The primary question for any global citizen is direct: What is the definitive cost of international medical insurance?

There is no single figure. A robust plan may be valued at $4,000 annually for a young professional, whereas a senior executive might see premiums exceeding $10,000 annually. The final investment is contingent upon your unique circumstances and global footprint. This is not merely an expense; it is an investment in your peace of mind and access to premier medical care, regardless of your location.

The True Cost of Global Healthcare Coverage

The premium for a first-rate international medical plan is not an arbitrary number. It is a meticulously calculated figure reflecting your personal profile, the jurisdictions where you require care, and the specific benefits selected. For high-net-worth individuals, defining this figure accurately is a non-negotiable component of sophisticated financial planning.

This guide is structured to move beyond generic price ranges and deconstruct the specific factors that drive your premium. My objective is to provide a clear framework for evaluating value, not just price, enabling you to invest wisely in your health security. The appropriate policy is a strategic asset, ensuring your global lifestyle is supported by world-class medical protection.

Before delving into the specifics, it is beneficial to gain a sense of the full landscape. Exploring comprehensive international health insurance options can provide a clearer understanding of the breadth of possibilities available.

A Baseline for Your Investment

To ground this discussion, let’s examine specific figures. The table below offers a concrete starting point, illustrating how annual premiums shift based on two primary variables: your age and the comprehensiveness of your chosen plan.

These figures should be considered a baseline for your potential investment. They deliberately exclude coverage within the United States, which constitutes a distinct and significantly more expensive market.

Estimated Annual Premiums for International Medical Insurance

This table provides estimated annual premium ranges for an individual, illustrating how costs vary by age and level of coverage (excluding USA coverage). These figures serve as a baseline for understanding potential investment.

| Coverage Tier | Young Professional (Age 30) | Senior Executive (Age 55) |

|---|---|---|

| Standard | $4,000 – $6,500 | $9,500 – $12,000 |

| Enhanced | $6,000 – $8,500 | $12,000 – $16,000 |

| Premier | $8,000 – $11,000+ | $15,000 – $25,000+ |

As illustrated, the investment escalates with both age and the richness of the benefits. This is logical, as it directly reflects the actuarial risk and the scope of services included in more robust plans.

With this initial perspective, we can now explore the core factors that will ultimately shape your final premium.

