides coverage for prenatal consultations, delivery, and postnatal care—essential for those planning to start or expand their family abroad.

- Wellness and Preventive Care: Augments basic physicals to include more extensive health screenings and wellness programs.

When evaluating these add-ons, your diligence must extend beyond the benefits to the limitations. It is imperative to watch out for policy exclusions to ensure the coverage is as robust as it appears.

The Financial Strategy Behind Global Medical Plans

To view international health insurance as a mere travel expense is a profound misjudgment. For a US citizen living or working abroad, a top-tier plan is not a cost—it is a sophisticated financial instrument designed to protect your wealth. It functions less like a simple insurance policy and more like a strategic hedge against the acute financial volatility of a major medical crisis overseas.

The premium for these plans is not an arbitrary figure. It is a calculated risk assessment, meticulously priced based on a handful of key factors. By understanding these variables, you can architect a policy that provides optimal protection for your specific circumstances.

This reframes the conversation from "how much does it cost?" to "what is the value of the risk I am transferring?" A single medical emergency abroad can easily generate six-figure expenses. Viewed through this lens, a robust policy becomes an essential component of any serious asset management strategy.

Deconstructing Your Premium

The premium for an international health insurance for us citizens plan is the output of a precise algorithm. The primary inputs are your personal risk profile and your selected coverage parameters. Insurers weigh these elements carefully to arrive at a price that reflects their potential exposure.

Four main factors drive the bulk of your premium calculation:

- Age and Health Profile: Actuarial data is clear—medical needs generally increase with age. Premiums are tiered to reflect this reality, with costs escalating as you move into higher age brackets.

- Geographic Area of Coverage: This is arguably the most significant variable. A plan providing unrestricted global coverage will be priced very differently from one limited to a specific region, such as Southeast Asia.

- Deductible and Coinsurance Levels: This determines the portion of initial cost you are willing to assume. Opting for a higher deductible—the amount you pay out-of-pocket before the insurer's liability begins—will reduce your annual premium.

- Overall Policy Limit: This is the maximum amount the insurer will pay out in a policy year. While a lower limit can reduce your premium, for any individual focused on asset protection, securing a high or unlimited annual maximum is the only prudent course of action for true financial peace of mind.

The core concept is straightforward: a higher premium corresponds to a greater transfer of financial risk from your personal balance sheet to the insurer's. The objective is to identify the optimal point where you retain a manageable level of risk while shielding your assets from a catastrophic loss.

The Decisive Impact of US Coverage

The decision to include or exclude the United States in your coverage area has a profound financial impact. Due to the extraordinarily high cost of medical care in the US, adding it to your plan can easily double your premium. This is not an arbitrary surcharge; it is a direct reflection of the immense financial risk insurers assume when covering treatment within the American healthcare system.

The data is compelling. According to the Peterson-KFF Health System Tracker, U.S. healthcare spending per capita is nearly twice as high as in comparable developed countries. This cost differential is a primary driver for any insurer providing coverage in the U.S.

This single choice highlights the need for a strategic, not merely transactional, approach. It is also vital to understand the broader context of rising healthcare costs. You can read more about why medical insurance premiums rise year after year to gain a deeper understanding for long-term planning. By thoughtfully structuring your coverage, you can secure the protection you need without overpaying for benefits you may not utilize.

A Strategic Framework for Selecting Your Plan

Let us be direct: selecting the right international health insurance is not a casual undertaking. It is a serious exercise in financial and personal due diligence. Approach it less like shopping and more like vetting a critical business partner—one to whom you will entrust your health and financial security on a global scale.

The objective is not merely to find a policy that appears adequate on paper. It is to construct a coverage strategy that is perfectly tailored to your life, providing absolute confidence in your protection, no matter where you are in the world. This framework is designed to help you achieve that.

First, Define Your Personal Blueprint

Before reviewing a single brochure or quote, you must meticulously map out your own circumstances. This is the most crucial step. An error at this stage will cascade through every subsequent decision. A granular analysis of three key areas is required.

Begin by delineating your global footprint and health profile:

- Your Travel and Residency Patterns: Where do you actually reside and travel? Precision is key. A U.S. citizen based in Singapore with occasional business in Europe has vastly different requirements than an individual dividing time between London and Hong Kong. List your primary countries of residence and frequent destinations.

- Your Geographic Coverage Needs: Based on your established patterns, what is your non-negotiable coverage area? Can you operate effectively with a "Worldwide excluding the USA" plan, or do you require unrestricted global access, including for professional or personal trips back to the United States?

- Your Health and Family Profile: Now, a candid assessment is required. What is your current health status? That of your family? Document any pre-existing conditions, ongoing treatments, or potential future needs such as maternity care. A clear understanding of your health baseline is essential. You can delve deeper into which type of expat medical insurance policy is right for you.

Next, Vet the Insurance Providers Themselves

Once your personal blueprint is established, you can begin to evaluate insurers. A critical point: the company you choose is as important as the policy it offers. For discerning individuals, the standard for service and reliability is exceptionally high.

Use these criteria to place potential insurers under rigorous scrutiny:

- Financial Stability: This is non-negotiable. Look for providers with impeccable ratings from independent agencies like A.M. Best. An A- rating or higher is a strong indicator of an insurer's ability to meet its obligations. A top rating signifies the capacity to pay a multi-million dollar claim without financial strain.

- Client Service Excellence: What is the actual service experience? Will you have a dedicated account manager, or will you be routed through an anonymous call center? Is a 24/7 multilingual assistance service available? Test their responsiveness. Initiate contact and evaluate the quality of the interaction.