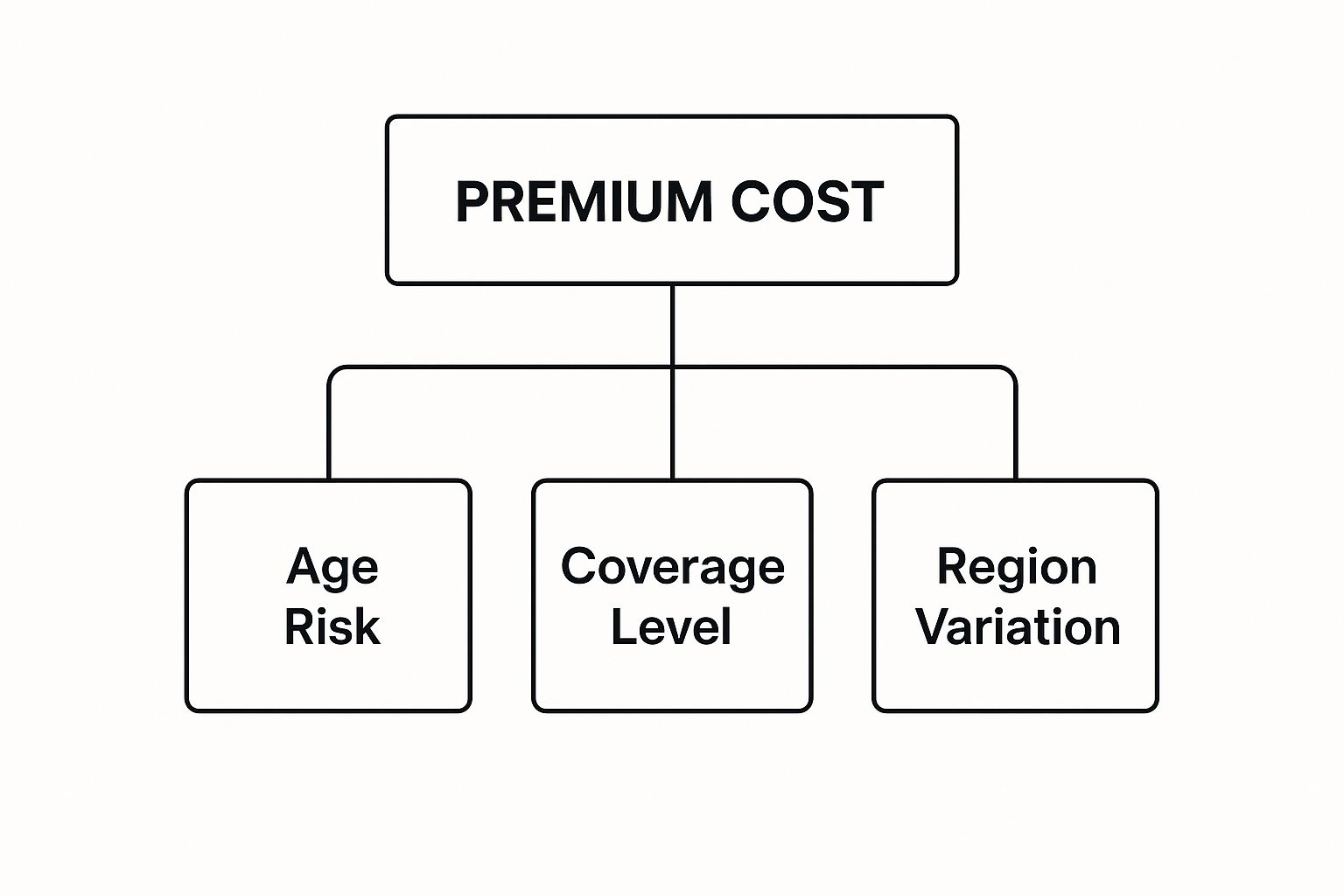

The Three Pillars That Define Your Premium

To fully comprehend the cost of your international medical insurance, one must look at its foundational components. Insurers construct your premium based on three core pillars: your age, your geographic area of coverage, and the level of benefits you select.

Consider the construction of a bespoke residence. Your age is the foundation, the region of coverage is the structural frame, and the benefits are the interior finishing. Each element contributes a layer to the final cost.

This hierarchy—age, region, and benefits—forms the blueprint for your premium.

An understanding of how these components interrelate allows you to make strategic decisions to secure the right coverage without over-investing.

Age and Actuarial Risk

Of all factors, age is the most straightforward and non-negotiable. For an insurer, age is the clearest indicator of health risk. Actuaries utilize vast datasets to predict the likelihood of claims for individuals within a specific age demographic.

A 30-year-old professional, for instance, is statistically far less likely to require major surgery or ongoing care for a chronic condition than a 60-year-old executive. This is why premiums for a 55-year-old can be two to three times higher than for a 30-year-old with an identical plan. It is a direct reflection of anticipated healthcare needs.

This is not a penalty for aging, but rather a pricing model based on shared risk. The premiums paid by all individuals in your age bracket contribute to a pool designed to cover the potential care for that entire group. This ensures the insurer’s financial solvency to pay significant claims when they arise.

Your Geographic Area of Coverage

The second pillar is your area of coverage, and one choice is paramount: whether to include the United States. The U.S. healthcare system operates on a cost scale that vastly exceeds the rest of the world.

Adding USA coverage to your plan can easily double your annual premium. A medical procedure that costs $20,000 in a premier European hospital could escalate to $100,000 or more in an American equivalent. Insurers must price policies to account for this significant disparity.

Consequently, plans are almost invariably structured in two ways:

- Worldwide excluding USA: The standard choice for individuals who do not reside in or travel frequently to the United States.

- Worldwide including USA: An essential requirement for those who need seamless medical access within the United States.

Making the correct decision here is one of the most significant levers you can pull to manage your costs effectively.

The Scope of Your Benefits

Finally, the richness of your plan directly influences its price. The level of benefits you select determines the extent of your financial protection. This is where you customize your coverage.

A foundational plan might only cover inpatient care—services requiring hospital admission, such as surgery or treatment for a major illness. This is the most affordable option, providing a critical safety net for catastrophic events.

However, many individuals require more extensive coverage. Adding modules for services such as outpatient care (GP visits, specialist consultations, diagnostic tests), dental and vision, or wellness checks will increase the premium with each addition. Every benefit you add increases the insurer’s potential payout, and the price adjusts accordingly. This modular design allows you to construct a plan that precisely fits your lifestyle and health priorities.

Understanding Global Medical Inflation Trends

Your personal profile and policy choices are significant, but they do not exist in isolation. The cost of international medical insurance is heavily influenced by a powerful economic force: medical inflation. This is the annual percentage increase in healthcare costs, and it is the primary driver of premium adjustments year after year.