- Their Direct-Billing Network: A premier provider will not require you to front a $100,000 hospital bill and await reimbursement. They will have an extensive network of elite hospitals where they settle accounts directly. This is a massive differentiator that ensures a seamless, stress-free experience during a medical event.

The ultimate measure of an insurance provider is not the quality of its marketing materials, but its proven ability to perform flawlessly at the moment of a crisis. Financial stability and an impeccable service record are non-negotiable.

This structured vetting process ensures you secure more than just a policy document; you gain a reliable partner. This is particularly crucial considering that medical emergencies, often involving complex and costly evacuations, are a primary driver of claims for U.S. citizens abroad. You can review a full analysis of travel insurance statistics and trends at EmergencyAssistancePlus.com.

Ensuring Your Global Health and Financial Security

A successful international life requires more than astute management of your career and personal affairs—it demands the construction of a robust foundation to protect your health and financial assets. Selecting the right international health insurance is not a perfunctory task. It is the final, critical component that ensures a medical emergency will not jeopardize your financial stability or compel you to accept substandard care.

If there is one singular takeaway from this guide, it is this: your U.S. health plan is an inappropriate instrument for this purpose. It was designed for a different geography and a different set of circumstances. It is simply not viable for a life lived abroad.

Recapping the Core Pillars of Your Decision

True security is not derived from merely holding a policy, but from holding the right policy. This begins with a solid foundation of non-negotiable benefits. You must absolutely prioritize comprehensive coverage that includes high-limit inpatient care and readily accessible outpatient services.

However, the ultimate safety net, the one feature that can single-handedly avert a financial catastrophe, is emergency medical evacuation. This is not an ancillary benefit. It is the core component that guarantees geography will never be the determining factor in the quality of care you receive.

Regard your international health insurance as an active financial tool. It is a powerful shield that insulates your net worth from the staggering and unpredictable costs of global healthcare, granting you the confidence to live and work anywhere in the world.

Another pivotal decision is the inclusion of U.S. coverage. This choice directly influences your premiums and allows you to align the plan precisely with your travel habits and lifestyle. Lastly, your due diligence must extend beyond the benefits to the provider's financial strength and reputation. You require a partner of unimpeachable reliability.

Integrating Health Security into Your Financial Plan

Ultimately, this decision is a key part of your overall financial architecture. To truly protect both your health and your wealth on a global scale, you need a plan that integrates seamlessly with your long-term objectives. For a more extensive exploration of this topic, resources on comprehensive financial planning for expats can provide valuable context.

By choosing the right international health insurance, you are not just purchasing a policy. You are making a strategic investment in your future. It is this investment that provides the peace of mind necessary to truly thrive, secure in the knowledge that you are protected, whatever may arise.

Frequently Asked Questions

In the course of evaluating global medical coverage, a handful of critical questions invariably arise. For high-net-worth U.S. citizens who value precision and clarity, obtaining definitive answers is a non-negotiable prerequisite to any commitment. Here, we address the most common inquiries regarding international health insurance for us citizens.

These are not generic responses. They reflect the real-world complexities and strategic considerations you will face when securing premier medical protection for your international lifestyle.

Does My US Health Insurance or Medicare Cover Me Abroad?

In virtually all circumstances, the answer is an emphatic no. Your domestic U.S. health insurance, including ACA marketplace plans and particularly Medicare, is designed exclusively for use within the United States. Its provider networks, billing infrastructure, and entire operational framework are confined by U.S. borders.

Relying on these plans overseas constitutes an immense financial risk. While some may offer extremely limited coverage for a true, life-threatening emergency, they will not cover routine physician visits, specialist consultations, or any form of ongoing care. For any significant duration abroad, a dedicated international plan is not an option—it is an absolute necessity.

What Is the Difference Between Travel and International Health Insurance?

This is a critical distinction. Consider it in these terms: travel insurance is a short-term, acute-care solution for trips, typically under 90 days. It is designed to address unexpected emergencies—a sudden illness, an accidental injury—and travel-related disruptions like a cancelled flight.

International health insurance, conversely, is your primary health plan for long-term residence abroad (six months or more). It is the comprehensive, robust coverage that manages everything from annual physicals and chronic conditions to major surgeries and oncology treatments. It is your actual healthcare infrastructure, globalized.

Should I Include USA Coverage in My International Plan?

This is a purely strategic financial decision. Adding the USA to your area of coverage can easily double your premium, a direct consequence of the exceptionally high cost of American healthcare. The optimal choice depends entirely on your lifestyle and frequency of travel to the U.S.

- Exclude the USA: This is the prudent, cost-efficient strategy if you spend minimal time in the States. Many expatriates in this position maintain a separate, high-deductible plan in the U.S. to cover short visits.

- Include the USA: If you return to the U.S. frequently for business or personal reasons, or if you require the absolute freedom to consult with American physicians for a serious condition, including it is essential. It provides seamless, uninterrupted protection regardless of your location.

How Are Pre-existing Conditions Handled by These Plans?

An insurer's approach to pre-existing conditions is a key differentiator between a standard and a premier plan. The single most important action you can take is to provide a complete and transparent medical history during the underwriting process. Any omission or misrepresentation can be grounds for policy cancellation precisely when you need it most.

Top-tier insurers have several methods for addressing this. Some may offer full coverage, potentially after a specified waiting period. Others might apply a premium surcharge or place a specific exclusion on that condition. This is where expert guidance becomes indispensable—in identifying the one plan that aligns perfectly with your specific health profile.

At Riviera Expat, we provide precisely this level of expert guidance. We help you navigate the complexities of these questions to identify a plan that affords you complete clarity, control, and confidence in your global healthcare strategy. Contact us for a complimentary consultation.