This is not a mere economic theory; it is an essential consideration for your long-term financial planning. Consider it a powerful current in the ocean of global healthcare. While your personal choices steer your vessel, this current affects everyone’s journey, making it critical to understand its direction and strength.

Medical inflation is distinct from the standard consumer price inflation. Its engine is fueled by high-cost medical technologies, breakthrough pharmaceuticals, and a rising global demand for premier healthcare.

Why Costs Are Rising Globally

Innovation is the principal engine driving medical costs upward. Revolutionary treatments, from gene therapies to advanced robotic surgeries, deliver superior outcomes but come with a substantial price tag. As these technologies become the standard of care in leading hospitals, the baseline cost of treatment increases for everyone.

This trend is not uniform across the globe. Certain regions are experiencing more significant cost pressures than others, a vital detail for anyone living or working internationally. For instance, the global cost of medical insurance is experiencing sustained double-digit growth. The 2025 Global Medical Trends Survey projects the global average medical trend rate to be between 10.0% and 10.4% for 2025.

A closer look at regional data reveals that North America’s rate is expected to climb to 8.7% in 2025, while Asia Pacific’s is projected to reach an impressive 12.3%. Meanwhile, the Middle East and Africa region faces the most dramatic acceleration, with trends forecasted to reach 12.1%.

This data demonstrates the systemic pressures increasing your premiums, entirely separate from your personal health or claims history.

Regional Inflation Hotspots

For individuals who live or travel between global financial hubs, understanding these regional differences is absolutely critical.

- North America and Asia-Pacific: These regions are at the forefront of medical innovation. The rapid adoption of new diagnostic tools and exceptionally expensive specialty drugs creates a high-cost healthcare environment. In hubs like Singapore and Hong Kong, this is magnified by high demand from an affluent population that expects the highest standard of care.

- Europe: While still facing rising costs, medical inflation in Europe is often more moderate. This is largely due to established public health systems and stronger government controls on pharmaceutical pricing, which can mitigate the sharpest cost increases seen elsewhere.

These regional dynamics are precisely why your chosen area of coverage has such a direct and significant impact on your premium. They also explain why your premiums almost always increase annually, even if your personal health has remained unchanged.

To gain a more profound understanding of this topic, you can learn more about why medical insurance premiums rise annually in our detailed article. This knowledge provides the clarity to anticipate future costs and make more strategic decisions about your global health coverage.

How Your Location Dictates Your Insurance Premiums

While global inflation garners significant attention, the single most impactful factor determining your cost of international medical insurance is your primary country of residence. This has a direct and powerful influence on your annual premium. The focus is not on broad regions, but on the specific healthcare and economic reality of your location.

Consider the analogy of real estate. An apartment in central London carries a very different valuation than one in a quiet village, even with identical square footage. The same logic applies to health insurance. An insurer must price your policy based on the actual cost of providing medical care in your city.

A firm grasp of this principle is fundamental to your financial planning as an expatriate. When you understand why premiums vary so dramatically between global hubs like Dubai, Hong Kong, and Switzerland, you can make more informed decisions about your coverage and budget.

A Tale of Four Hubs: Why Premiums Diverge

Let’s be practical. The differences become crystal clear when we examine a few popular expatriate destinations. Each city possesses a unique blend of factors that directly shape insurance costs, demonstrating why a “one-size-fits-all” approach to global health insurance is ineffective.

- Switzerland: Renowned for its exceptional quality of care, Switzerland’s healthcare system is also among the world’s most expensive. High living standards and a mandatory insurance system create a very high-cost baseline. For expatriates, this means private insurance premiums are firmly at the upper end of the scale. You are paying for access to a premier system.

- Hong Kong and Singapore: These Asian financial powerhouses boast some of the finest private hospitals on the planet. This world-class care, however, comes at a significant price. The cost of cutting-edge technology and top-tier medical talent is immense, and high demand from an affluent population maintains high prices. Your insurance premium must reflect that reality.

- Dubai: As a major crossroads in the Middle East, Dubai has developed a world-class private healthcare system at a remarkable pace. Costs for certain procedures can be lower than in Europe or Asia, but a mandatory insurance requirement and a transient expatriate population create a highly competitive and dynamic market that influences how all policies are priced.

To see how deeply local economics affect healthcare costs, consider the general cost of living in Ireland. Higher living costs almost invariably correlate with higher healthcare expenses and, consequently, higher insurance premiums.

Regional Snapshot of Healthcare Costs and Insurance Premiums

The following table provides a comparative look at key expatriate destinations, highlighting the core factors that drive local insurance premiums.

| Region/City | Average Healthcare Quality | Key Cost Drivers | Typical Premium Tier |

|---|---|---|---|

| Switzerland | Exceptional | High standard of living, mandatory insurance system, premier facilities | Very High |

| Hong Kong / Singapore | Very High | Advanced technology, top medical talent, high demand from affluent population | High |

| Dubai | High | World-class private facilities, mandatory insurance, competitive market | Medium to High |

| Thailand | Good to Very Good (in major cities) | Medical tourism, excellent private hospitals, lower general cost of living | Medium |

This snapshot illustrates a clear pattern: the quality and cost of local healthcare are directly mirrored in the price of your insurance.

The Economic Engines Driving the Cost

The price differences between these cities are not arbitrary. They are anchored in local realities such as government regulations, the balance between private and public healthcare, and the country’s overall economic climate.

The local cost of care is the single most important variable. A simple consultation or a complex surgical procedure will have a dramatically different price tag in Zurich compared to Bangkok, and your insurer must account for this potential liability. This is why accurately declaring your main country of residence is not just a formality; it is a core component of your policy’s pricing and validity.

This is amplified by regional inflation. For example, some forecasts predict that the medical trend rate—the growth in healthcare costs—in Asia-Pacific could reach 11.1% in 2025. This surge, fueled by sharp increases in countries like New Zealand and Thailand, ripples across the entire regional insurance market.

Ultimately, your choice of home base determines the hospitals you can access and the price of that access. Ensuring your policy is built for that specific reality is crucial. A strong provider network in your area can be a decisive advantage, a topic explored in our guide on the importance of global medical networks.

Optimizing Your Policy for Cost and Value

Understanding the drivers of your international medical insurance cost is one part of the equation. Actively managing those factors to construct a policy that delivers robust value without being prohibitively expensive is another skill entirely.

This is not an exercise in finding the cheapest plan available. It is about making intelligent, strategic decisions to take direct control over your policy’s design. By adjusting key components, you can significantly influence your annual premium while retaining the high-quality, comprehensive protection you require.

The Art of Strategic Cost-Sharing

One of the most powerful methods for managing your premium is through cost-sharing. It is a straightforward trade-off: you agree to cover a small portion of your medical expenses in exchange for a lower insurance premium. The two primary tools for this are deductibles and co-payments.

- Deductibles: This is the fixed amount you pay out-of-pocket annually before your insurance company begins payments. Selecting a higher deductible—for example, increasing it from $1,000 to $5,000—can reduce your annual premium by 15% to 30%. It is an excellent strategy if you can comfortably cover smaller medical costs but require absolute protection against a major health event.

- Co-payments: This is a small, fixed fee you pay for a specific service, such as a specialist consultation or a prescription. Incorporating a co-payment structure means you share a predictable cost for routine care. This lowers the risk for the insurer, and those savings are passed to you as a lower premium.

By thoughtfully combining these elements, you effectively self-insure for minor expenses while preserving your premier insurance for significant events.

View your policy as a sophisticated financial instrument. Adjusting your cost-sharing is akin to fine-tuning an investment portfolio—you are calibrating it to match your personal financial position and risk tolerance.

Modular Design for Precision Coverage

The best international health plans are no longer one-size-fits-all. They are built with a modular design, allowing you to assemble a policy that perfectly aligns with your life. The foundation of any quality plan is always inpatient coverage for hospital stays.

From this core, you can select the modules you genuinely need:

- Outpatient Care: Covers everyday health needs like GP visits, specialist appointments, and laboratory tests.

- Dental and Vision: Provides coverage for everything from routine cleanings to major dental work and corrective eyewear.

- Wellness and Preventative Care: Includes benefits for health screenings, check-ups, and vaccinations.

For a young family, a robust outpatient module is likely non-negotiable. However, a single, healthy individual might choose to forgo a comprehensive dental plan to manage costs. Our guide on choosing the right expat medical insurance policy type delves deeper into how these choices shape your final plan.

To truly maximize your policy’s value, a key first step is understanding legal documents, as they form the contract between you and your insurer.

The Financial Wisdom of Wellness

A final consideration for managing long-term costs is to invest in your own health. Adding a wellness and preventative care module may slightly increase your premium today, but it is one of the most astute financial decisions you can make.

Regular health screenings and check-ups can detect potential issues long before they become serious and costly to treat. By proactively addressing future health risks, you also mitigate their significant associated costs. It is a proactive approach that secures both your physical and financial well-being for years to come.

The Future of International Health Premiums

Looking ahead, it is clear that three powerful forces are shaping the future of global health insurance: relentless medical inflation, incredible technological advancements, and the increasing number of professionals living and working abroad.

Contemplating these trends is not merely an academic exercise. It is fundamental to protecting your long-term financial health and ensuring you always have access to premier medical care, regardless of where your career takes you. The cost of international medical insurance is on an upward trajectory, and these are the underlying reasons.

This outlook presents both challenges and opportunities. On one hand, public healthcare systems in many developed nations are under strain from aging populations and budgetary constraints. This elevates a premier international plan from a luxury to a necessity—it is your guarantee of access that public systems may struggle to provide in the future.

The Expanding Global Premium Market

The market itself is poised for substantial growth, indicating how essential this coverage is becoming. Projections suggest that over the next decade, the global insurance premium pool is set to grow by a staggering EUR 5,319 billion.

A significant portion of that—approximately EUR 1,743 billion—is expected to come from health insurance alone. This is not a minor increase; it represents a clear global pivot toward private coverage. You can explore the complete analysis of these global insurance market projections for a comprehensive view.

This growth, however, will not be distributed evenly. While the United States will remain a major driver, the most significant expansion is occurring in Asia. In fact, Asian markets, particularly China, are predicted to account for over half of the new premium growth in both life and health insurance, adding approximately EUR 1,071 billion to the market.

These are not just large numbers. They signal a market that is becoming more competitive, diverse, and robust. For discerning individuals, this translates into a wider choice of specialized products and services designed to meet the high standards of a global citizen.

Your Strategy for Future Security

What does this mean for you? While underlying costs are likely to continue their ascent, you are not a passive observer.

The key takeaway is the absolute necessity of proactively managing your global health plan. The future demands a more strategic mindset when choosing and maintaining your coverage.

This involves regularly reviewing your plan against your evolving personal and professional circumstances, understanding the cost drivers in the countries where you reside and work, and making conscious decisions about your benefits. By doing so, you transition from simply paying a premium to actively managing a critical personal asset.

This strategic oversight is the bedrock of your long-term financial security. It ensures that no matter how the market evolves, your access to world-class healthcare remains a certainty, providing the confidence and peace of mind to focus on what you do best.

Frequently Asked Questions

When determining the cost of international medical insurance, a few key questions consistently arise. Let us address them directly to provide the clarity you need to make informed decisions.

Why Are My Premiums So High Even Though I’m Perfectly Healthy?

This is a valid and frequent question. You are in excellent health and rarely consult a physician, yet your premium seems substantial.

The premium is not solely a reflection of your personal health. It is based on the collective risk of your age demographic and, critically, the high cost of medical care in the jurisdictions where you require coverage. Your policy is priced to shield you from a financial catastrophe—a sudden, severe illness or accident that could incur costs in the hundreds of thousands of dollars.

Your premium is the price for absolute financial security against a worst-case medical scenario. It is calculated based on the risk of a large group, not just your individual health status.

Can I Negotiate My Premium?

While you cannot negotiate the base rates with actuaries, you can absolutely influence your final price.

This is achieved by strategically tailoring your plan’s structure. You have direct control over the variables that determine your cost, which is a powerful way to impact the final premium.

Key levers you can adjust include:

- Increasing your deductible: A direct trade-off where you agree to cover more of the smaller costs yourself in exchange for a lower annual premium.

- Adding a co-payment: By sharing a small, fixed portion of predictable costs, you can reduce your overall premium.

- Removing non-essential coverage: If you do not anticipate needing optical and dental benefits, trimming these modules is an easy way to lower the price.

How Does a High Deductible Affect My Total Cost?

Opting for a higher deductible is one of the most effective strategies for reducing your annual premium. I often recommend this approach for clients who can comfortably pay for routine check-ups or minor illnesses out-of-pocket.

This allows you to self-insure for smaller expenses while retaining robust protection against a major health crisis with potentially devastating financial consequences. You reduce your fixed insurance costs but keep the full power of the plan for when it is truly needed. It is also important to note that external factors are increasing costs for everyone—for instance, 57% of global insurers are concerned that the declining quality of public healthcare is forcing more individuals into the private system. You can gain more insights into these 2025 global medical trends and their impact on premiums.

At Riviera Expat, we provide the clarity and deep expertise required to design an international medical plan that perfectly aligns with your global lifestyle and financial objectives. Contact us for a personalized consultation and take control of your healthcare security.